NikkiZalewski/iStock via Getty Images

Investment Overview

In 2022, the S&P 500 lost 16% of its value as almost all sectors of the stock market suffered losses owing to rising interest rates and inflation. Sectors such as technology, communication, and consumer cyclicals suffered losses of >30%, whilst the stand out out-performer was energy, owing to the sanctions imposed on Russia due to the war in Ukraine, which led to rising prices.

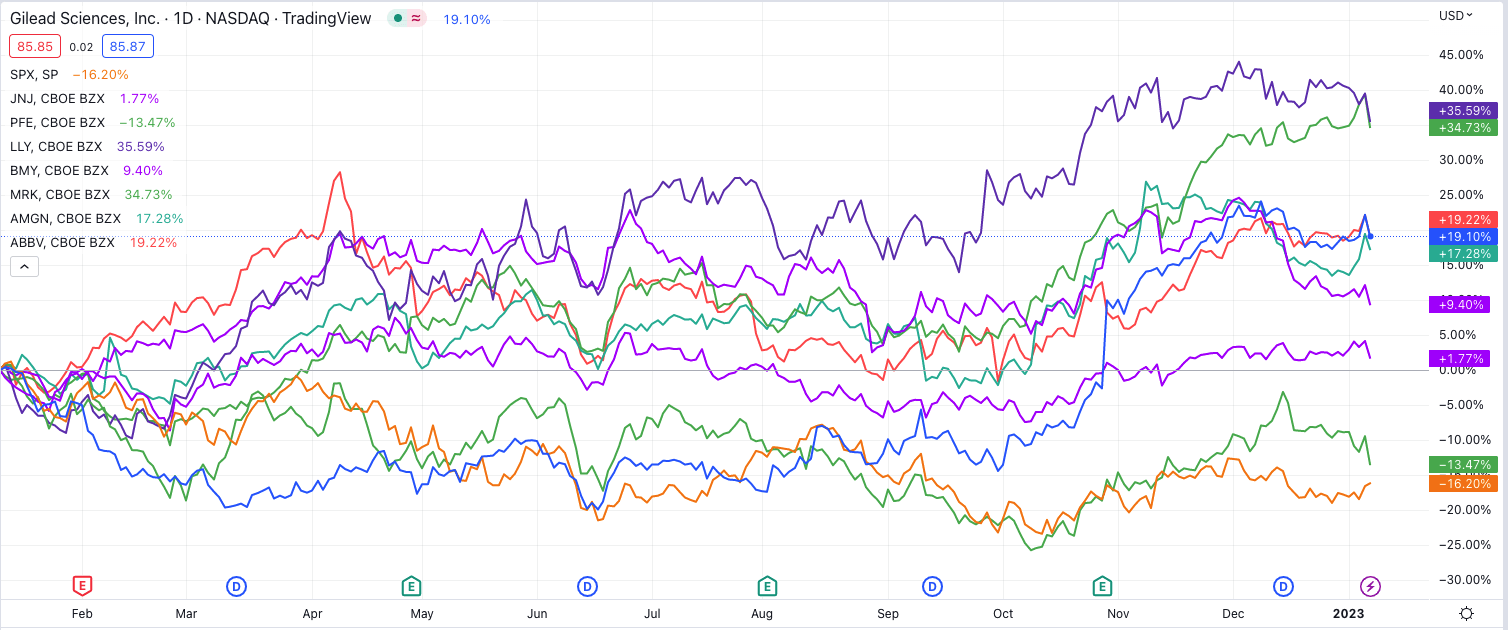

With that said, one segment of the healthcare sector performed well – namely so called “big pharma.” Across 2022, the share prices of what I refer as the “Big 8” US Pharmaceutical companies – Johnson & Johnson (JNJ), Eli Lilly (LLY), AbbVie (ABBV), Pfizer (PFE), Merck & Co (MRK), Bristol Myers Squibb (BMY), Amgen (AMGN), and Gilead Sciences (NASDAQ:GILD) – rose by an average of 15%-plus.

Share price performance of “Big 8” US Pharmas – past 12m (TradingView)

As we can see above, over the past 12 months, only Pfizer shares have fallen in value – by 14%. Eli Lilly and Merck shares rose by the largest amount – both achieved a gain of 35% – but arguably the stand out performer in the second half of 2022 was Gilead Sciences – the subject of this post.

