ubrx/iStock via Getty Images

Back in both high school and college, I played the beautiful game of basketball.

I’m a tall guy, so I’ve got that natural advantage. But I’ve also got an absolute love of the sport. Basketball is a passion of mine and therefore one of my few aging-related regrets.

At some point, the sport just becomes too tough to play competitively, and so I’ve largely let go of it outside of shooting hoops with my son. I’ll just have to live vicariously through college and pro basketball, I guess.

I’ve written enough about my love of basketball by now that my regular readers are well aware of that interest of mine. Every time February ends – or even before begins, I’ll admit – I’m planning out my March Madness REIT series.

I’ll include introductions about which teams are in, who has advanced, and the tournament’s history. It’s a ton of fun, so stick around if you want to get in on all the stats – as well as the equally competitive analysis I attach to them.

But today, I’m going to fill you in on a sports-related detail you probably don’t know about me…

I played baseball in middle school. Moreover, I was pretty darn good at it.

So good, in fact, that they named me the “homerun king.”

I would swing for the fences. And while I can’t tell you I always connected… I put both power and practice into each attempt for pretty positive results.

I guess it was a shadow of what was to come with my REIT batting average.

Twitter (@rbradthomas)

Dividend Kings Provide Something to Really Admire

Don’t worry. I’m not here to brag about either my middle school baseball batting average or my REIT returns.

I’m just using those subjects to segue into my real topic – and a very profitable one at that.

In fact, I’m not even going to talk about REITs exclusively today.

(Go ahead and gasp or gape in surprise if you’d like. I understand.)

There’s one of those real estate “rewarders” down there, mind you. But that’s only because it’s a dividend king – a title that takes a whole lot longer to achieve than a stint in middle school, mind you.

We’re talking about a minimum of 50 years before a company can claim that title. Here’s what it entails, according to Time magazine:

A dividend king is a publicly-traded company that has increased its shareholder dividends every year for at least the past 50 years… These companies have a proven track record of rewarding shareholders with regular dividends. Think of these as companies like Coca-Cola and Johnson and Johnson.”

In other words, they’re used to proving themselves in every regard over and over and over again.

Because of that high standard, it likely doesn’t come as a surprise that only an exclusive list of firms make the (cut). In 2021, there were 31 dividend kings… in 2022, there (were) 37.”

Now, there are solid stocks that have paid an increased dividend for even just 15 consecutive years. And they should be lauded and applauded for that accomplishment.

It’s not an easy thing to do, especially as markets and economic data ebbs and flows. But that only means we should really, really admire companies that make it to the five-decade mark.

Whereas you can claim the title as part of your portfolio with just the click of a button.

Be Discerning About Your Dividend Kings

That’s not to say you should add them to your portfolio so fast though.

Just because a company has a stellar track record of providing income-oriented investors with what they want doesn’t mean it’s an automatic stellar buy. In fact, depending on their prices, some of these companies can lose you money.

Here I go again on my value spiel. Many of you have read my opinion on this subject a lot. Maybe even ad nauseum.

But that’s because it’s so important to keep in mind. Kingship is quite the title to tout, but heavy is the crown that wears it.

That comes with the territory. It’s hard work to retain that crown. And, in proper recognition of that hard work, investors tend to keep their shares pricey.

We don’t want pricey. We don’t even want to wear the heavy crown. We just want to be loyal vassals who reap the rewards from paying into the king’s coffers.

At a discount.

That’s why my team and I went through the full list of dividend kings to pick out a few that have fallen out of favor – while still maintaining their kingdoms and sustaining their crowns.

These companies are dominant members of their respective industries. They’ve been there, done that, and seen it all, from booms to busts – and lived to tell the dividend tale.

So when the markets decide to forget about their past and how many times they’ve proven what they can do and how well they can do it…?

We want to be there to analyze these monarchs and pay them our compliments – picking up shares in the process.

Make sure to consider whether each one is right for your personal portfolio, of course. But on our end, we see solid gold.

