gorodenkoff

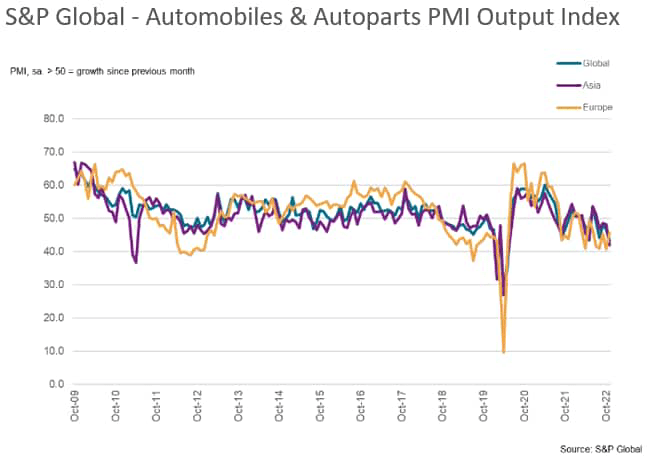

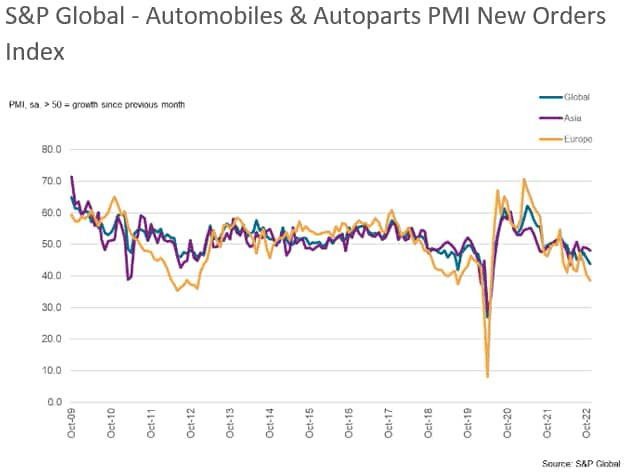

Latest global sector PMI data, compiled by S&P Global, highlighted the tough conditions being faced by Automobiles & Autoparts manufacturers at present, with the sector the second-worst performer of all those covered in November. Firms registered the most pronounced drop in production and new orders since the onset of COVID-19 in early 2020.

Meanwhile, for the first time in three months, staffing numbers declined, dropping at the quickest pace since July 2020, as producers adjusted capacity to weakened order book inflows.

More encouragingly, average cost burdens increased at a rate much faster than those recorded prior to the pandemic, and manufacturers continued to raise their selling prices in November, although rates of inflation showed signs of moderating amid weaker demand conditions. This also helped to alleviate pressure on supply chains.

Collapse of European demand drives global deterioration

Central to the downturn in the global autos sector was a slump in European demand. In fact, November data saw the sharpest contraction in European order book volumes since May 2020 and one of the steepest recorded over the past decade. The current sequence of decline first began in March 2022 as selling price inflation was ramping up, eventually hitting a peak in April. With various nations experiencing a severe cost-of-living crisis, particularly within Europe, the demand for many cyclical goods, automobiles included, will be on the decline. The rate of output price inflation is still among the highest on record, and with the cost-of-living crisis becoming an increasingly prominent issue heading into the winter months, it’s unlikely that we will see European autos demand recover anytime soon.

In terms of production, output across Europe’s autos sector continued to fall in November, but at the softest rate since June and not to the same extent as seen in new orders. Backlogs of work fell at the fastest pace since May 2020, while stocks of finished goods accumulated at the fourth-sharpest pace in the series history. These factors helped to prevent a much sharper fall in production during the month.

Demand trends lead to lower output in Asia

Trends in Europe have seemingly fed through to Asia, where manufacturers registered the fastest reduction in output volumes since May 2020. Moreover, autos firms in Asia registered the sharpest contraction in output of the 18 monitored industries. That said, relative to the drop seen in Europe, the decline in new orders was notably softer amid cooling cost pressures and easing supply chain disruptions, and Asia’s data are dominated by trends in mainland China, where the ongoing fight against COVID-19 continues to cause lumpy trends in demand and output.

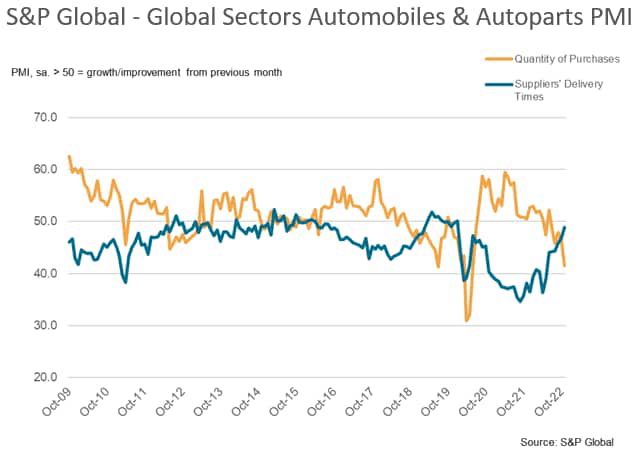

Muted input demand eases supply chain pressures

There have been tentative signs that supplier performance across the global autos sector has been improving in recent months. November data revealed the softest deterioration in vendor performance since January 2020, with lead times lengthening to a smaller degree than the pre-pandemic average. Alongside reduced pandemic disruptions, the factor perhaps playing a prominent role in an improving supply picture has been a substantial drop in demand for inputs. To mirror output trends, firms have scaled back on purchasing activity at a rate which is among the sharpest in the PMI series history, and subsequently, there is much less pressure on suppliers.

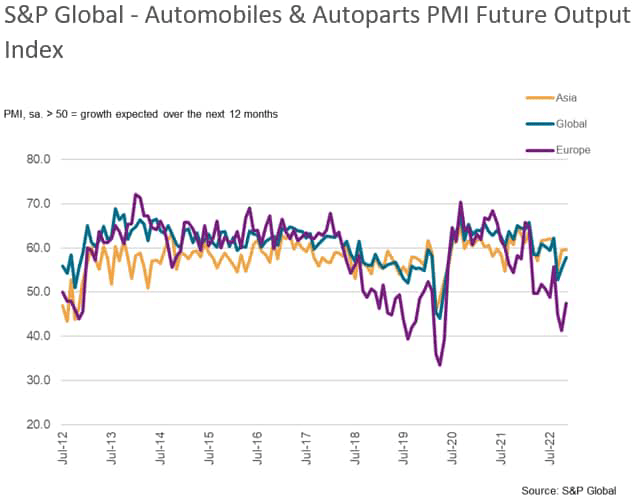

Business sentiment upheld by optimism at Asian manufacturers

While November PMI data paint a gloomy picture for the global autos sector, manufacturers maintained an overall positive outlook for output over the year ahead. That said, sentiment varied extensively by region. Optimism was underpinned by growth expectations across Asian autos producers. Meanwhile, European manufacturers registered a third consecutive month of pessimism, albeit less so than in October.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment