Sjo

Lessons learned from our investment history with GTT

We’ve been following Gaztransport & Technigaz SA (OTCPK:GZPZY) (OTCPK:GZPZF) for quite some time, dating back to 2015. Back then, we had just established ourselves up as a family office and investment manager, and GTT, as it is commonly referred to, was one of the very first companies we analyzed in depth and considered as an investment.

We soon became highly impressed by GTT’s dominant position in a niche market, as well as its unique business model of licensing of its technologies instead of in-house or partially outsourced production, which leads to extremely attractive business fundamentals – including high profitability levels, a very light asset base, and a structurally negative working capital requirement. We also clearly saw the growth potential of Liquefied Natural Gas (LNG) in the global energy mix for decades to come, and therefore the growth in demand for GTT’s products and services.

The stock price had been declining meaningfully throughout the second half of 2015, valuation had become quite attractive, and in late December that year we decided to make our first purchase and acquire a participation in the company. The price was EUR 38.5 per share. Delighted at having made one of our very first active investment, we then proceeded to watch the stock fall precipitously over the following two months.

As many will recall, this was a time during which the global energy complex was going through some significant turbulence, with the signing of the U.N. climate agreement in Paris, and the Saudi-led move to have OPEC reduce oil prices short-term in an effort to preserve its market share. As a result, crude oil prices fell as low as USD 25 per barrel in early 2016, and energy stocks were indiscriminately battered in the process.

Google Finance

So barely over a month following our initial investment in GTT, the stock price had declined to EUR 22.5, down a massive 42% from our purchase price. We’d be lying if we said that the magnitude and rapidity of the drawdown didn’t have an impact on our psychology. We were quite badly shaken, and so methodically went back over our work to try to ascertain whether our investment thesis was flawed, or whether we were just suffering the brunt of negative yet likely transitory events.

We became increasingly convinced that despite the high level of cyclicality that could be expected, GTT’s long-term prospects remained intact, and that the valuation of the company had become incredibly cheap, as it was now trading at a forward PE multiple of about 6x earnings estimates for 2016. This, together with the firm’s pristine balance sheet, gave us the conviction to continue to accumulate shares at very depressed prices in January and February of 2016.

This is the part that we did well. We remained disciplined in following our investment process, a function of which is to prevent us from the temptation of letting emotions get the better of us, and sell our stake in a panic for example. Instead, we more than doubled-down on our initial investment, reducing our average buying price meaningfully in the process.

The mistakes started shortly thereafter. Of course, it is easy to say this in hindsight, yet we feel that it is crucial to revisit past investment decisions, and try to assess what deductions could have or should have been made from the observable facts as they were at the time. Only then can one learn from his or her accumulated investment experience. We hope others might benefit too, just from hearing the tale.

In short, the mistake we made was reducing and eventually divesting of our entire stake in GTT over the following two years, which represented an uncharacteristically short holding period by our standards. A number of considerations motivated these decisions, or so we thought. The company’s stock price had more than doubled from its lows, as the energy complex gradually stabilized and fundamentals improved. As a result, the forward PE multiple had expanded into the mid- to high-teens, arguably a fair PE multiple for GTT. The size of our position, relative to other investments, had become quite large. Last but not least, we had made a decent, although unspectacular, total return on our investment in GTT.

All of these are reasonable grounds to consider trimming or selling an investment. But what became more clearly visible with the benefit of hindsight is that these considerations weren’t the main motivation behind our decisions to sell. Instead, there was a far more powerful subliminal force at work. (Here I’m going to switch to the singular form, as this is a mistake I need to own up to personally, not the rest of the team): I was suffering from a severe case of ‘loss aversion’. I felt psychologically scarred from the previous massive drawdown in the stock price, and without consciously being aware of it, I wanted to terminate my association with this investment, and proceeded to look for every good reason to do so (i.e. ‘confirmation bias’). In reference to Seth Klarman’s famous extract in Margin of Safety, I let my behavioral biases make me confound what was effectively an ‘eating sardine’ for a ‘trading sardine’!