Federal Realty Investment Trust Is King of the REITs

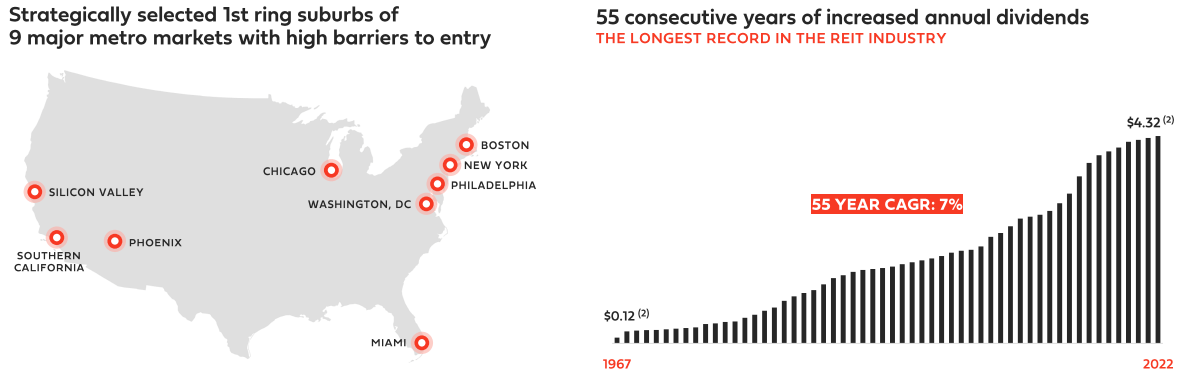

Federal Realty (FRT) is a REIT that invests in mixed-use properties and high-quality open-air shopping centers. They own 104 properties covering 26 million square feet. All told, FRT offers 3,300 residential units and serves 3,200 commercial tenants.

It’s also in nine high-barrier markets with properties in first-ring suburbs that tend to be densely populated and near the city. And Federal Realty has the longest record of dividend increases of any REIT.

Fifty-five consecutive years of annual increases makes it the only REIT to qualify as a dividend king.

FRT – Investor Presentation

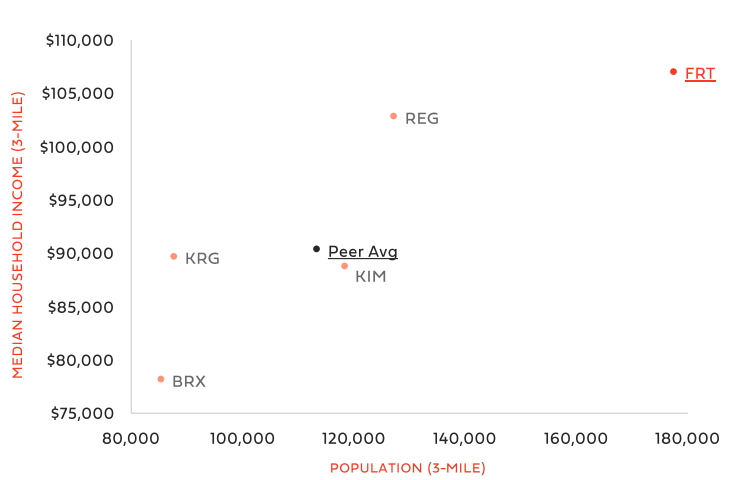

With the location and demographics surrounding its properties, FRT should be relatively well insulated from any pending recession or heightened interest rate environment. These assets are in the middle of or surrounded by large affluent population within three miles of their properties.

That matters. Because if the current inflationary environment continues or a recession ensues… affluent shoppers will be less likely to change their spending habits.