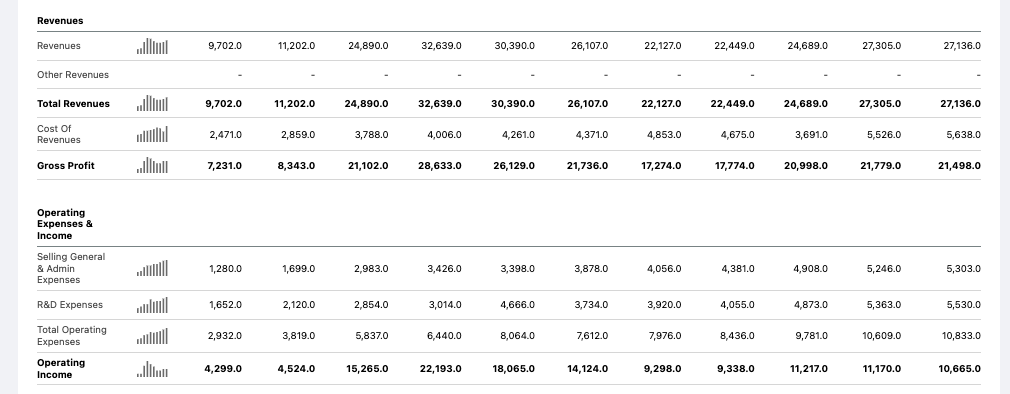

Gilead stock declined in value from $120 per share in 2015 to <$60 by September last year, but subsequently gained 32% in Q422, to trade at $85 per share at the time of writing. The historical losses were due to the decline in sales of Gilead’s Hepatitis C franchise – notably the antiviral drug products Harvoni and Sovaldi.

Both drugs became double-digit billion selling assets in their prime years between 2014 and 2016, before becoming victims of their own success as Hep C patients were functionally cured in a matter of months. As we can see below, as their sales fell, Gilead was initially unable to offset the losses, and its top and bottom line earnings fell in each year between 2015 and 2018, explaining the company’s share price woes.

Gilead income statements historical (Seeking Alpha)

Gilead’s 2018 appointment of a new CEO – Daniel O’Day, who spent three decades at Swiss pharma giant Roche (OTCQX:RHHBY) helping to grow its oncology division into one the industry’s largest – signified that California-headquartered Gilead intended to become an oncology super-power, but several big bets have so far failed to make a meaningful impact on top line revenues.

As I discussed in my last post for Seeking Alpha on Gilead in July, the company spent $12bn acquiring Kite Pharma in 2017, $5bn acquiring anti-CD47 pioneer Forty Seven in 2020, and $21bn acquiring Immunomedics and its promising Trop-2-directed antibody Trodelvy in 2020.

The Kite acquisition has yielded two approved drugs – Yescarta and Tecartus – both cell therapies and indicated respectively for later line large B-cell Lymphoma and Follicular Lymphoma, and relapsed / refractory mantle cell lymphoma and Acute Lymphoblastic Lymphoma.

These are pioneering therapies, with Yescarta a potential blockbuster (>$1bn sales per annum) selling therapy, while Trodelvy – approved to treat metastatic triple-negative breast cancer and urothelial cancer so far, is beginning to win over the doubters thanks to some promising recent data readouts – Trodelvy could one day rival the likes of BMY’s $7bn per annum selling Opdivo, or even Merck’s $17bn per annum selling Keytruda.

These highlights aside, however, the truth is that Gilead has spent almost $40bn on Oncology M&A in recent years, to achieve just over $1.5bn of revenues across the first 9m of 2022. In short, there’s a lot of work still to do before the oncology experiment can be declared successful.

Instead, it has been one of Gilead’s more traditional strengths – its HIV division – that’s primarily driving analysts’ and the market’s recent optimism about the future of the company. Daily oral HIV therapy Biktarvy was first approved in 2018, and sales were up 38% across the first three quarters of 2022, to $7.4bn. The HIV division as a whole posted revenues of $12.4bn across the same period, up 5% year-on-year.

In my July note I provided some rough forward revenue expectations covering the period 2022 – 2030, and used discounted cash flow analysis to try to set a realistic price target for Gilead shares. My target then was $127 per share, which represents a 49% premium to current traded price.

Not only does the US big pharma sector offer outstanding growth prospects, it’s dividend payouts are amongst the most generous of any sector of the stock market. Gilead’s current quarterly dividend payout is currently $0.73 per quarter, which translates to $2.92 per annum, for a yield of 3.4% per annum.