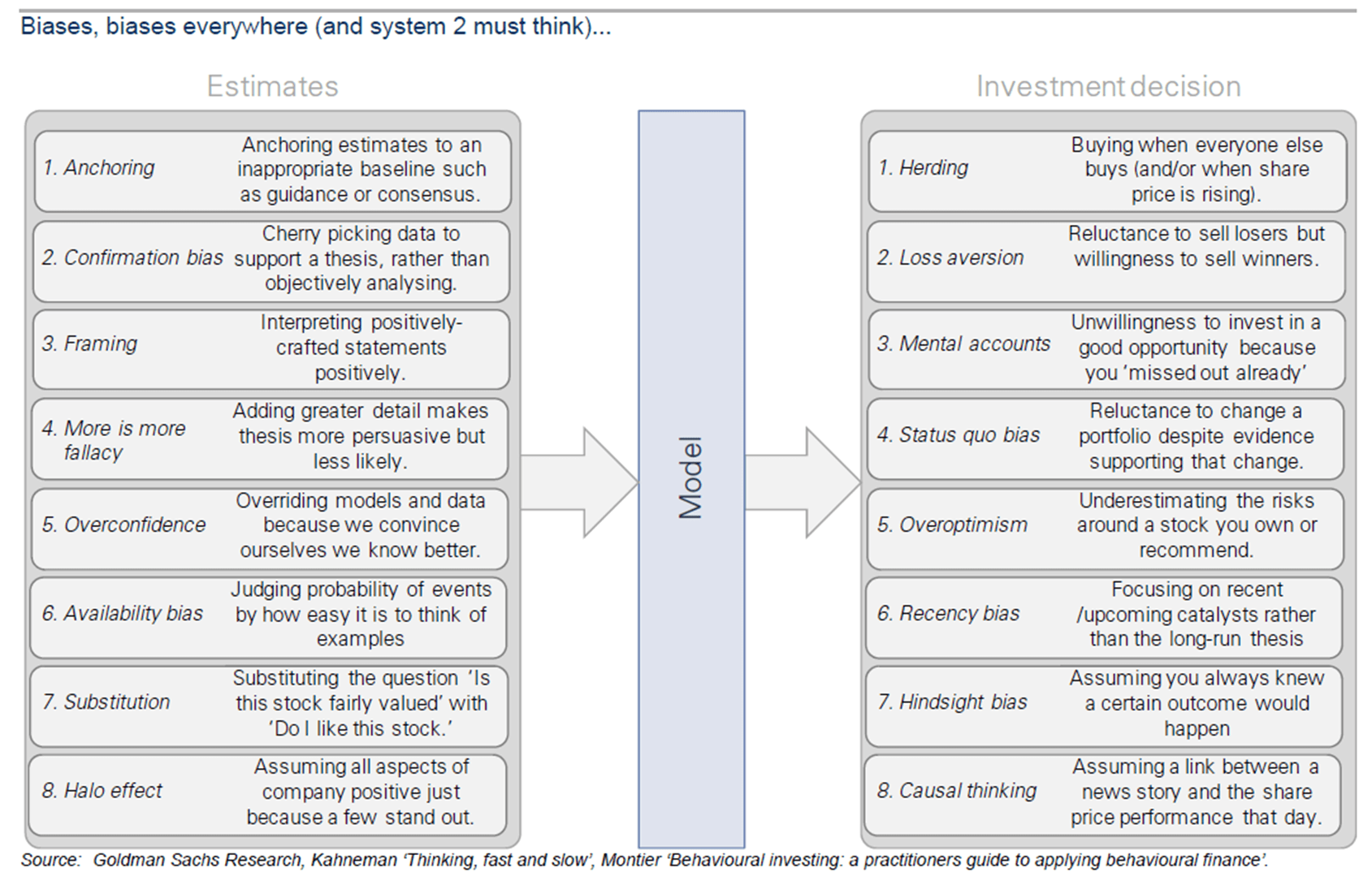

The lesson has since been well learned. For investors such as ourselves, it makes sense to be keenly aware of one’s behavioral biases (see Appendix for a graphic summary of some of the main ones), and employ a structured investment process that aims to negate such biases as best as possible – instead focusing on long-term business fundamentals and the deployment of capital at sensible prices.

