FX Week Ahead Overview:

- The first week of a new month brings about the usual smattering of ‘high’ rated event risk from around the globe.

- The global economic recovery from the coronavirus pandemic is in focus, with two central bank meetings and three major labor market reports (including April US NFP).

- Overall, recent changes in retail trader positioning suggest that the US Dollar still has a mixed bias.

For the full week ahead, please visit the DailyFX Economic Calendar.

05/04 TUESDAY | 04:30 GMT | AUD Reserve Bank of Australia Rate Decision

The RBA’s May meeting may come and go without many surprises, given the recent tone that’s been established over the course of many weeks and months. But the fact of the matter is that the RBA still has some QE allocated henceforth, and there may be some language around the timing of bond purchases later this year. Absent that, however, the RBA may offer some light jawboning around the Aussie itself, which it has considered overvalued during the pandemic recovery.

Reserve Bank of Australia Interest Rate Expectations (MAY 3, 2021) (Table 1)

RBA interest rate expectations have remained firmly anchored for several weeks, thanks in large part to the RBA’s efforts to keep Australian government bond yields tamed through yield curve control (YCC). To the extend that the RBA has said it intends on keeping interest rates low through March 2023, there is little to no reason to think that the main rate is going up anytime soon (although alterations to the QE program are possible).

05/04 TUESDAY | 22:45 GMT | NZD Employment Change & Unemployment Rate (1Q)

The New Zealand economy didn’t experience the downside that many of its developed counterparts did throughout 2020, in both economic and human capital lost to the pandemic, but that also means it’s not experiencing the type of high-flying growth figures that are coming from places like China or the United States.

To this end, the New Zealand labor market experienced but only modest growth in 1Q’21, with the employment change due in at +0.2% from +0.6% (q/q), while the unemployment rate is set to stay on hold at 4.9%. Accordingly, with an otherwise bearish seasonal backdrop for the New Zealand Dollar, these labor market data may not help the New Zealand Dollar.

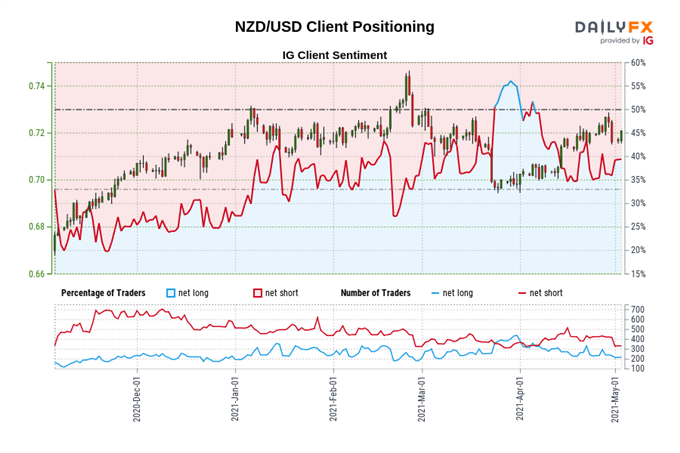

IG Client Sentiment Index: NZD/USD Rate Forecast (May 3, 2021) (Chart 1)

NZD/USD: Retail trader data shows 40.25% of traders are net-long with the ratio of traders short to long at 1.48 to 1. The number of traders net-long is 18.55% higher than yesterday and 1.87% lower from last week, while the number of traders net-short is 16.82% higher than yesterday and 12.19% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests NZD/USD prices may continue to rise.

Yet traders are less net-short than yesterday and compared with last week. Recent changes in sentiment warn that the current NZD/USD price trend may soon reverse lower despite the fact traders remain net-short.

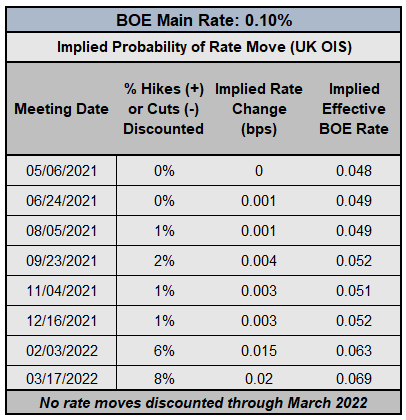

05/06 THURSDAY | 11:00 GMT | GBP Bank of England Interest Rate Decision

The BOE is not moving on interest rates any time soon. However, the BOE has a specified target for its pandemic-era easing programs unlike the Fed or ECB (which have open-ended QE programs), and, as the saying goes, ‘the night is getting long.’

Bank of England Interest Rate Expectations (May 3, 2021) (Table 2)

The BOE set a target of purchasing £875 billion of UK government bonds through the end of 2021, and unless the pace of QE is slowed in the next few months (perhaps now, but if not now then extremely likely by the end of summer), then the BOE will likely achieve its £875 billion target in early-October. A slight change of pace to the purchase program would keep the liquidity spigot open for a few more months, which markets would likely perceive as a positive (but perhaps not for the British Pound).

