moxumbic/iStock via Getty Images![]()

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 12th, 2023.

Earlier in 2022, I looked at Clough Global Opportunities (NYSE:GLO) and PIMCO Global StocksPLUS & Income Fund (NYSE:PGP). I had concluded that PGP could be the better option going forward. This ended up being the final result in both of my previous updates. However, my opinion lately is starting to shift as most of the damage appears to be done with GLO now. So today, I wanted to provide a quick update on these funds.

The Basics

GLO

- 1-Year Z-score: -2.22

- Discount: -12.67%

- Distribution Yield: 11.36%

- Expense Ratio: 2.60%

- Leverage: 32.25%

- Managed Assets: $510 million

- Structure: Perpetual

GLO’s investment objective is “to provide a high level of total return.” The fund attempts to achieve this by “applying a fundamental research-driven investment process and will invest in equity and equity-related securities as well as fixed-income securities, including both corporate and sovereign debt.” They also include that the fund will “invest in both U.S. and non-U.S. markets.”

In the last annual report, the fund showed a total expense ratio with leverage included at 4.57%. That’s certainly on the higher end, but with reduced leverage – as we’ll touch on – that expense could come down. An expense ratio excluding leverage of 2.60% is still high.

PGP

- 1-Year Z-score: 0.69

- Premium: 4.40%

- Distribution Yield: 10.91%

- Expense Ratio: 1.63%

- Leverage: 39.43%

- Managed Assets: $135 million

- Structure: Perpetual

The objective of PGP is to “seek total return comprised of current income, current gains and long-term capital appreciation.” They attempt to achieve this through an “innovative StocksPLUS approach, pioneered by PIMCO…” They will “build a global equity and debt portfolio by investing at least 80% of the fund’s net assets in a combination of securities and instruments that provide exposure to stocks and/or produce income.”

Interestingly enough, PGP runs the lower expense ratio of the two. Of course, that can help the longer-term results, but PIMCO often charges high expense ratios. The 1.63% is still relatively high for more vanilla funds; being a more complex fund can be the reason. The total expense ratio comes up to 2.30% when including leverage expenses.

The Results

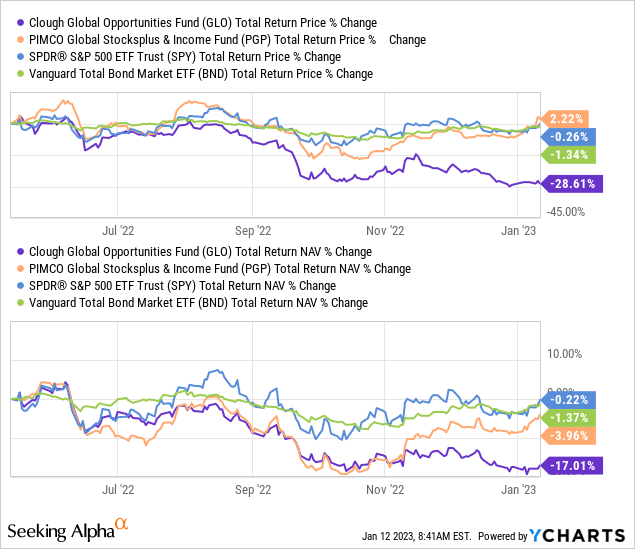

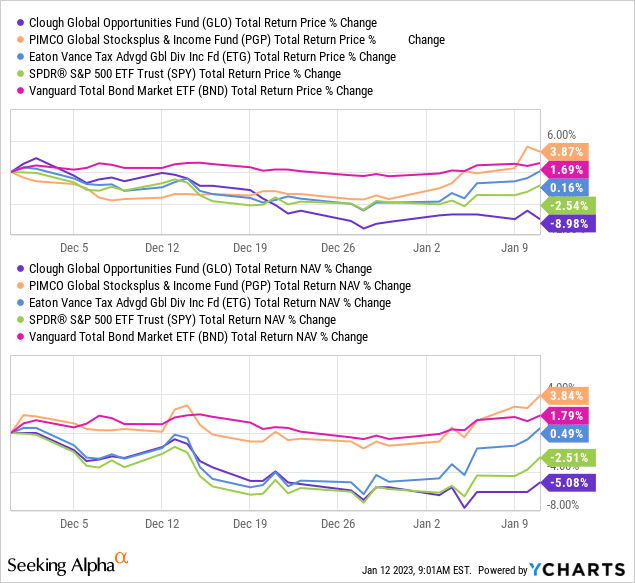

My first article was posted publicly on May 15th, 2022; at this point, here are the latest results. I’ve also included the SPDR S&P 500 ETF (SPY) and Vanguard Total Bond Market ETF (BND) performance for some context. Although, these are not appropriate direct benchmarks for either of these rather unusual funds with a high amount of flexibility.