As time went by, the realization gradually sank in that I had made a colossal mistake in treating GTT’s stock as a ‘trading sardine’. I also eventually came to better understand why I had made that mistake. We continued following the company’s growth and strategic evolution, and were determined to own the company once again, should the opportunity present itself. We wrote an initial Seeking Alpha article on GTT in early 2021, which mainly covered the company’s historical background, the competitive landscape, and business fundamentals. We encourage those interested in GTT to read it, as we’ll not be reiterating much of what was already outlined there in this article. Instead, we’d like to focus on the recent developments in business fundamentals over the past two years.

Business developments over the recent past

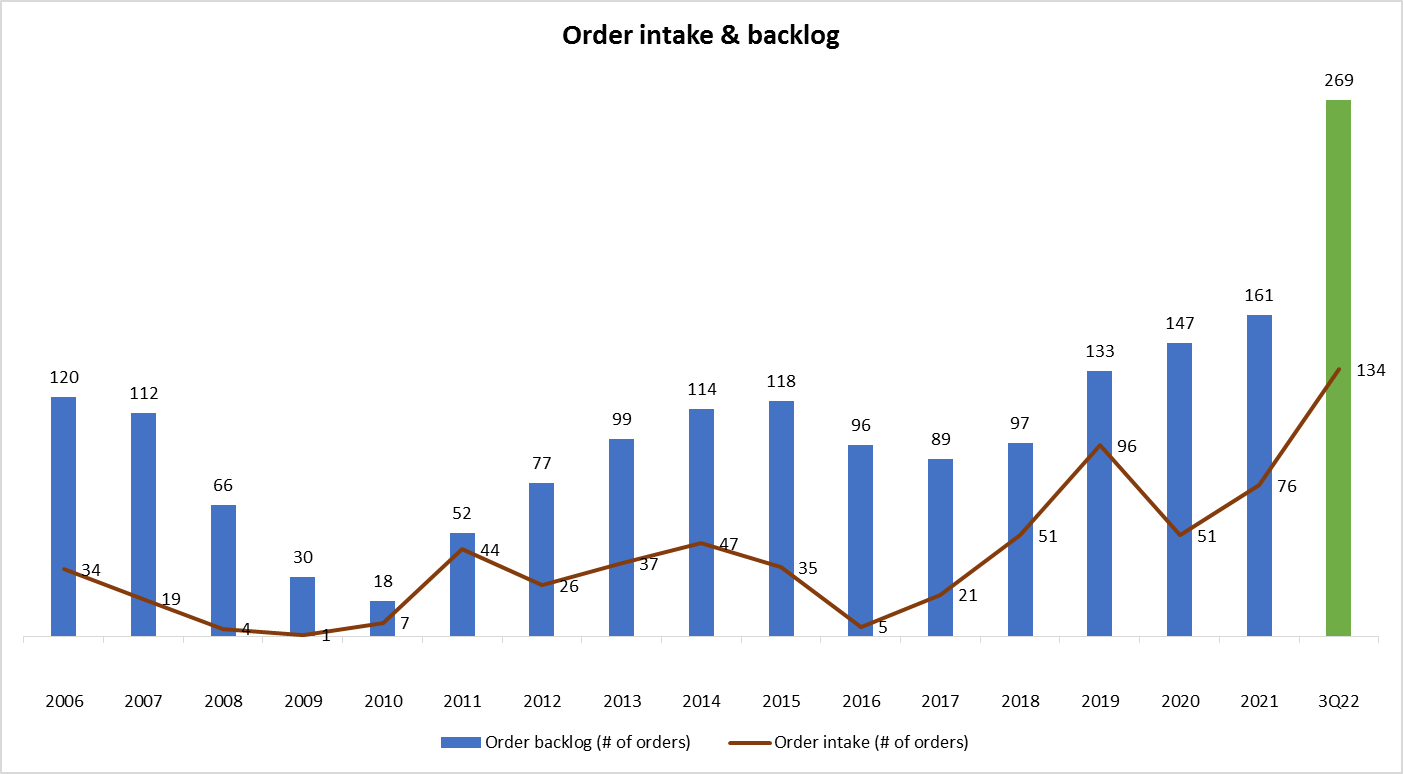

Let’s first take a look at the evolution in GTT’s order intake and backlog. As shown below, the turbulence of late 2015 did have a material impact on order intake, which fell massively in 2016. However, the firm’s large order book – with lead times of approximately three years – enabled it to sail through these troubled waters without any significant issues. Order intake then recovered and gradually accelerated between 2016 and 2019, reaching a record intake of 96 orders that year. Then Covid hit, which once again disrupted the market amidst uncertain conditions, although the book-to-bill ratio remained firmly above 1x, and the backlog thus continued to grow. Which was followed by the start of the armed conflict in Ukraine in early 2022. As everyone is aware, these events massively disrupted the energy complex, and especially natural gas, to the benefit of LNG, which is the only way to transport gas without making use of pipelines. As a result, in the first nine months of 2022, GTT recorded an intake of 134 orders, increasing its backlog to 269 orders, which we estimate to be worth about EUR 1.2 billion in sales.

GTT Investor Relations publications

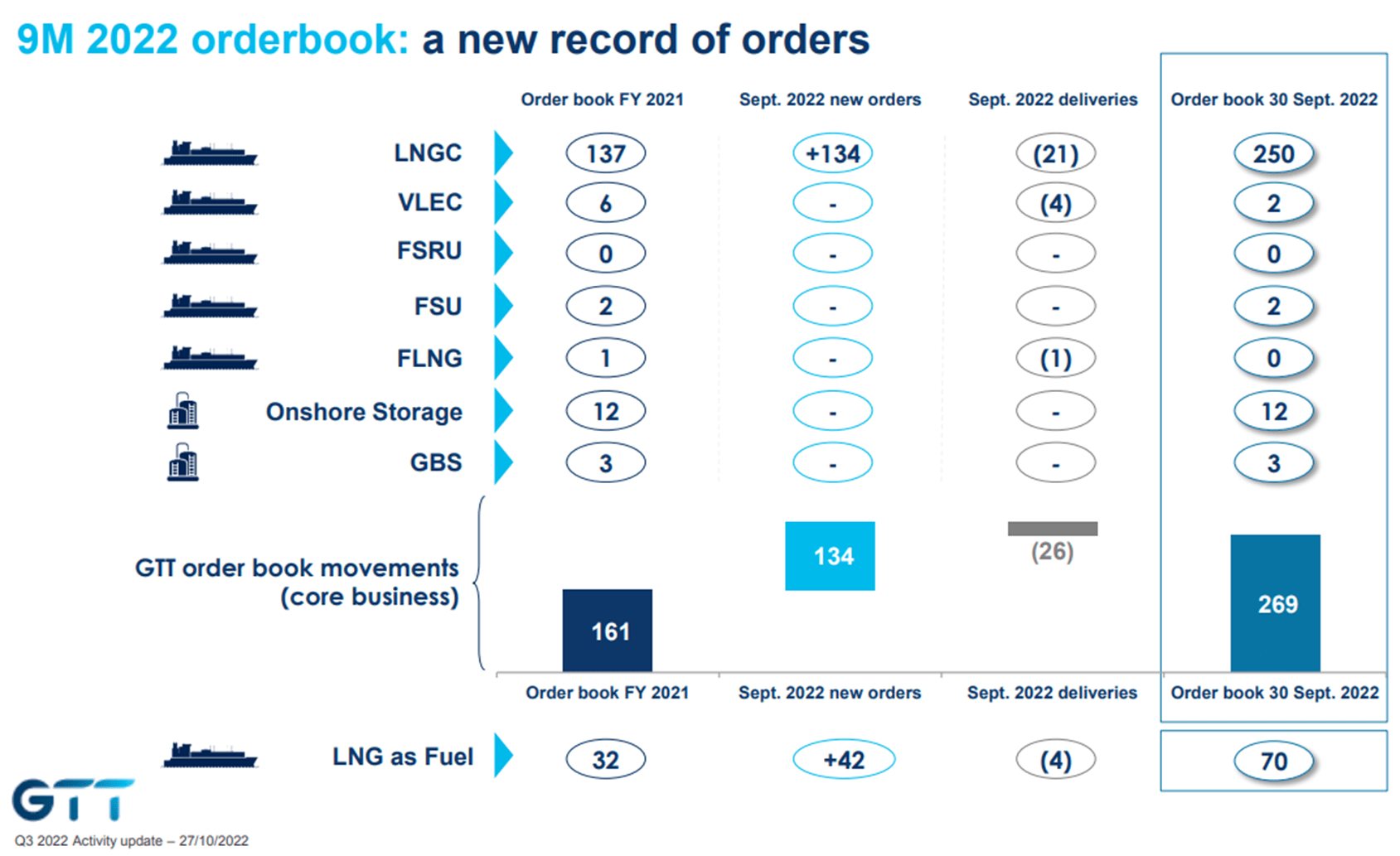

The graph below from GTT’s latest investor presentation for 3Q22 details the evolution and composition of the order backlog as of the end of September 2022. As can be seen, the order book is dominated by LNG carriers (LNGC), although one should also point that growth in orders for LNG propulsion systems for maritime vessels (i.e. LNG as Fuel in the graph below) has exploded, with the order book more than doubling from the start of 2022 to 70 orders total by the end of 3Q22.

IR presentation 3Q22

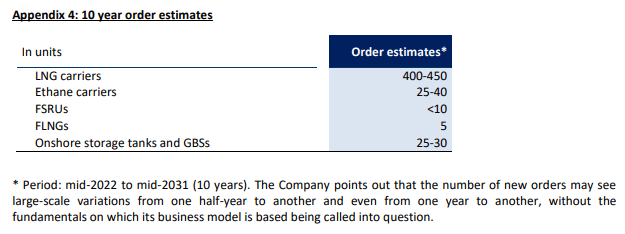

In the July 2022 update that GTT gave on ’10-year order estimates’ for the period starting mid-2022, the company projected to win 465-535 new orders, worth some EUR 2.2 billion in sales according to our estimation.