FRT – Investor Presentation

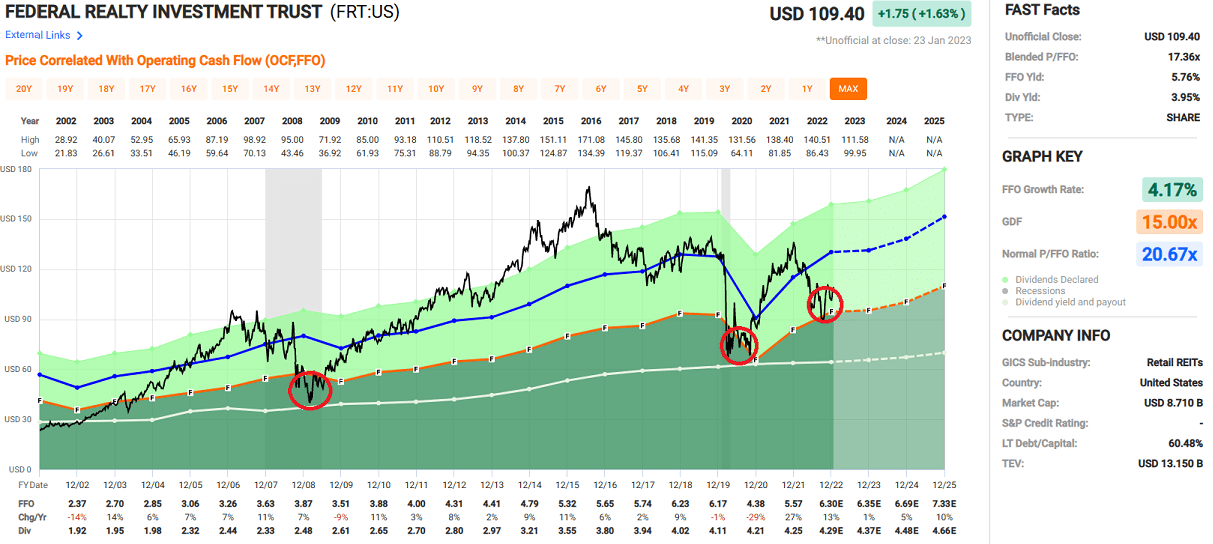

Federal Realty currently pays a dividend yield of 3.95%. That’s sufficiently covered with an expected 2022 adjusted funds from operations (AFFO) payout ratio of 92.06%. While that payout is a little high, this dividend king has averaged roughly 75%-85% since 2007.

During 2020, that ratio did exceed 100%. But it improved to 97.48% in 2021 and then improved again to 92.06% in 2022, where it currently stands.

Don’t get me wrong. I would like to see that figure under 90%. But I still feel confident that Federal Realty will continue to improve this metric given the quality of its assets and management team.

Federal Realty Is Batting a Strong Balance Sheet

Federal Realty is in a strong financial position with a BBB+ credit rating and a 4x fixed-charge coverage. It currently has a net debt to earnings before interest, taxes, depreciation, and amortization (EBITDA) of 6x. But it’s targeting levels ranging between the low- and mid-5x marks.

As of October 2022, FRT had complete availability on its $1.25 billion credit facility. That gives it a total of $1.4 billion in liquidity. Additionally, 87% of its debt is fixed rate, which should provide some stability if rates continue to rise.

The REIT is trading at a blended price to funds from operations (p/FFO) ratio of 17.36x, whereas its average since 2002 has been a multiple of 20.67x. In relation to its earnings, FRT hasn’t been priced this favorably since the pandemic.

At iREIT, we rate Federal Realty a Buy.

FAST Graphs

Lowe’s Companies Knows How to Build With the Best of Them

Lowe’s (LOW) is a home improvement retailer with over 1,700 stores in the U.S. These locations average 112,000 square feet of retailing space for a total of 194 million square feet of national selling space.

It also has 450 stores in Canada consisting of corporate and independent dealer stores operating under the Lowe’s, RONA, Reno-Depot, and Dick’s Lumber brands. These total 14 million square feet of selling space.

In all, it services approximately 19 million customer transactions weekly and employs close to 300,000 associates.