In the remainder of this post I’ll provide my updated forecasts based on recent performance, management guidance, prevailing industry trends, and learnings from CEO O’Day and other members of senior management’s Q&A at the JP Morgan Healthcare conference in San Francisco which took place yesterday.

Recent Performance – Expected Declines in Veklury Sales Shouldn’t Overshadow Impressive Performance

We will have to wait a few weeks before Gilead announces its FY22 earnings and provides guidance for 2023, but strangely for a company whose share price is up >30% across the past three months, Gilead’s revenues fell year-on-year across the first 9m of 2022, and will likely fall again in 2023.

This is down to the falling sales of Veklury, Gilead’s COVID antiviral which has been used to treat hospitalized patients since the beginning of the pandemic. Veklury sales fell from $4.2bn across the first 9m of 2021, to $2.9bn across the same period in 2022, reflecting a fall in the number of hospitalized patients.

The likelihood is that Veklury – which is available in >170 countries and has been administered to ~12m patients, and 60% of all US patients hospitalized with COVID, according to a JPM conference presentation – will experience another, perhaps more significant fall in sales revenues in 2023 as pandemic pressures ease, barring the emergence of a new, more infectious and virulent strain of the virus.

Gilead is working on a new COVID antiviral – candidate GS-5245, an oral therapy which will enter two separate pivotal studies in 2023, in standard risk and high risk patients respectively. It’s therefore not impossible that Gilead’s COVID franchise could flourish again – for context, Pfizer’s COVID antiviral Paxlovid earned >$17bn of revenues in the first 9m of 2022 – but the more realistic outcome is a significant decline in Veklury revenues in 2023, with any approval of the new candidate not likely to take place until 2024.

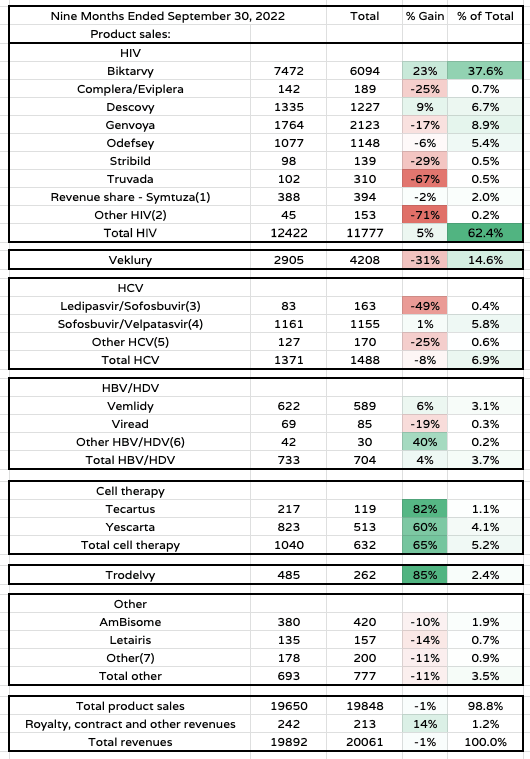

Gilead product sales to Q322 (Gilead Sciences 10Q submission)

Taking a closer look at Gilead’s sales in 2022 to the conclusion of Q3, we can see how falling sales of Veklury will hurt the company going into 2023, given it accounted for 15% of all revenues, but two other things stand out.

Firstly, the performance of the HIV division – a positive where Biktarvy is concerned, although its ~38% share of all revenues arguably puts too much pressure on the performance of a single asset for investor’s liking.

Secondly, the strong growth within the cell therapy and oncology divisions. Admittedly, Gilead is starting from scratch in oncology, with only three approved products – for context, Bristol Myers Squibb markets and sells 9 major oncology products, which will likely drive >$17bn revenues in 2022 – but an average growth of 73% between Tecartus, Yescarta, and Trodelvy sends a strong message and may be repeated in 2023 as all 3 products are a long way from meeting peak sales expectations.

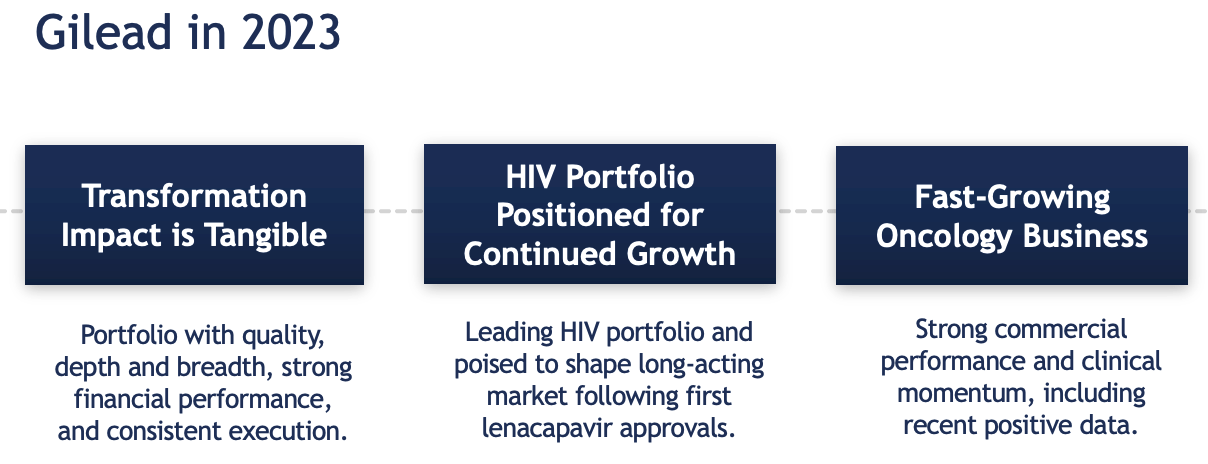

Although several other divisions – Hepatitis C and B – and products – HIV therapies Descovy and Genvoya, for example – make meaningful contributions to Gilead’s business, investors should be in no doubt that HIV and Oncology represent the future for Gilead, as stated in the very first slide from the accompanying presentation for yesterday’s JPM Q&A.

Gilead in 2023 (Slide from JPM Healthcare presentation)

Before moving on to look at sales projections for both Gilead’s product portfolio and pipeline, it’s also worth noting the phenomenal profitability of the big pharma industry – and the fact that Gilead is no exception.

key investment analysis ratios of Big 8 Pharmas compared (data collected from TradingView, Google Finance)

The above table compares key investment ratios of the “Big 8” US pharmas and as we can see, all 8 drive net profit margins >15%. All except Eli Lilly have price to earnings ratios <25x, and price to sales ratios <6x, and all 8 Pharmas have a net profit margin >15%.

That represents extremely strong performance for any sector of the stock market and means that pharma’s typically drive exceptionally strong cash flow, which is what allows them to make huge bets on M&A – i.e. the ~$40bn Gilead has spent acquiring a handful of promising molecules through biotech acquisitions – while at the same time rewarding investors with attractive dividends, and completing share buybacks – Gilead management says it repurchased $1.4bn of stock in 2022, with $800m completed in Q422 alone.

With that said, most pharmas also take on relatively high levels of debt – a great way to raise funds when interest rates are low, but higher risk when rates are climbing, as investors will demand a higher yield on their investment. Gilead reported $13.6bn of current assets as of Q322, balanced against $10.4bn of current liabilities, and long-term debt of ~$23bn.

By big pharma standards, Gilead’s debt to equity ratio of 120% is far from the worst amongst the “Big 8,” and therefore not something investors ought to be too concerned about, although as mentioned, rising interest rates may check some of Gilead’s price momentum in 2023.

Gilead Sales Projections To 2030 – Product and Pipeline

The last time I completed forward revenue analysis and discounted cash flow analysis for Gilead, my price target was $127, based on the company achieving revenues of ~$43bn by 2030, at a CAGR of 8.7%. Today, I’m less optimistic about that revenue target, revising it downward substantially, although I still believe Gilead’s shares could be as much as 25% undervalued.

During the Q&A section of Gilead’s JPM Healthcare conference presentation management were continually pressed to provide some forward revenue projections – most frequently in oncology and HIV – but declined to do so.

Although FY23 guidance will doubtless be provided when Gilead’s announces FY22 earnings, likely in March, management are unlikely to provide forward revenue projections for each drug product, and certainly not to 2030.

In order to establish a price target for the company I believe this type of modeling is essential – I have compiled the following tables using all of the data and research at my disposal – management and analyst guidance, competitive threats, prevailing economic conditions, historical performance, and some of my own assumptions based on my independent research.

I will break the tables down for readers by division, and highlight where I have made revisions to my last set of forecasts shared back in July.