GTT 1H22 results

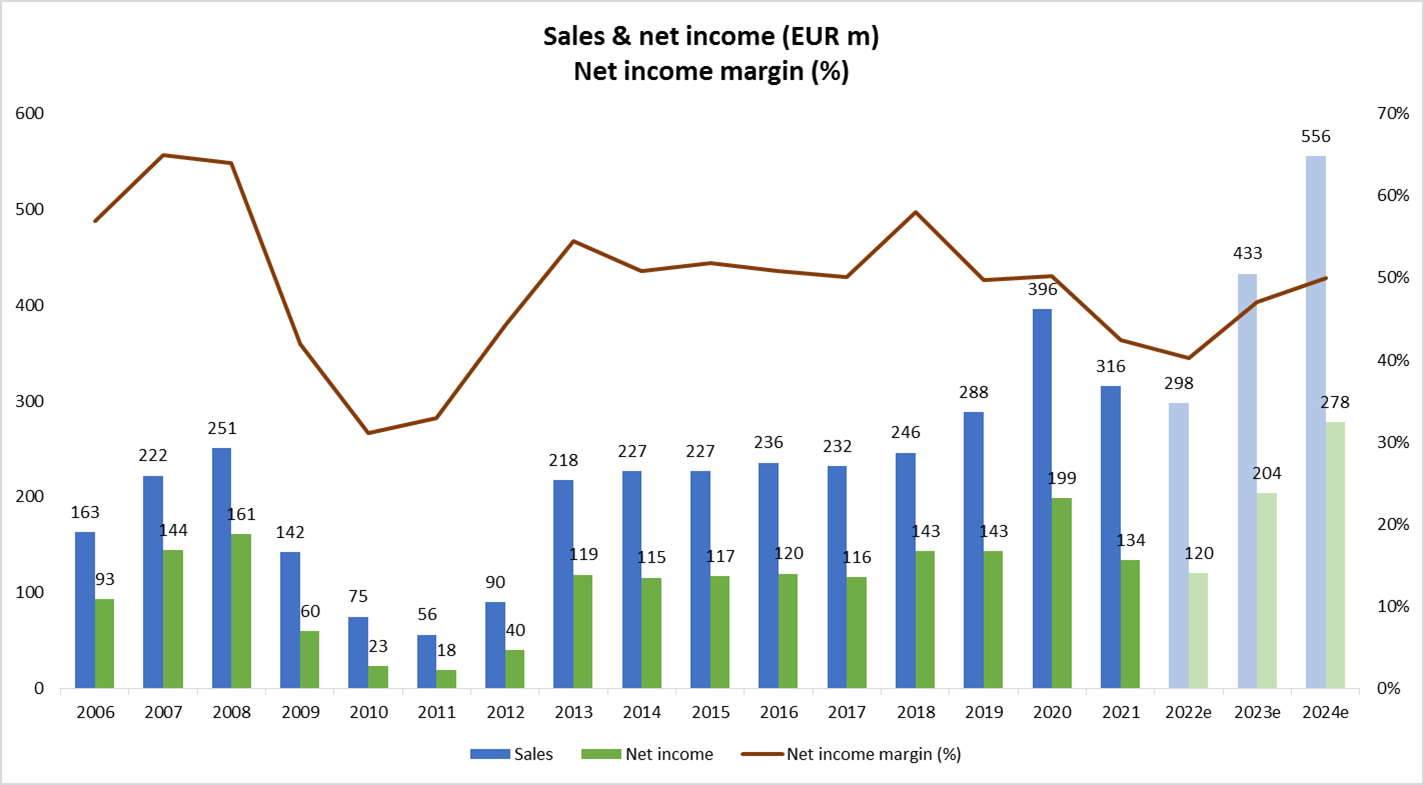

Let’s now turn our attention to the firm’s financial performance, and how it has delivered on its order book to generate sales and profits for shareholders. As should already be obvious, no one should be in denial about the fact that GTT operates in a highly cyclical business. Depending on the state of the order backlog and evolution in order intake, slowdowns can either be very pronounced (such as in the 2008-2011 period), or barely noticeable (2015-2018). Despite being an asset-light business, there is still some operating leverage, mainly related to fixed personnel expenses, which can make profit margins fluctuate meaningfully in-line with sales growth. Looking forward, we can see that the strong order intake of recent times, and the all-time high order backlog, are expected to generate fast growth in sales in 2023 and 2024. Net profit margins are also expected to recover towards 50%, according to consensus estimates.

GTT IR publications, Refinitiv

Other aspects of our initial investment thesis on the company remain largely unchanged, such as the firm’s strong free cash flow generation, stellar balance sheet, and shareholder-friendly dividend policy.

Potential reasons for recent stock price weakness

Finally, let us consider some of the factors that have likely contributed to the recent decline in GTT’s stock price, from a high of nearly EUR 140 per share last summer to below EUR 100 presently. General market unease notwithstanding, a number of company-specific developments have contributed to this weakness:

- On December 1, 2022, the Seoul High Court confirmed GTT’s obligation to separate the technology license agreement from technical assistance, if requested by the Korean shipyards. This is part of an ongoing legal dispute with the Korea Fair Trade Commission that dates back to 2016. GTT has once again appealed the decision.