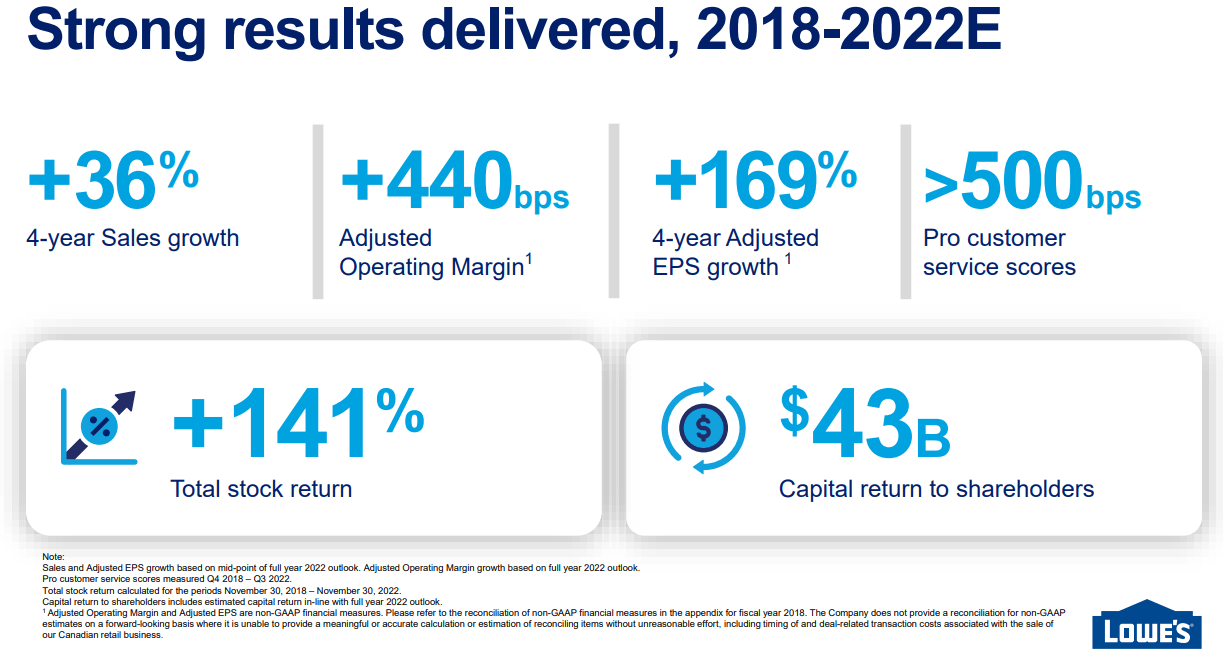

Lowe’s has delivered strong results recently with more than:

- 36% sales growth over the last four years

- 169% adjusted EPS growth since 2018.

In that time, it’s returned $43 billion of capital to shareholders and had a total stock return of more than 141%.