At this time, GLO was sporting a premium, and PGP was at a discount, bizarrely enough. That discount/premium switching sides certainly helped the quite expected results we see below.

YCharts

For the most part, PGP and GLO followed each other on a total NAV return basis quite closely. It was in November that the divergence really happened on that metric. Still, on a total share price basis, the divergence happened much quicker due to valuation differences.

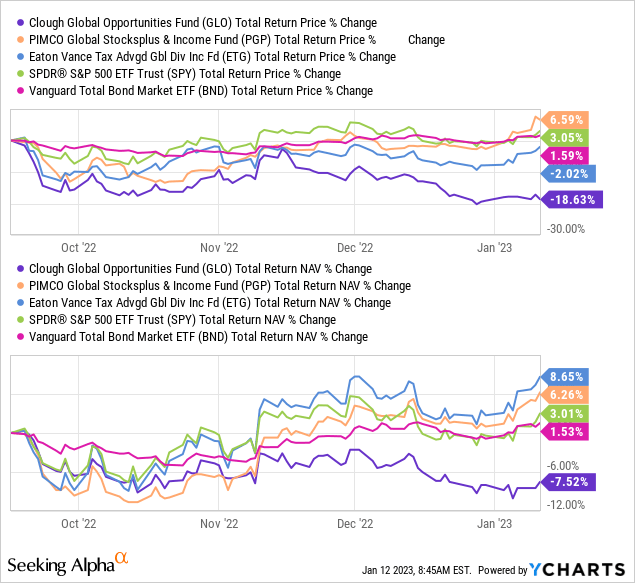

Later in the year, I touched on GLO once again. In this case, the market continued to struggle, and GLO was having a particularly difficult time. I once again finished that piece by saying PGP was a more attractive potential position. I even included Eaton Vance Tax-Advantaged Global Dividend Income (ETG) as a potential alternative as a more vanilla type closed-end fund.

That once again proved to be the right call. The article was posted publicly on September 16th, 2022. As we can see here, a closer look at when the total NAV return performance started to diverge.

YCharts

I titled that last article “Recovery Doesn’t Seem Likely.” I think some missed the main point, but it ended up coming to fruition. My main takeaway was meant to say that it was a highly leveraged fund that was susceptible to deleveraging. That it was trading at too narrow of a discount despite that huge risk.

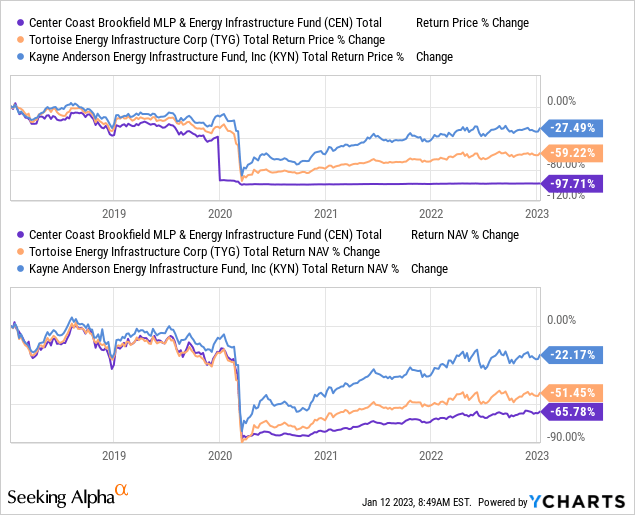

When deleveraging happens, it becomes an almost permanent loss of capital. When selling at lows, they have less capital to stay invested for the recovery. Check out leveraged energy CEFs from pre-COVID to after. Those show some of the most extreme examples but, regardless, illustrate the problem.

Below are Center Coast Brookfield MLP & Energy Infrastructure Fund (CEN), Tortoise Energy Infrastructure Corp (TYG) and Kayne Anderson Energy Infrastructure Fund (KYN) as examples. Important to note that TYG is no longer a pure-play energy fund.

YCharts

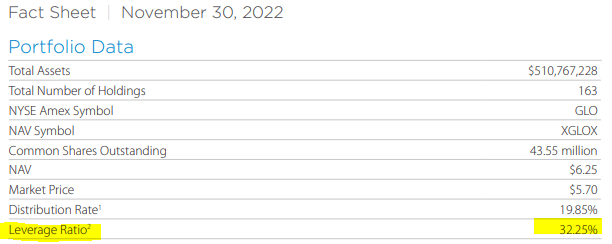

GLO had $257 million in borrowings at the end of April 30th, 2022, and they listed $204 million at the end of October 31st, 2022. That left leverage at a still very elevated level of around 43%.

Now, it would appear at the end of November 30th, 2022; leverage was slashed even further. At around 32%, we are looking at a more standard level of leverage for this type of fund.