- On January 2, 2023, GTT communicated with investors regarding the likely impact of European sanction packages N° 8 and 9, notably prohibiting engineering services with Russian companies, and the company’s decision to cease its activities in Russia. According to the press release, GTT estimates a total exposure to Russia represented slightly less than 6% of the order book.

- Finally, it should be noted that Engie SA has continued to divest of its stake in GTT, via a private placement to institutional investors and a convertible bond offering in 2021, and likely some selling on the open market since then. From owning nearly 15 million shares at the start of 2021, Engie now only owns about 3.6 million GTT shares, or slightly less than 10% of the company (convertible bonds excluded). GTT indicates in its 3Q22 presentation that Engie intends to keep a 15% participation in the firm for the time being, including the convertible bonds, which implies that Engie may still be looking to sell half its direct equity holding, or some 1.8 million shares. Over time, this will continue to increase the proportion of GTT’s shares that are freely-floated on the Paris stock exchange.

Concluding thoughts

As Bastiat once said:

… life is only a long apprenticeship. … Man’s starting-point is ignorance and inexperience. The farther we trace back the chain of time, the more destitute we find men of that knowledge which is fitted to direct their choices-of knowledge that can be acquired only in one of two ways; by reflection or by experience.

This applies to investing as much as it does to any other human endeavor. Hopefully, by indulging us with the first part of this article, you’ve learned something from our experience investing in GTT, and the mistakes we made along the way. In the second part, we aimed to highlight the more recent positive development in GTT’s business since our initial article. In our view, the main conclusions we drew back then remain entirely valid, and as a result, we’d be happy to own a participation in the business once again at the right price.