Lowes – Investor Presentation

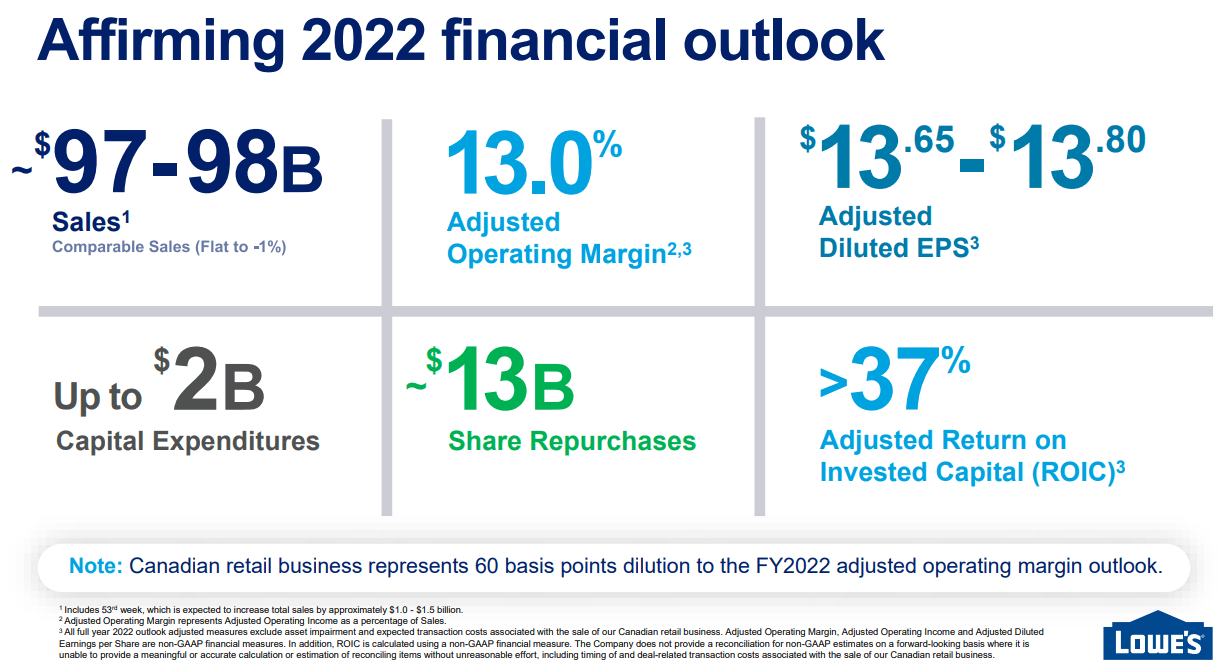

The retailer recently affirmed its outlook for 2022, with:

- $97 billion to $98 billion in sales

- Adjusted diluted earnings per share of $13.65-$13.80

- An adjusted operating margin of 13%

- A Return on invested capital of 37%.

Additionally, Lowe’s affirmed its $13 billion share repurchases for 2022.

Lowes – Investor Presentation

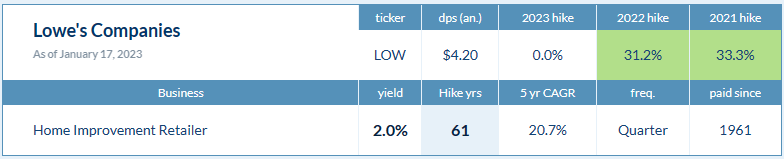

Lowe’s also is a dividend king, having paid a quarterly dividend since 1961 with 61 consecutive annual increases. Over the last five years, it’s raised its dividend at a compound annual growth rate of 20.7%. And it currently has a very safe dividend yield of 2.05% with an estimated EPS payout ratio of 30.46%.

Dividend Hike

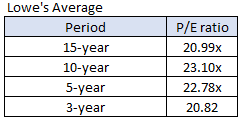

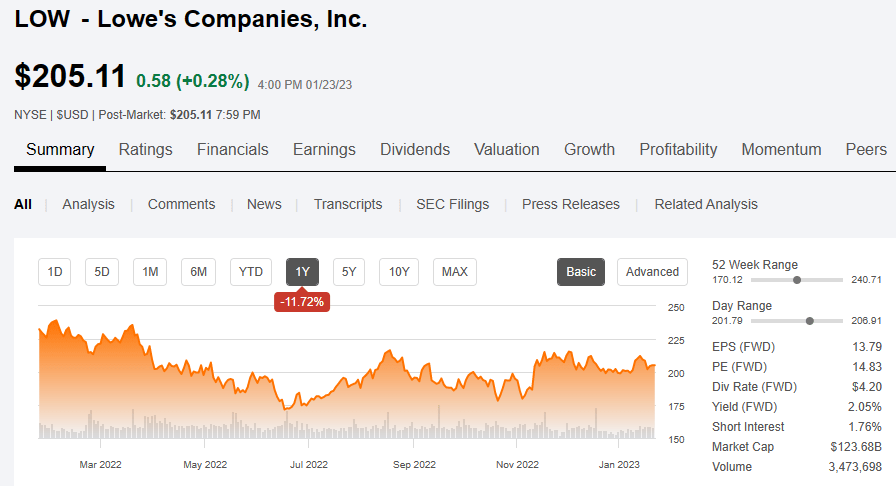

In terms of valuation, Lowe’s is trading at a significant discount when compared to its historical multiples. Its average multiple over the last 15 years has ranged from approximately 20x to 23x. Yet it’s now at a price-to-earnings (P/E) of 14.83x next year’s earnings.

All put together, we rate Lowe’s a Strong Buy.