GLO Portfolio Stats (Clough (highlights from author))

This would suggest that leverage is now down to around $165 million. Interestingly enough, this was probably beneficial for GLO because, since the end of November, the fund hasn’t performed well. So losses would have been even larger if they were still highly leveraged. Albeit, this is a very short time period, PGP, BND and ETG managed to put up positive results in this period.

YCharts

Now What?

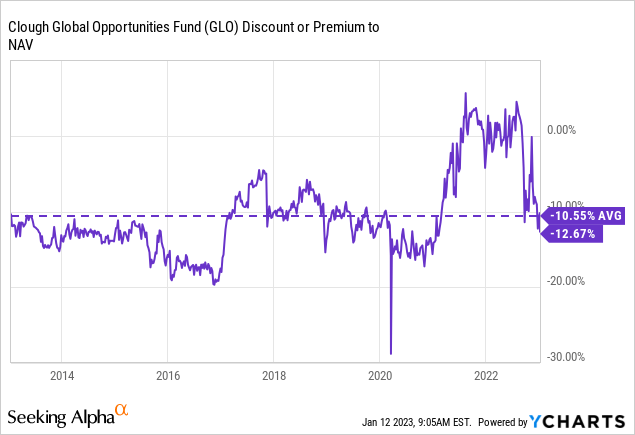

Despite the fund’s lack of performance in the short term, I believe that GLO is looking like a much better idea at this time. It could still be considered a speculative play, but the valuation means it is much more tempting. The discount has widened out considerably on this fund relative to PGP. ETG has also become more tempting, too, for what it’s worth.

YCharts

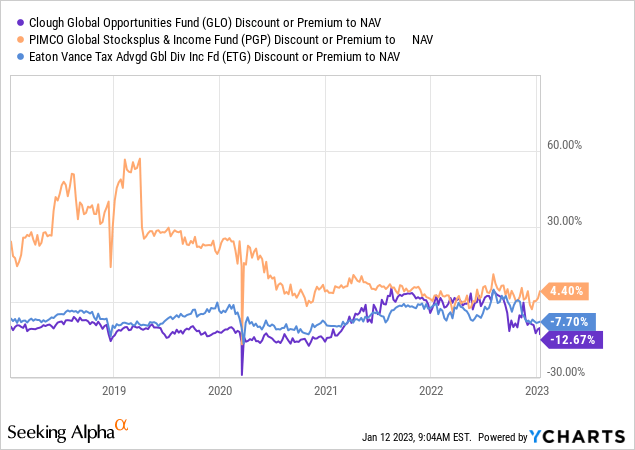

More specifically, we have crossed under the longer-term decade-long average discount/premium for GLO. We can see above that PGP has trended a lower and lower premium. So while PGP could make sense too, GLO’s is much more attractive here.

YCharts

One of the reasons for the drop is because of the fund’s managed distribution; it resets annually at 10%. When the fund had such a poor year, the distribution was slashed from $0.0943 to $0.0483. ETG also cut their distribution recently, which could have likely spurred their latest decline despite the relatively attractive results. ETG doesn’t have a managed distribution in terms of a targeted NAV.

GLO distribution History (Seeking Alpha)

All shareholders should have expected it because it’s spelled out for investors. And to be fair, a lot of investors realize this. Still, it always seems like there is at least a small group of investors who don’t see it coming and start panic selling.

In the long run, the fund should adjust lower. This is because it means less capital erosion, which means they have more assets to rebound with when that happens. The real question would be if they should keep it set at a 10% plan in the first place. They haven’t been able to achieve this in the long run. However, it provides a predictable distribution as investors can follow the NAV.

Conclusion

The damage is done for GLO; it’s looking like a much more tempting fund. Albeit, there are some serious headwinds we face in 2023, and they are still leveraged. But now that their leverage has decreased substantially, they are relatively less susceptible to permanent damage.

I would still consider this fund more of a short-term play because, historically, they’ve shown poor performance. A total NAV return of 1.76% in the last ten years should be evidence enough. One can compare that to 7.87% for PGP and 8.39% for ETG.

The latest results in the last 3 and 5 years are worse for all three of these funds but show GLO as the worst of them again, with negative results in both time frames. PGP had negative returns in the 3 years and positive in the 5 years. ETG put up positive results in both of these same time frames. The poor results in the shorter-term time frames are expected as, over the last year, most assets have taken a substantial hit.

A poor historical track record doesn’t mean going forward, it will also be poor, but even recent results show significant underperformance. Hence, there isn’t much evidence that things will change as their strategy hasn’t changed.

To sum it up as concisely as possible, PGP looks more like a solid hold at this point, and GLO seems like a buy but could be viewed as a shorter-term speculative buy.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment