FX Week Ahead Overview:

- The final week of July brings forth a packed economic calendar – particularly for the US Dollar: June durable goods orders; July consumer confidence; the July FOMC meeting; and 2Q’21 US GDP.

- Elsewhere, Australia and Canadian inflation rates and Mexican GDP are due over the coming days, likely to inject volatility in AUD-, CAD-, and MXN-crosses.

- Overall, recent changes in retail trader positioning suggest that the US Dollar has a mixed bias.

For the full week ahead, please visit the DailyFX Economic Calendar.

07/28 WEDNESDAY | 01:30 GMT | AUD INFLATION RATE (CPI) (2Q)

Like most of the developed economic world, Australian price pressures have begun to increase. According to a Bloomberg News survey, the headline Australia inflation rate is due in at +3.8% (y/y) for2Q’21, a sharp uptick from the +1.1% rate in 1Q’21.

While headline inflation is shooting through the upper bound of the Reserve Bank of Australia’s +1-3% target range, the central bank’s position has been to look through any near-term acceleration in inflation, continuing to promise to keep its main rate on hold until March 2023. Given how downtrodden the Australian Dollar has been in recent weeks, the elevated inflation reading may help spur short-term speculation that could lift AUD-crosses.

{{GUIDE|AUD}

07/28 WEDNESDAY | 12:30 GMT | CAD Inflation Rate (JUN)

According to a Bloomberg News survey, the June Canada inflation rate (CPI) is forecasted to show a deceleration to +3.2% from +3.6% (y/y), while the core reading is due in unchanged at +2.8% (y/y). The Bank of Canada has already announced another taper to its QE program, thus making it unlikely that the forthcoming inflation will translate into greater speculative fervor for a more hawkish BOC in the very near-term (leaving CAD-crosses on their current trajectory).

07/28 WEDNESDAY | 14:00 GMT | USD Federal Reserve Rate Decision & Press Conference

The July FOMC meeting will conclude on Wednesday, and given the uptick in concerns around the delta variant, the upcoming meeting – typically overlooked as it falls between the June FOMC (which brings a new Statement of Economic Projections (SEP)) and the August gathering in Jackson Hole, Wyoming – may draw heightened interest.

Federal Reserve Interest Rate Expectations (July 26, 2021) (Table 1)

Ahead of the July FOMC meeting, Fed funds futures are pricing in 2% chance of a25-bps rate cut at the forthcoming meeting – immaterial. Notably, however, longer-dated expectations have come down considerably. In fact, one month ago, Fed funds futures were discounting a 63% chance of a 25-bps Fed rate hike in September 2022; those odds have since fallen to 37%. Meanwhile, December 2022 is now the favored month for the first rate move, clocking in with a 68% chance.

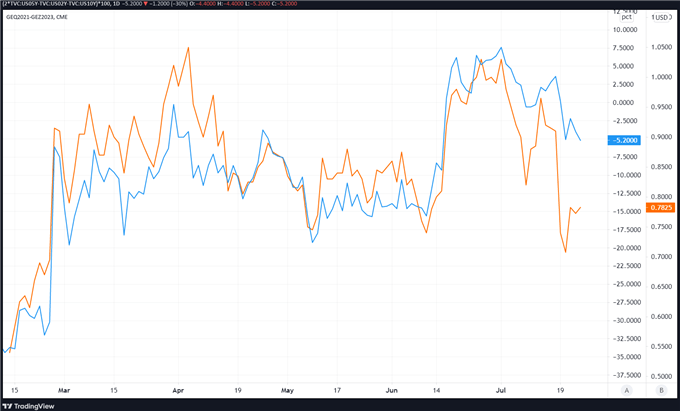

The decline in Fed rate hike expectations can examined from another angle. We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the August 2021 and December 2023 contracts, in order to gauge where interest rates are headed in the interim period between August 2021 and December 2023.

EURODOLLAR FUTURES CONTRACT SPREAD (AUGUST 2021-DECEMBER 2023): DAILY RATE CHART (February 14 to July 23, 2021) (CHART 3)

At their July high following the June US nonfarm payrolls report, there were 103-bps worth of rate hikes discounted by December 2023; now, there are just 78-bps priced-in. Markets are taking a less hawkish view of the FOMC: a full rate hike has been wiped off the board over the course of the month. Consistent with this view, the 2s5s10s butterfly – which tracks non-parallel shifts in the yield curve – has reverted, another indication that bond markets are interpreting a less hawkish Fed.

07/29 THURSDAY | 12:30 GMT | USD Gross Domestic Product (2Q)

According to a Bloomberg News survey, the US economy grew by a searing+8.6% annualized rate in 2Q’21, up from the impressive +6.4% pace reported last quarter. Typically, developed economies like the US produce growth rates between +2-3%; no doubt, ongoing stimulus efforts by the Federal Reserve and the Biden administration are helping juice the figures, as well as the statistical base effect coming out of the pandemic.

But with delta variant concerns on the rise, traders may be paying less attention to backwards-looking reports. Only a significant deviation from the estimate would provoke a sharp repricing in Fed rate odds, particularly on the heels of the July FOMC meeting.

07/30 FRIDAY | 09:00 GMT | EUR Core Inflation Rate Flash (JUL), GDP (2Q)

According to a Bloomberg News survey, the July Eurozone core inflation rate (flash CPI) is forecasted to show a slight moderation from +0.9% in May to +0.8% (y/y), while the initial 2Q’21 Eurozone GDP report is expected to show a booming rate of +13.2% annualized from the -1.3% reading in 1Q’21. With mini-lockdowns emerging in Europe in recent weeks thanks to the rapid spread of the delta variant, there may be concern that the data readings are dated and thus will be ignored by markets.

After all, the European Central Bank’s July policy meeting was notable for President Christine Lagarde’s remarks that policy will be “permanently accommodative,” sapping economic data releases of their potency in the near-term. Like with the US GDP report, only a significant deviation from the estimate would likely provoke a significant move in EUR-crosses.

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

Be the first to comment