HIV Division

Gilead HIV division projected revenues to 2030 (my calculations and assumptions)

Beginning with HIV, it’s no secret that Gilead views Biktarvy and Lenacapavir as its key revenue generating assets.

Lenacapavir was finally approved in December 2022 after some frustrating delays, including an initial FDA rejection – in March last year – on Chemistry, Manufacturing and Control grounds, related to the FDA’s belief that vials containing the drug, made from borosilicate, could interact with the drug creating glass particles.

Gilead duly rectified the issue and now Lenacapavir – which will be marketed and sold as Sunlenca in the US, and which has already been approved in the UK, Europe, and Canada, becomes the first-ever capsid inhibitor-based HIV therapy, administered only twice per year.

In July I forecast Lenacapavir to achieve $2bn in peak sales, but this time – based on the drug’s ability to expand its label into fields such as Pre-exposure prophylaxis (“PrEP”), and in combo with other therapies – most notably Merck’s islatravir – I have opted to use a more optimistic projection of $4bn in peak sales by 2030 – the same figure as analysts at RBC Capital Markets.

Sunlenca does have a rival of significance – GlaxoSmithKline’s (GSK) recently approved Cabenuva – but Cabenuva must be administered every month, and has a marginally higher price point of $40 – $50k per annum, compared to Sunlenca, which will cost $42k in its first year of use and $39k per annum thereafter, according to Evaluate Pharma.

CEO O’Day discussed Sunlenca at JPM yesterday, commenting:

I think this is really the best of Gilead really shining through. This is a result of our own research and development, first in-kind medicine, 16 years of innovation, more than 4,000 compounds screened and a truly unique molecule.

It’s clear that Gilead has great confidence in Lenacapavir, although the label expansions are essential to the success of the drug. As we can see below, Gilead has multiple studies ongoing with other HIV drugs it has developed in-house.

Gilead’s focus on long-acting HIV therapies (JPM Conference presentation)

These studies will likely not complete for 1/2 more years, hence I would expect any major revenue growth to occur later this decade. Lenacapavir is absolutely central to Gilead’s future and I’m giving management the benefit of the doubt and projecting $5bn in peak sales in 2030. If the drug succeeds in PrEP, for example, Gilead believes only ~25% of patients are accessing this medicine that could benefit from it.

Moving to Biktarvy – the only asset, perhaps besides Trodelvy that’s more central to Gilead’s success or failure – there’s no question that Biktarvy is the standard-of-care in HIV – management told analysts at JPM that the drug enjoys a 45% market share, and growing. Gilead’s Chief Commercial Officer Johanna Mercier told the audience that:

…Biktarvy is at a 45% market share in the U.S. We have been growing on a year-on-year basis, about 4%, so about 1% or a little less than 1% per quarter-over-quarter. And we do believe that there’s still an opportunity for growth with Biktarvy. We believe that because of its profile and what it offers for this patient population, we do believe that there is still room for growth in ’23 and beyond in the oral market.

In 2023, I anticipate Biktarvy will deliver ~16% year-on-year growth, but after that I have opted for a more conservative 2.5% CAGR. That means I no longer view Biktarvy as having $15bn peak sales potential, although $13.5bn sales in 2030 would still make Biktarvy one of the world’s best-selling drugs.

Gilead seems to be trying to find ways to combine Sunlenca and Biktarvy and repeat its success with Hepatitis C, by creating a functional cure for HIV. That’s a tremendously exciting prospect, and a very good reason for backing the company notwithstanding its share price performance.

I may have been somewhat harsh with my forward revenue projections for the remaining assets in Gilead’s HIV division, although I have highlighted in red in the table where patent expiries occur, and most assets will go off patent in the next few years, which will result in rapidly falling sales as generic competitors enter these markets.

The beauty for both Biktarvy and Lenacapvir is that they will not go off patent this decade, so Gilead is very likely to be the dominant player in HIV for the foreseeable future – few pharmas can boast such dominance of a lucrative field of treatment, and such strong protection from generic competition.

Oncology Division

The reality for Gilead is that its oncology division is a long way from matching the pre-eminence of its HIV division – but if Gilead’s execution matches its ambition then success certainly beckons.

Gilead acquired Immunomedics for $21bn purely to gain access to Trodelvy, and the drug got off to the worst possible start, with management accepting a $2.7bn write-down last year owing to its delayed approval in breast cancer.

