kzenon/iStock via Getty Images

Description

Investors should hold off any purchase of GFL Environmental (NYSE:GFL) until valuation becomes more attractive. Given that we are in the pretty volatile “investing” environment, I believe there will definitely be opportunities. Technicalities aside, GFL has a solid business that operates in a very attractive industry with high barriers to entry. Layering on top of that is GFL ability to continuously conduct value accretive deals to enhance growth and market positioning. I believe with the right valuation GFL would be a very attractive long.

Company overview

GFL provides waste management services. Services provided by GFL include the identification of hazardous and nonhazardous liquid waste, their collection, transportation, processing, recycling, and disposal.

GFL focused verticals are all very attractive

Solid waste

The solid waste industry is highly defensive and recession resistant due to the critical nature of its services in ensuring public health and safety through adequate waste collection and disposal. Firstly, waste generation from homeowners and businesses is consistent and predictable, which results in high revenue visibility. Additionally, some customers have signed multi-year contracts that include yearly Inflation-pegged and fuel adjustments. Secondly, pricing rates are relatively inelastic to recessions, while waste volume growth is highly stable organically strongly linked to population and GDP growth. Thirdly, there are no viable alternatives to collection and landfill disposal that are also cost-effective. Last but not least, and in my opinion most importantly, new market entrant prospects are constrained by geographic, regulatory, environmental, and substantial capex. Such competitive characteristics are compounded by the difficulty in establishing route density and by vertical integration, wherein businesses control the entire value chain.

Infrastructure and Soil Remediation

Extreme specialization characterizes the North American infrastructure and soil remediation industry, leaving only a handful of significant competitors in each region where GFL conducts relevant business. This is a business sector with very high entry barriers. Companies that deal with soil remediation or disposal must go through a lengthy and expensive permitting process to legally operate in the industry. Also, given the seriousness of the problem, I anticipate that regulators in the Canadian and American markets will continue to tighten up on the standards they use to control soil contaminants.

Liquid waste

Liquid waste management is subject to stringent regulations from government agencies, just like solid waste management, infrastructure & soil remediation. In other words, there is also high barriers to entry.

