Vertigo3d/E+ via Getty Images

fuboTV (NYSE:FUBO) keeps collecting RSN agreements, but the video streaming company needs to grab a gambling angle in order to prosper from these deals. The video streaming market remains a difficult area to generate profits with compressed pricing. My investment thesis remains Neutral on the stock until fuboTV is able to generate revenue synergies from a sports-first streaming platform.

Bally Sports Deal

Last week, fuboTV agreed to carry the 19 Bally Sports regional sports networks (former Fox Sports RSNs) to expand their regional coverage. The deal will allow the company to stream the RSNs for in-market customers under the base plan.

The key here is that only DirecTV (T) carries the RSNs from Sinclair Broadcast Group (SBGI). fuboTV clearly has the cheapest option for picking up the RSNs with the satellite service requiring a nearly $100 subscription in order to view the sports channels.

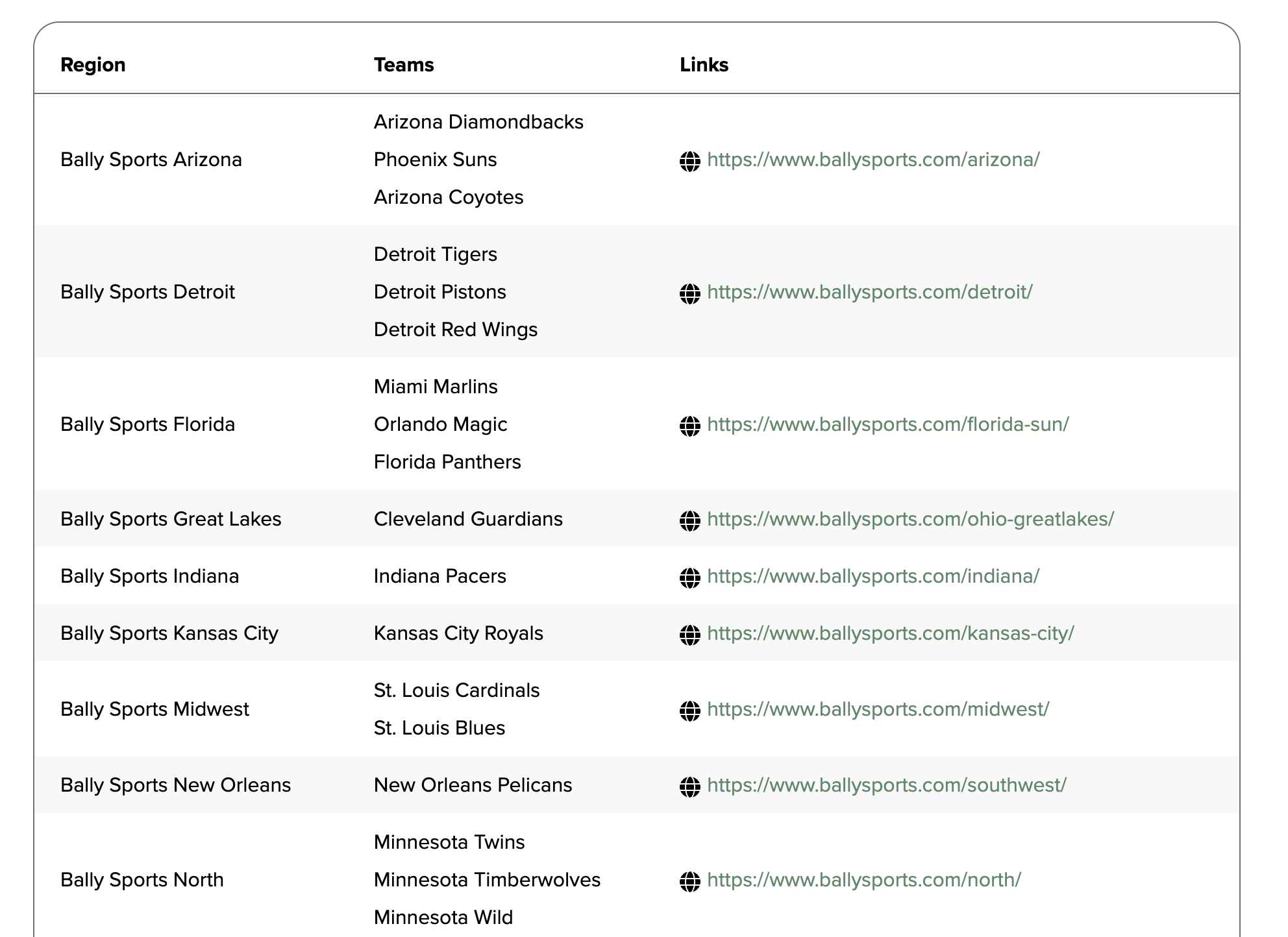

Per the Bally Sports website, the Bally Sports networks are the leading providers of professional local sports. The below table highlights the team coverage in certain networks with a spattering of MLB, NBA and NHL teams in each RSN.

Source: Bally Sports

Access to these networks would be a gamblers dream, but fuboTV doesn’t exactly have a way to monetize the access to these sports networks. As with the NFL Sunday Ticket deal won by Google (GOOG, GOOGL) for $2 billion, the devil is in the financial details.

Sports rights are expensive and fuboTV distributing the Bally RSNs might leave limited margins. The terms of the deal are unknown, but Bally Sports recently launched Bally Sports+ at a cost of $19.99 per month. The DTC product costs $189.99 a year while fuboTV plans to include the in-market RSNs in a package already costing only $69.99.

Doesn’t Solve Problems

While the Bally RSNs further enhance fuboTV as the leader in sports programming, the deal doesn’t necessarily help the profit picture. Financial details weren’t provided, but DISH Network (DISH) and other streaming services like YouTube TV have balked at paying the high RSN fees.

The company is forecast to produce strong revenue growth in the next year. Analysts have Q4 revenues topping company guidance to hit $286 million for 24% growth. The Q4’23 revenues are forecast to jump another 33% to reach $379 million next year.

The question is really how fuboTV will produce a profit with paying the RSN fees without hiking the monthly subscription price for the base package. With limited margins and large losses, the company won’t see any leverage despite the benefit of adding new subscribers due the lack of the other options for hardcore sports fans to watch in-market teams.

fuboTV only has 1.2 million subs at the end of September with a plan to reach 1.37 million at the end of December. The company would generate $11.9 million in additional monthly revenue from adding 170K customers a month at the base rate of only $70. Under this scenario, fuboTV adds about $35 million in base revenues per quarter.

Again, this is a revenue figure, not a profit figure. The RSNs will no doubt drive additional user growth for customers unlikely to leave with so many other streaming distribution services lacking coverage of the Bally RSNs, but these competitive services won’t add the RSNs for a big reason.

fuboTV recently terminated their owned-and-operated Fubo Sportsbook. If the company can integrate gambling data and subscriptions services into the virtual MVPD service focused on live sports, fuboTV could produce a platform rewarding shareholder with premium offerings beyond just distributing RSNs other streaming services don’t want to touch.

Takeaway

The key investor takeaway is that fuboTV is playing a dangerous game. The company had no plans to turn cash flow positive until 2025 and the addition of the expensive RSNs doesn’t appear to improve this process, though the streaming service could add additional subscribers in the process.

Investors should continue watching from the sidelines until fuboTV figures out a business plan to monetize a sports-first platform beyond just distributing expensive sports content.

Be the first to comment