Morsa Images

Ginkgo (NYSE:DNA) is committed to streamlining the process of engineering biology. Their goal is to scale the platform for programming cells, making it easier for customers to bring their ideas to life. By collaborating with clients to clearly define their product specifications, Ginkgo offers a comprehensive B2B solution that includes two key assets: our robust foundry and extensive code base.

The foundry serves as an automated laboratory, providing customers with the ability to convert typically underutilized R&D investments into a manageable variable cost that can be accessed as a service. This feature is particularly appealing in challenging economic conditions, especially for small companies looking to maximize their resources.

Ginkgo provides its customers with the benefits of scale economics and a continuously expanding code base. The code base accumulates valuable knowledge and data from experiments, allowing this information to be reused to improve program success and lower costs for customers. The company operates as a service-based business and has recently completed four acquisitions. They are open to potential customers reaching out and becoming part of their platform.

Standardizing offerings to facilitate sales

A significant task for Ginkgo is to establish an easily accessible set of offerings. While engineering cells is not as straightforward as a trip to the supermarket, the company is working to make the customer experience more intuitive, allowing potential customers to better understand the types of solutions and associated costs available to them. That has the potential to greatly aid in the sales process and make it easier for institutions to find the solutions they need.

Therefore, in order to enhance its sales efforts, Ginkgo is working to standardize its offerings and streamline the sales process. This involves standardizing key aspects such as milestones, cost structures, IP terms, and timelines, which helps to increase transparency and consistency in the sales process. This standardization also allows for greater automation and efficiency, making it easier to generate accurate quotes for clients. An example of this type of standardized offering is the company’s collaboration with Merck in the enzyme space, which serves as a model for future endeavors.

The addition of new programs and customers enhances both the platform and the financial performance of Ginkgo. The new programs add to the code base by offering valuable experiences that can lead to improved operations and decreased unit costs. The R&D fees generated by these new programs help to mitigate risk and can expand the customer base through inside sales efforts, further benefiting the company’s financial performance.

Furthermore, the introduction of new programs gives Ginkgo the chance to participate in the value generated by its customers’ products through means such as royalties, equity, or milestone payments. This diversification of the company’s exposure to various end-product markets through new program additions minimizes risk and enhances the likelihood of success. On the other hand, attracting new customers opens up opportunities for future growth through internal sales. Ginkgo’s track record of expanding relationships with existing customers, such as Bayer, highlights the effectiveness of the “land and expand” strategy, which presents a more streamlined sales cycle compared to onboarding a new customer.

The public figures are promising, as Ginkgo continues to attract new programs to its platform and had 15 new programs in the third quarter. The company had a successful partnership with Merck, leveraging its fungal strains, which holds the potential for up to $144 million in milestone payments. The agreement includes a collaboration with Merck to engineer enzymes for use as biocatalysts in Merck’s active pharmaceutical ingredient [API] production. Ginkgo will utilize its proficiency in cell engineering, enzyme design, and process optimization to create optimal strains for expression of the biocatalysts. The collaboration aims to make biocatalysis more cost-efficient by minimizing expensive synthesis and purification steps, using Ginkgo’s unique fungal strains. This project has the potential to lower the cost of goods and enhance the supply chain for APIs.

All-in-all, they aim to grow new programs by 80% YoY in 2023, from 31 programs last year to a range of 55-60 this year.

Financials

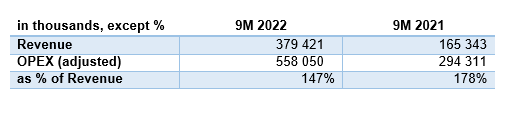

The Third Quarter of 2022 financial results indicate a decrease in overall revenue in comparison to the same period in the previous year. This is due to a one-time equity milestone payment in the foundry revenue for Q3 2021. Despite this, the company’s cell programming business demonstrated impressive growth and diversification, as it added 15 new cell programs to its platform, supporting a total of 85 active programs across 43 customers in the same quarter. The foundry revenue for Q3 2022 was recorded as $25 million, a decrease of 29% from Q3 2021, owing to the absence of large milestone payments.

Ginkgo’s R&D expenses increased to $73 million, up from $53 million in the same period of the previous year. The increase was due to the expansion of its Foundry capacity and the broadening of its capabilities to support ongoing and future collaborations. Meanwhile, the general and administrative expenses, excluding stock-based compensation, rose from $29 million in Q3 2021 to $59 million in Q3 2022, reflecting investments in business development, the addition of new customers and programs, increased Foundry activity, the company’s biosecurity offerings, and the demands of being a public company.

The adjusted cash burn rate for 2022 is estimated to be around $270 million, based on my calculations. This figure is supported by the current assets, which provide coverage for over five years, given the current macroeconomic climate and current burn rate. Although there has been an increase in stock-based compensation due to recent acquisitions and restructuring, I have made adjustments to reflect this, and the adjusted figures show signs of improvement. The substantial cash cushion is also a positive factor. Despite these positive indicators, the cost structure still requires attention and I will be monitoring the company’s progress in addressing this issue.

Author’s computations based on Ginkgo financials

Risks

I take this moment to pause and highlight some of the risks that investors should consider before making any decision. The following is not an exhaustive list and interested investors should dive deeper. One such risk is the risk to the company’s reputation in the event that a program goes wrong. This could lead to a loss of trust among stakeholders and harm the company’s financial performance, especially as the company may still need to seek capital from markets.

Another factor for potential investors to keep in mind is the report from Scorpion Capital that accuses Ginkgo of generating fake revenues from its spin-off companies. If this claim is substantiated, it could seriously harm the company’s future prospects for securing financing. This casts doubt on the company’s business dealings. I believe that this question rests in a grey area, but I understand the company’s approach to trying to retain long-term potential from its current deals. Nevertheless, the ultimate decision on whether or not to accept this risk rests with the investor.

Furthermore, Ginkgo has recently undergone a series of acquisitions that require integration, which could present difficulties and associated risks for the company.

Valuations and takeaways

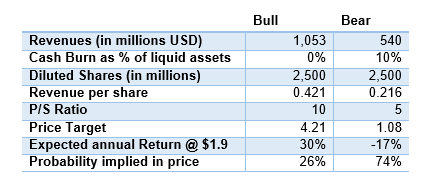

In a previous article, I made a simple model to capture the bull and bear case for this company. I will now proceed by tweaking them. In both scenarios, the growth of revenue and the reduction of cash burn are important factors affecting the company’s worth. The bull scenario predicts strong revenue growth and zero cash burn, which would result in a high P/S ratio of 10. The bear scenario, on the other hand, assumes stagnant revenue and a significant cash burn, leading to a lower P/S ratio of 5. Investors can use this information to evaluate the potential range of the company’s worth.

Author’s computations

This is my updated outlook on the company. I believe that the market is currently underestimating the potential upside of this stock. The company’s sales efforts to standardize its offerings by clearly defining milestones, cost structures, IP terms, and timelines should make it easier to provide quotes to clients and streamline the sales process.

Ginkgo Presentation at JPM 2023

Furthermore, the company can also expand its reach through inside sales, drawing on valuable lessons learned from current programs. These sales efforts will be crucial in breaking into markets that were once dominated by chemical companies, and I believe that the market is currently underestimating this potential.

Be the first to comment