05/07 FRIDAY | 12:30 GMT | CAD Employment Change & Unemployment Rate (APR)

After a robust +303.1K reading on the headline March Canada jobs report, the Great White North is expected to see a not-so-great iteration of its labor market readings during April. Consensus forecasts are calling for the Canadian economy to have shed -175K jobs, leading to an uptick in the unemployment rate from 7.5% to 7.8%. The Canadian Dollar, which has enjoyed a strong 2021 thus far, may be burdened amid an otherwise bearish seasonal backdrop.

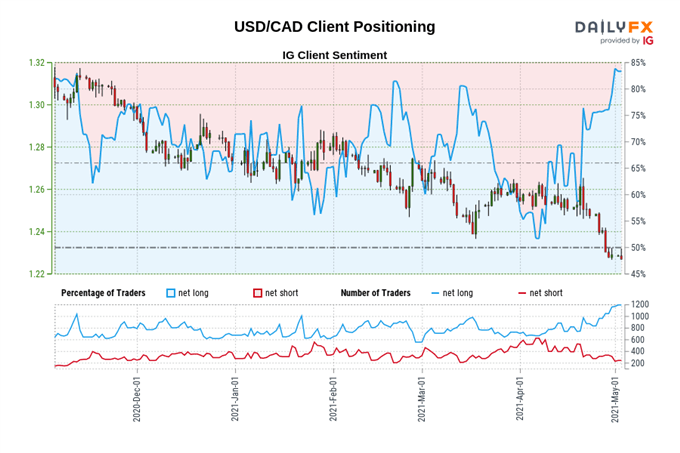

IG Client Sentiment Index: USD/CAD Rate Forecast (May 3, 2021) (Chart 2)

USD/CAD: Retail trader data shows 81.61% of traders are net-long with the ratio of traders long to short at 4.44 to 1. The number of traders net-long is 11.15% higher than yesterday and 40.48% higher from last week, while the number of traders net-short is 20.88% higher than yesterday and 4.88% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/CAD prices may continue to fall.

Positioning is less net-long than yesterday but more net-long from last week. The combination of current sentiment and recent changes gives us a further mixed USD/CAD trading bias.

05/07 FRIDAY | 12:30 GMT | USD Non-Farm Payrolls & Unemployment Rate (APR)

The US economy is humming right now, and forecasts are starting to roll in from banks and other financial institutions that peg the 2021 to 2022 years as perhaps the best two-year period of growth for the US economy since 1950 to 1951 – the peak of the post-World War II boom. If those forecasts come true, then it likely means robust jobs growth across sectors for the US economy.

The upcoming US non-farm payrolls report and household employment survey (from which unemployment rates are derived) should indicate that the US economy is indeed booming as it shifts away from the worst of the pandemic. Consensus forecasts are looking for US jobs growth at +988K in April, up from the equally-torrid pace of +916K in March. The unemployment rate (U3) is due to fall to 5.8% from 6%, its lowest mark since the pandemic started (not withstanding the drop in labor force participation rate, which suggests ample labor remains on the sidelines should higher wages prevail).

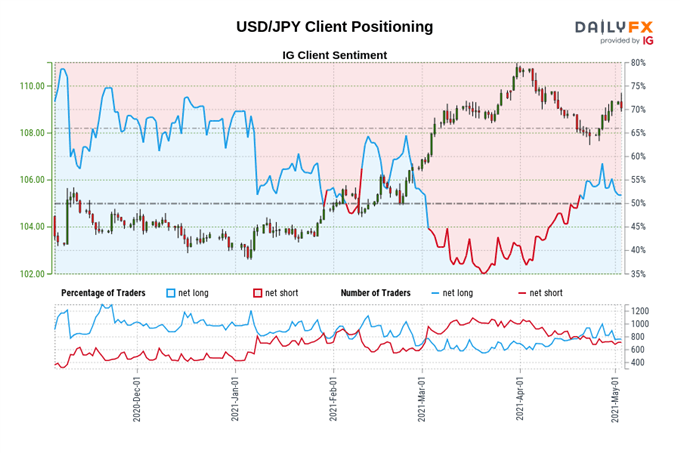

IG Client Sentiment Index: USD/JPY Rate Forecast (May 3, 2021) (Chart 2)

USD/JPY: Retail trader data shows 53.99% of traders are net-long with the ratio of traders long to short at 1.17 to 1. The number of traders net-long is 6.28% higher than yesterday and 8.14% lower from last week, while the number of traders net-short is 3.62% lower than yesterday and 6.61% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/JPY prices may continue to fall.

Positioning is more net-long than yesterday but less net-long from last week. The combination of current sentiment and recent changes gives us a further mixed USD/JPY trading bias.

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

Be the first to comment