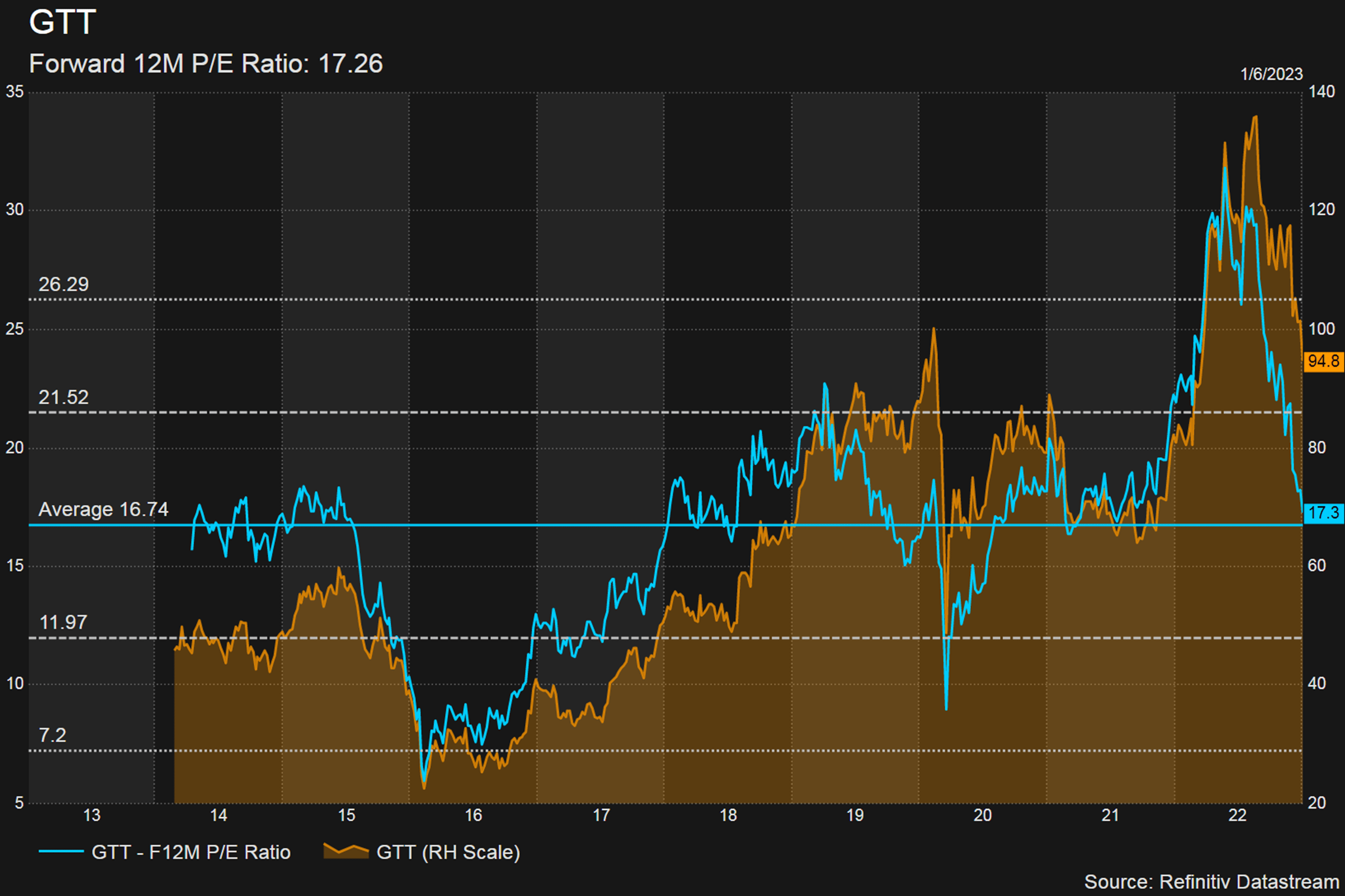

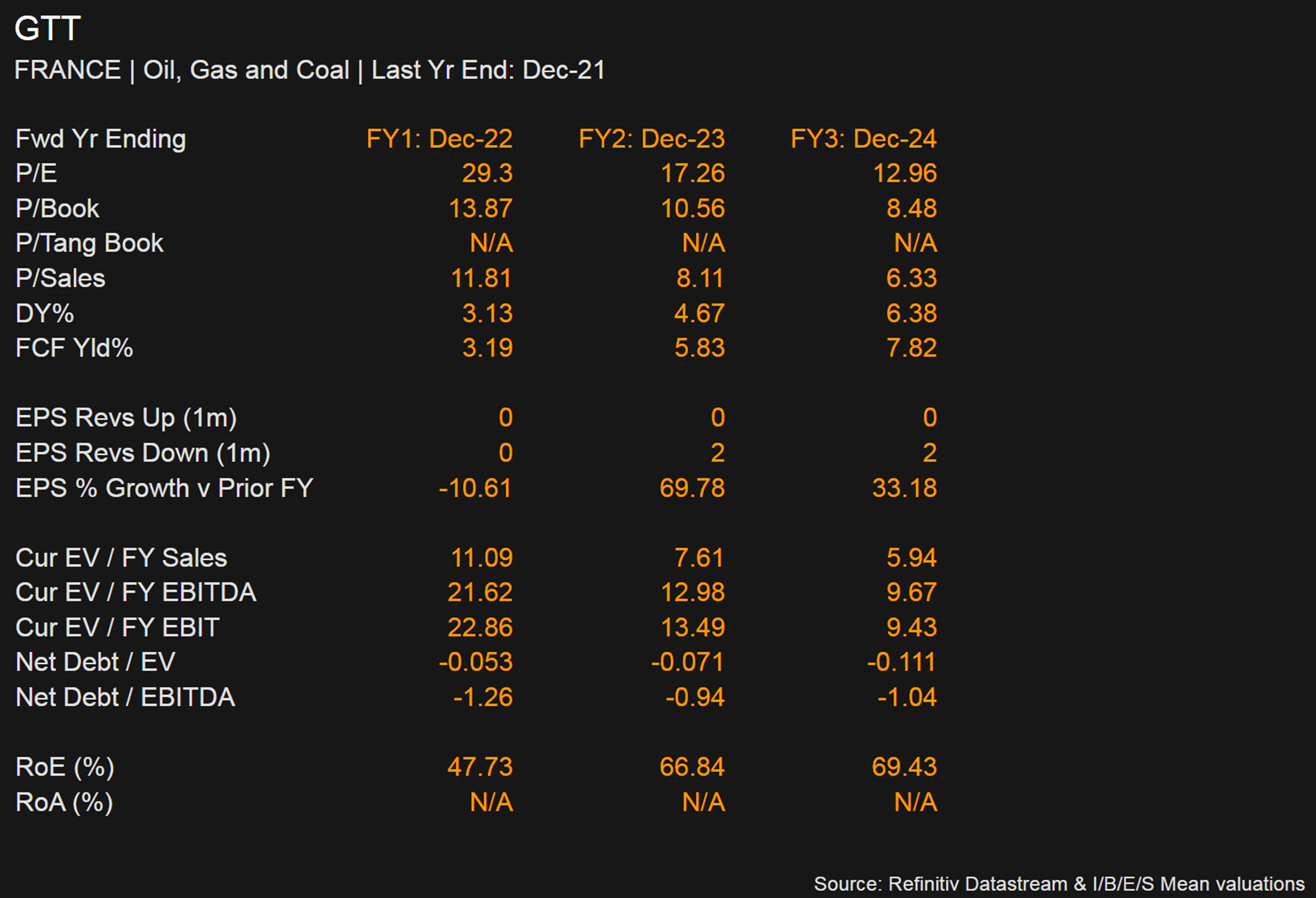

Recent news flow regarding legal disputes as well as Russian sanctions have pressured the stock price of late, and that ‘right price’ might not be too far from the current quotation, depending on one’s required margin of safety. Some might look at a forward PE of 17x 2023 earnings and 13x 2024 earnings, according to consensus estimates, and find the valuation attractive enough (see Appendix). Others, as we do, might prefer to base their valuation assessment on an estimation of mid-cycle earnings power, rather than what might be a cyclical peak in earnings in the next 2-3 years. In such a case, patience is still required to purchase the company at a more reasonable price below EUR 80 per share.

—

Appendix

Goldman Sachs, Kahneman, Montier Refinitiv, as of Jan. 5th 2023 Refinitiv, as of Jan. 5th 2023

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment