MicroStockHub

Thesis

First Trust High Income Long/Short Fund (FSD) is a closed end fund focused on high yield corporate bonds. What differentiates this CEF from the larger corporate bond CEF cohort is its long/short mandate:

The Fund will take long positions in securities that MacKay Shields LLC (“MacKay” or the “Sub-Advisor”) believes offer the potential for attractive returns and that it considers in the aggregate to have the potential to outperform the Fund’s benchmark, the ICE BofA US High Yield Constrained Index (the “Index”). The Fund will take short positions in securities that the Sub-Advisor believes in the aggregate will underperform the Index. The Fund’s long positions, either directly or through derivatives, may total up to 130% of the Fund’s Managed Assets. The Fund’s short positions, either directly or through derivatives, may total up to 30% of the Fund’s Managed Assets.

A long/short strategy is a very powerful tool, especially in a year like 2022 that has seen substantial drawdowns across all asset classes. The general idea is that some credits are fundamentally strong, while others are weaker. In a down-market, the stronger credits are going to hold up better, while the weaker ones are going to sink. A manager can basically take a market neutral stance (i.e., neutral overall market risk) and just bet that the difference in credit spreads between the two bonds will widen. That is a very powerful tool in a world where most managers can just buy bonds (i.e., be long).

Let us have a look at an example:

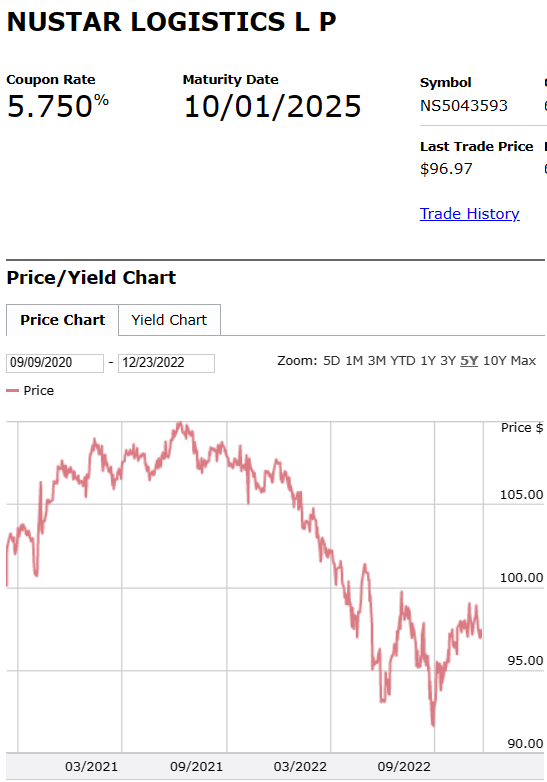

Nustar Bond (Finra)

and

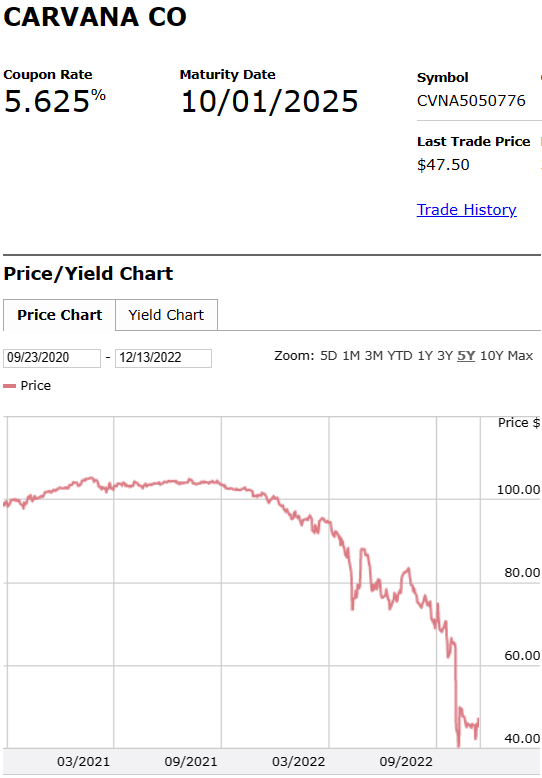

Carvana 2025 Bond (Finra)

We offered two bond graphs above. Both are 2025 maturities. The first one is from an energy company, namely NuStar (NS), while the second one is from a car retailer, namely Carvana (CVNA). We can see the Nustar bond having lost 7 points this year, while Carvana has lost more than 60. A long/short strategy would have gone long the NS bond, while shorting the CVNA one. This paired trade would have produced significant positive results.