CEO O’Day has defended the drug however, explaining that Gilead’s strategy with Trodelvy has been to work from the outside in i.e. beginning with approvals in later line stages of therapy and working towards approvals in more lucrative early lines.

Perhaps O’Day’s strategy will eventually pay off – Trodelvy cut the risk of death by 49% versus chemotherapy in its pivotal study in third line, metastatic triple negative breast cancer (“TNBC”), which led to the FDA approving the drug as a second line therapy.

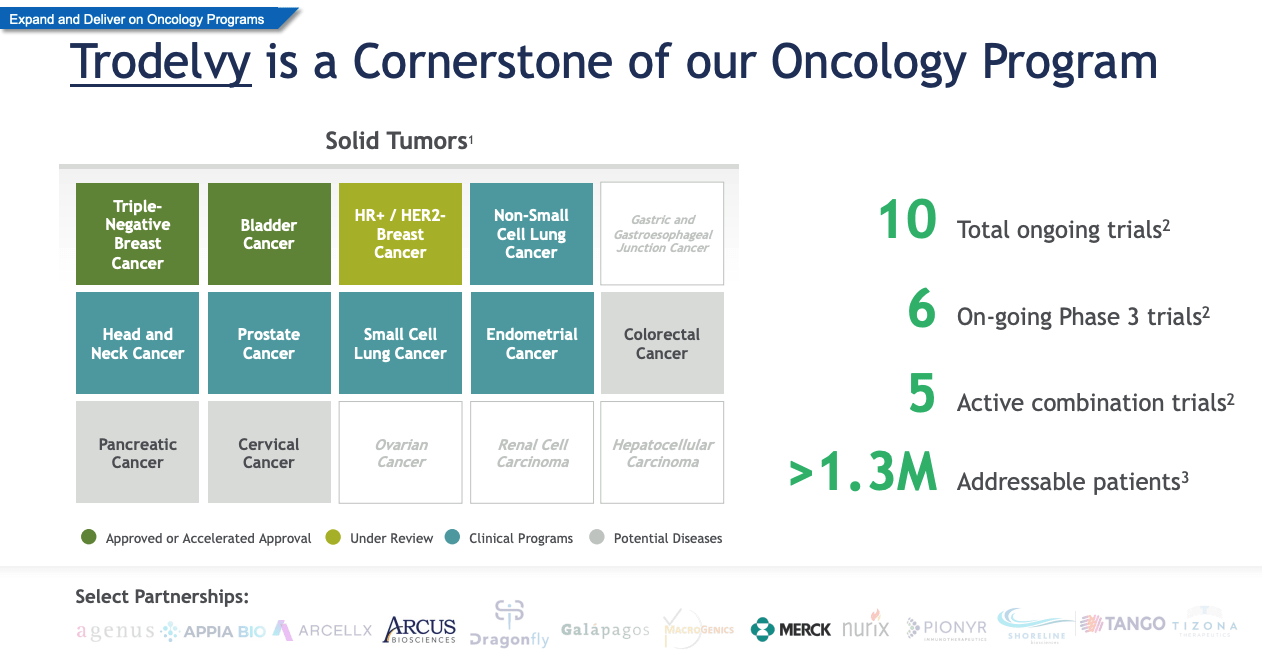

Trodelvy cornerstone of Gilead’s Oncology Program (JPM Conference presentation)

The approval in bladder cancer was another positive although O’Day revealed yesterday that 90% of the drug’s sales are in TNBC. As we can see above, further expansion opportunities are plentiful – at least if you listen to O’Day who told the JPM Conference yesterday:

It’s, again, hard to overemphasize the potential here because of the expression of TROP2 across so many tumor types.

With a Prescription Drug User Fee Act (“PDUFA”) date arriving in less than one month for Trodelvy in hormone receptor positive/HER2 negative breast cancer, O’Day also pointed out that the drug could become the first antibody drug conjugate (“ADC”), that works in patients regardless of HER2 status.

Analysts have suggested that Trodelvy could drive up to $5bn in peak sales in breast cancer, but lung is the next major target for O’Day, who let’s not forget spent more than 30 years helping turn Roche into an oncology super-power.

While3 Gilead believes it’s total addressable market (“TAM”) for Trodelvy in breast cancer is ~700k patients, that could double to ~1.3m patients if Gilead can make breakthroughs in lung, and to lesser extent, prostate, head and neck and endometrial cancers.