Large strategic network of facilities

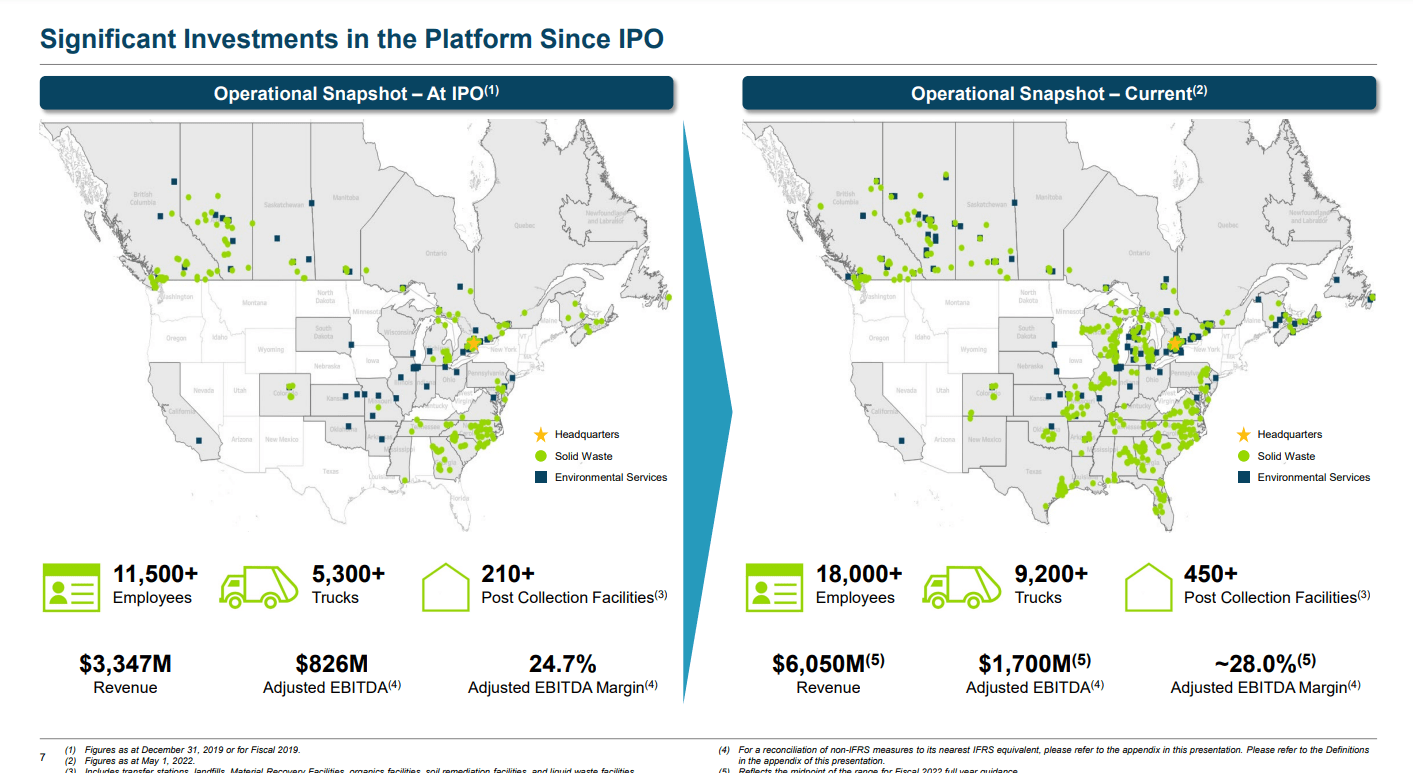

GFL’s services are available through a spread-out network of facilities in both the primary and secondary markets of the United States and Canada. There are more than 450 post collection facilities in the GFL network as of May 2022, and a total of more than 9,000 trucks serving its service areas. I believe GFL’s strong competitive position is backed by the substantial capital investment needed to reconstruct the underlying network of assets, route density, and compliance to regulatory requirements compared to smaller, more conventional competitors, I believe that GFL’s size and scale provide a unique and substantial competitive advantage.

May 2022 investor day

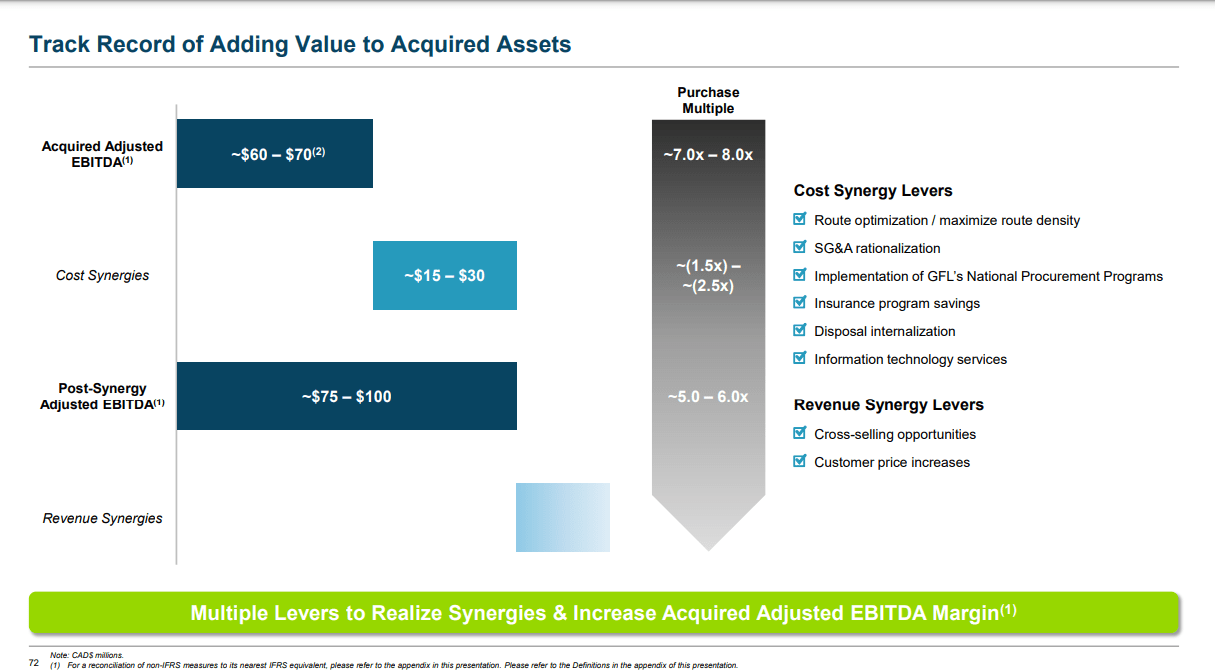

In addition, GFL is capable of efficiently handling the waste volumes it is responsible for thanks to its vast network of facilities serving different markets with different disposal methods. GFL’s vertically integrated model handles the entire waste management process for its customers, beginning with collection and ending with disposal, in certain markets (aka internalization). Thanks to this, I believe GFL is able to enjoy a predictable recurring flow revenue, and also maximize profits from operations. When GFL has control over large volumes of solid waste, it can also use this volume to negotiate favorable terms with 3P disposal facilities or whoever excess landfill capacity. In my opinion, this is why GFL has been able to consistently produce high levels of free cash flow despite the fact that its operations mix relies less on the development of owned landfills.

Finally, I believe GFL has amassed a highly desirable collection of facilities, particularly in markets where they are well to quickly and effectively meet their requirements.