Unfortunately for investors, FSD has not done much in terms of shorting weaker bonds. The only position taken by the CEF was to hedge some interest rate risk via a short U.S. Treasuries position. This type of trade just protects the portfolio from some of the increases in interest rates, but does not help with the market-wide credit spread widening, or the opportunities present there. Think about it from an equity perspective – as an investor, many people just take long positions. If you were long the S&P 500 this year you would have been down almost -20% today, however if you are allowed to have a long/short strategy you could have made a substantially higher return – the easiest metaphor is being long the Dow Jones Index and short the S&P 500. This long/short equity play would have made you over 10% in 2022! A long/short strategy can be very powerful.

An investor also needs to keep in mind that a short position does not always have to be outright against a specific bond. A fund manager can undertake such a view by buying protection via swaps on an index, such as the CDX HY Index. Any type of short positioning in 2022 would have generated very positive results. FSD, however, only shorted U.S. Treasuries in order to protect from higher rates. The CEF’s overall performance in 2022 has been in line or worse than other HY CEFs. In our mind, this was a substantial miss in terms of actually taking advantage of the long/short mandate.

FSD Holdings

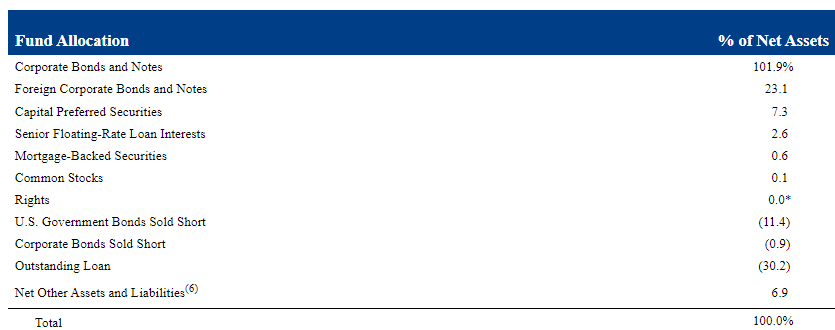

The fund is overweight corporate bonds and notes:

Holdings (Fund Fact Sheet)

We can see the fund having shorted U.S. treasuries in order to hedge interest rates. As rates go up, treasury prices go down, so a short U.S. debt position ensures the portfolio gets some immunization from higher rates (the underlying short position gains value in such an instance).

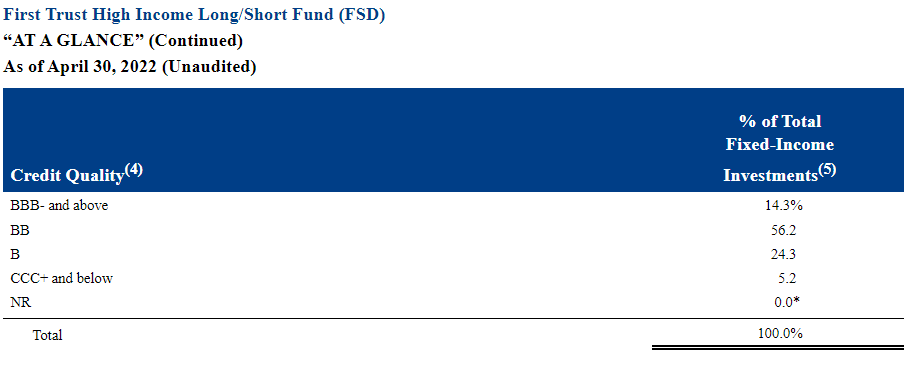

The fund does not take outsized credit risk:

Ratings (Fund Fact Sheet)

We can see from the ratings matrix that most names are in the ‘BB’ bucket, which is a conservative portfolio allocation.