There’s some significant uncertainty here, however, with certain markets contingent upon approvals of Gilead’s other drugs, such as Magrolimab, the anti-CD47 therapeutic. That’s why, although I have upgraded my growth expectations to 50% in 2023 versus 2022, or sales of $970m, I am maintaining my prior forecast of 35% in each subsequent year to 2030.

That gives me a peak sales projection in 2030 of $8bn, which puts Trodelvy on a par with BMY’s immune checkpoint inhibitor Opdivo, but I’m stopping short of proclaiming Trodelvy to be the next Keytruda, Merck’s $17bn per annum selling ICI. There is a long road ahead, but there are increasingly clear grounds for optimism.

If Gilead faced a real challenge to guide Trodelvy through the clinical process and get the data it needed, it arguably faces an even greater challenge with Magrolimab, and its TIGIT program, in which Gilead partners with Arcus Biosciences.

TIGIT is a controversial drug target to say the least. Gilead’s intention is to use its TIGIT therapy alongside Arcus’ Zimberelimab – a PD-1 inhibiting ICI – to try to improve its performance. O’Day insists that Gilead has:

The largest body of evidence on TIGIT that has been communicated so far to date

Phase 3 studies in Non-Small Cell Lung Cancer (“NSCLC”) are underway, but issues remain. Is Zimberelimab as effective a drug as e.g. Opdivo or Keytruda? And will the addition of the anti-TIGIT Domvanalimab provide a statistically significant improvement in efficacy? Magrolimab faces challenges also, with studies foundering in both blood cancers and solid tumors.

As such, I have reduced my peak sales targets for Magrolimab from $4bn in 2030, by half to $2bn, and reduced my target for Domvanalimab / Zimberelimab to $1.5bn.

In cell therapy, where Gilead was a first mover, but now faces competition from the likes of BMY and Legend Biotech (LEGN) / Johnson & Johnson, I have reduced peak sales targets for Yescarta to $1.5bn, from $1.75bn, and reduced expectations for the remaining Kite assets, targeting CD19 and CD20, from $2bn, to $1bn.

Gilead oncology revenue forecasts (my assumptions)

To summarize, my projections support the thesis that Gilead can make a success of Trodelvy, and a qualified success with Magrolimab, Dom / Zim, and the remaining cell therapy programs. I have the oncology divisions growing revenues at a CAGR of 24%, and delivering revenues of $13.7bn by 2030. I’m aware that is an ambitious target, and will test the CEO’s capabilities to the limit.

Remaining Portfolio Assets

In my last note I suggested that Jyseleca, in autoimmune, and Cilofexor, in nonalcoholic steatohepatitis (“NASH”), could earn Gilead $2bn of revenues each. These assets are part of Gilead’s ~$5bn collaboration with Galapagos and Jyseleca – a JAK inhibitor – has been approved in Europe and is targeting approval in Crohn’s Disease in the US. Autoimmune is a highly competitive space however in which Gilead has little “skin in the game,” and a NASH approval for Cilofexor is a long shot. I have therefore assigned peak 2030 revenue figures for each asset of $500m in my revised forecasts.

Gilead Other Products, NASH and Autoimmune revenue projections (my table and assumptions)

Likewise, I’m slashing Veklury revenues to $2bn in 2023, $1bn in 2024 and reducing revenues expectation by 50% per annum subsequently. I’m also reducing my expectations for sales of Vemlidy based on slowing growth in 2022, increasing revenues by 10% per annum, as opposed to 20%, until patent expiration in 2027 sees sales fall by 20% per annum.

The FDA declined to approve Hepcludex in October last year, although I still anticipate an approval for the Hep B therapy – already approved in Europe – in 2023, whilst cutting peak sales from $750m, to $500m. I also include an approval for the new oral COVID antiviral GS-5245 in 2024, with sales growing from $750m in that year, to $1bn by 2030. The therapy could be a surprise hot for Gilead, given the threat of COVID remains high.