Good track record of M&A

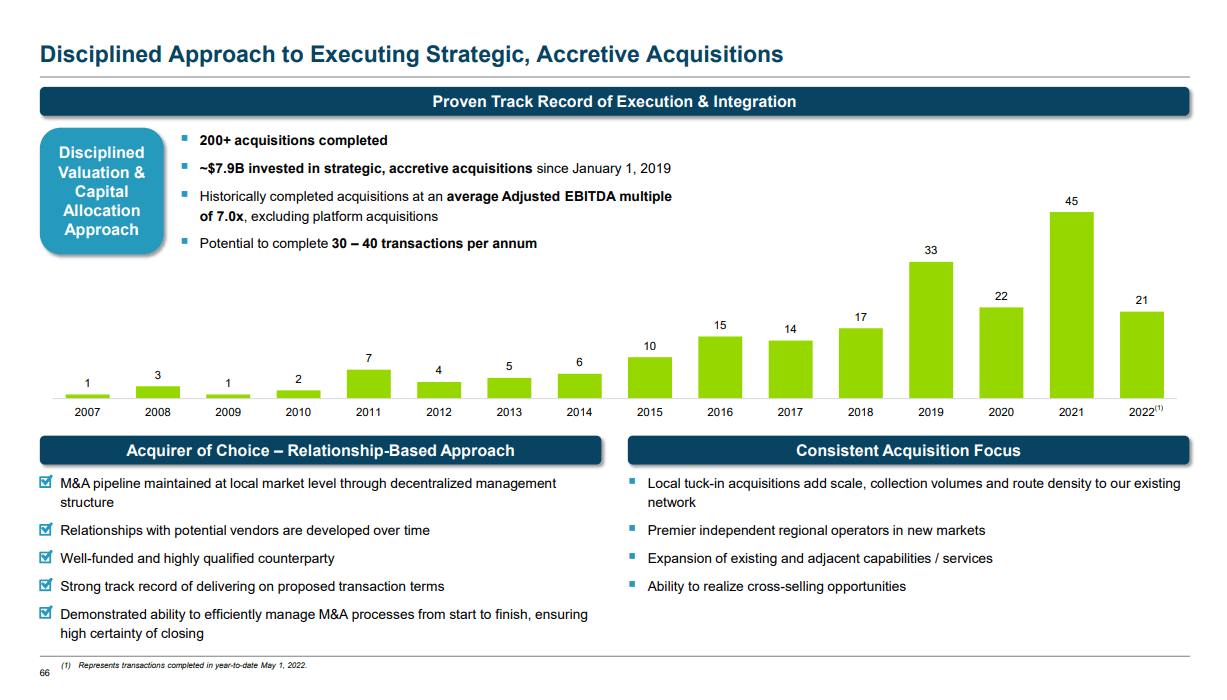

One could characterize GFL as a shrewd dealmaker. Growth at GFL can be attributed in large part to the company’s disciplined approach to acquiring businesses that can add value. The criteria they use for making mergers and acquisitions are strategic and well-considered, in my opinion. With a focus on establishing a foothold in untapped markets, GFL seeks to acquire leading independent regional operators. They plan to grow by acquiring smaller companies, or “tuck-ins,” and integrating them into their larger operations so that they can achieve scale through increased route density and resulting cost synergies, as well as margin expansion through the use of its infrastructure and centralized back-end management systems. In my opinion, this is a classic strategy, given the impracticality (in terms of time and money) of establishing an operation in the new regions (as mentioned above) without first clearing a number of substantial regulatory hurdles.

GFL has been in business since 2007, and during that time it has made over a hundred acquisitions. In addition, GFL has demonstrated its ability to successfully execute large-scale platform acquisitions through its completion of the Waste Industries Merger and its acquisitions of solid waste operations in Eastern Canada and Michigan. To reiterate what was said above, the strategic nature of these acquisitions is evident when considering the fact that they allowed GFL to enter new markets, realize cross-selling opportunities, and achieve cost synergies across the board.

I believe M&A will always be on the table for GFL to enhance its growth in the future, and I look forward to it.

May 2022 investor day

May 2022 investor day

Outlook provided by management is good

GFL maintained its EBITDA guidance in 3Q22 earnings despite significant recycling headwinds, and prices remain well above inflation, which I expect to accelerate into 2023. Regarding the skepticism regarding its high leverage, I think the substantial discount in valuation relative to its competitors more than makes up for this. Even though the company’s leverage is higher than its peers’, I have no reason to be concerned because the business model is inherently recession-resistant because price increases will more than make up for any declines in volume.

While I anticipate GFL’s deleveraging to occur organically over time as EBITDA expands, I also think that there is the possibility of expedited deleveraging through asset sales (which will help with closing valuation gap).

Valuation

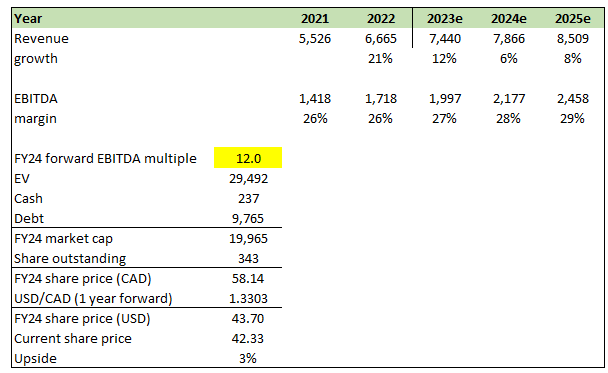

Everything is fine, except that the valuation has already factored in all of the good things I mentioned above. Since the 3Q22 earnings, GFL’s share price and valuation have both increased. As a result, I believe the stock is fairly priced.

My model is based on FY23 guidance from management, consensus estimates for the next few years, and a forward USD/CAD FX rate. GFL revenue should benefit this year from landfill gas and a robust pricing outlook (which is higher in FY23), followed by GDP+X% growth. Margin should improve naturally as GFL continues to grow.

Own estimates

Key risks

High debt

The debt load at GFL is substantial. It’s possible that the company’s path to profitability will be slowed or even derailed by the interest payments and principal payments associated with its high debt load. Also, GFL leverage may restrict its capacity to pursue larger M&A.

Lower M&A deals available

The rate of growth could be affected if the number of deals that are ultimately closed drops for any number of reasons. Potential synergies could also be lower than anticipated if GFL fails to successfully integrate companies it has acquired.

Summary

Investors should wait until the price is more reasonable before making a purchase. Despite the current unpredictability of the “investing” climate, I am confident that opportunities will present themselves. Forget the nitpicking, GFL runs a solid business in a lucrative sector with high barriers to entry. Adding to that is GFL’s capacity to sustainably engage in value-accretive deals that boost expansion and market standing. I think GFL would be a great long at the right price.

Be the first to comment