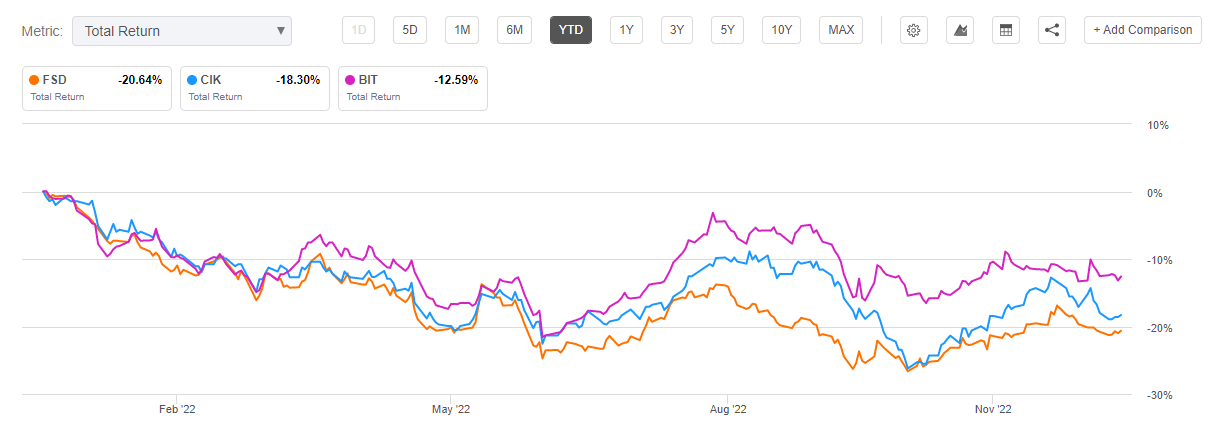

FSD Performance

The fund is now down more than -20% year to date:

Total Return (Seeking Alpha)

The outperformer in the cohort, namely (BIT) is a fund that we have covered here, and it has a better total return than its peers this year due to its aggressive interest rate hedging policy. CIK is a premier HY bond fund, and it has managed a better result than FSD year to date.

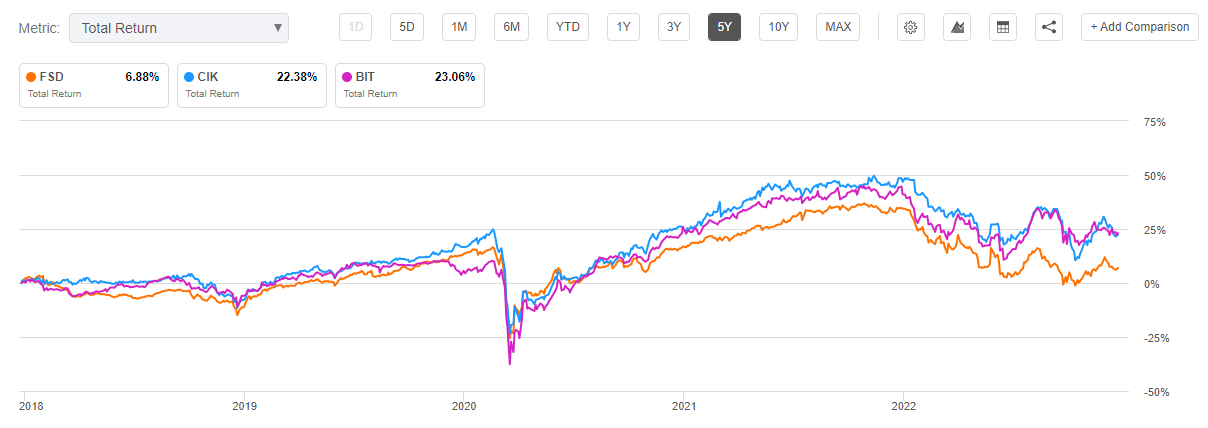

On a 5-year time-frame, the net results are similar:

Total Return (Seeking Alpha)

FSD has managed very poor results over the 5-year time-frame, being at the bottom of the cohort.

Conclusion

FSD is a high yield corporate bond CEF. The fund has a long/short mandate, which was not fully taken advantage of in 2022. The CEF only managed to hedge some interest rate risk via short treasuries positions, foregoing substantial profits that could have been made by shorting weaker credits in the bond market. FSD’s results are commensurate, lagging its peers in the space (peers that are long only focused). Down years like 2022 do not come around very often, and the fact that FSD was not able to take advantage of its short mandate is disappointing. The fund does not seem to actively engage in trying to profit from weaker credits tanking, and to us, it looks more of a long only fund that occasionally hedges interest rate risk. 2022 could have been a great year for the CEF, but it hasn’t.

Be the first to comment