COVID / HCV / HBV revenues projections (my assumptions and table)

Conclusion – Gilead’s Momentum May Be Checked Slightly In 2023 But I Remain Optimistic

Having completed my sales projections I plus them into a forward income statement as follows:

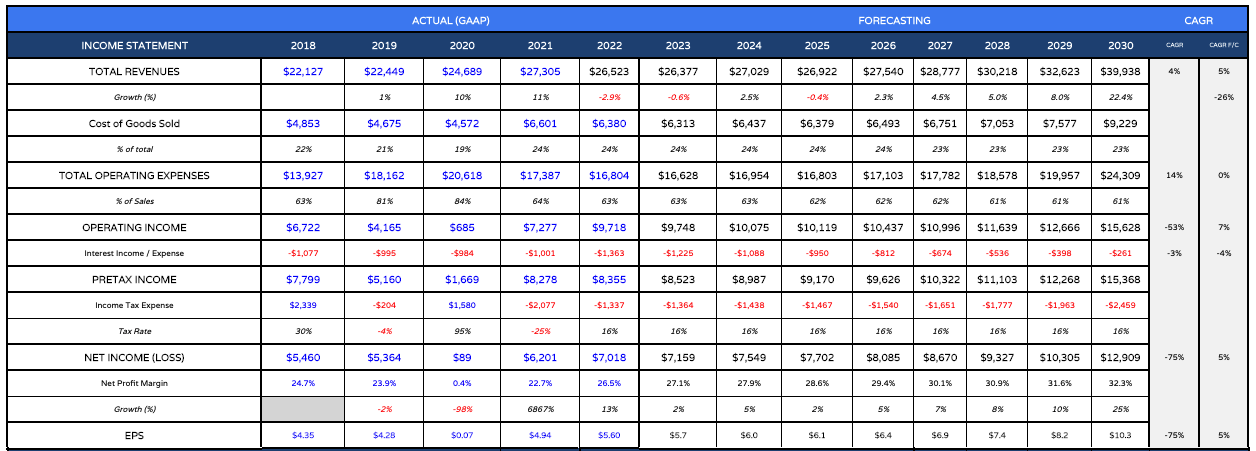

Gilead Sciences forward income statement (my table and assumptions)

As we can see, compared to July, when I forecast for revenues of $43bn by 2030, I’m now taking a more conservative outlook, forecasting revenues of $39bn in that year. This reflects Gilead’s clear focus on its HIV and Oncology divisions, and dwindling interest in some other areas. Within these divisions, the progress of Biktarvy, Lenacapavir, and Troveldy are absolutely key to Gilead’s future success, or otherwise.

Within oncology, Magrolimab, and Domvanalimab / Zimberelimab still have key roles to play, even if only in combo with Trodelvy, while I’m slightly more sceptical about prospects for cell therapy assets, particularly given the emergence of Personalized Cancer Vaccines, developed by the MRNA giants Moderna (MRNA) and BioNTech (BNTX), which may make it into the more lucrative solid tumor market ahead before cell therapies do, restricting their revenue potential.

Gilead sciences discounted cash flow analysis (my table and assumptions)

Finally, as shown above, I present my discounted cash flow analysis. My target price using DCF analysis has not changed excessively, being $103, but for the Ebitda multiple I have reduced the multiple from 14.5, to 12x, based on my expected 2022 EBIT figure.

My final price target for Gilead stock in 2023 is therefore the average of DCF / EBITDA multiple, which is $112 per share. I do expect Gilead’s momentum to be checked somewhat in 2023 thanks interest rate tailwinds, falling sales of Veklury, and owing to some of the difficulties I expect the company to have developing its oncology franchise after its $40bn M&A spree.

$112 per share remains a very attractive 29% premium to current traded price, however, and I would still recommend Gilead as a good investment based on my research into the pharma’s long-term prospects.

Naturally, there are so many moving parts involved in creating forecasting for a company as large as Gilead that valuations, price targets and forward revenues projections are subject to near constant change. As a general guide to Gilead’s pipeline and products, however, I hope readers find this analysis useful.

Ultimately, my gut feeling on Gilead is that its key HIV divisions can remain strong for the remainder of the decade with no patent cliffs in play, but the key to continuing momentum is the oncology division.

CEO O’Day makes a persuasive case for Trodelvy, and even TIGIT and CD47 as targets, which many observers may disagree with. O’Day was brought in to create a thriving oncology division, and if he succeeds, Gilead and its shareholders will succeed.

By the end of 2023, we may have a much clearer picture of how the key programs are progressing, and given Gilead does not intend to pursue any more M&A deals, and the bets have already been made, success must come from the current portfolio and pipeline.

It ought to be fascinating to see how matters play out, and I look forward to providing updated analysis once we have Q422 earnings, and FY23 guidance, in a couple of months’ time.

Be the first to comment