FAST Graphs – data compiled by iREIT Seeking Alpha

Dover Corporation Drives Dividends Wherever It Goes

Our third dividend king today is Dover (DOV), an industrial conglomerate that operates in five main categories:

- Engineered systems

- Clean energy solutions

- Imaging and identification

- Pumps and process solutions

- Climate technologies.

It has a vast array of products and services, including for industrial automation, waste handling, support services for marking and coding, components for the safe handling of chemicals, and aerospace and defense products.

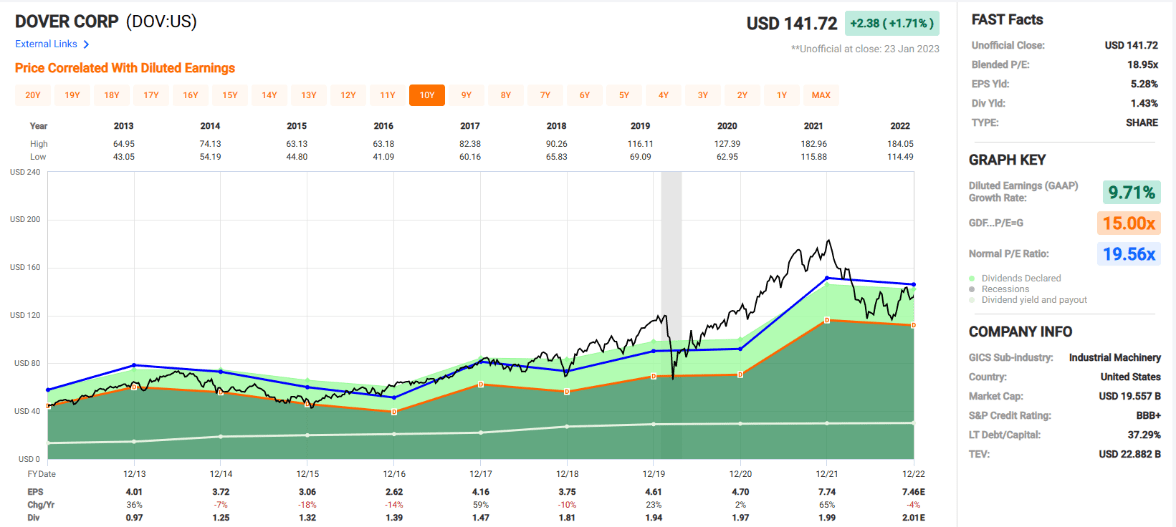

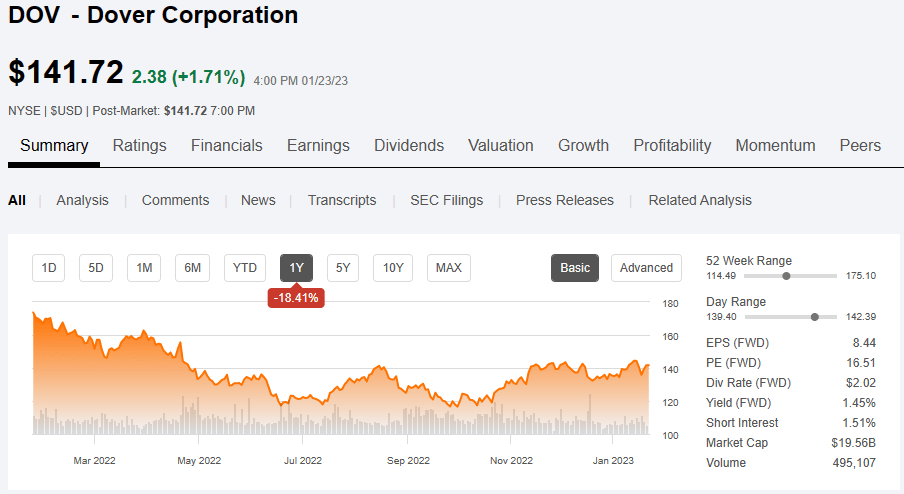

Over the last 10 years, DOV has averaged a diluted earnings annual growth rate of 9.71%. And it’s expected to grow earnings at 5% and 12% in the years 2023 and 2004, respectively.

FAST Graphs

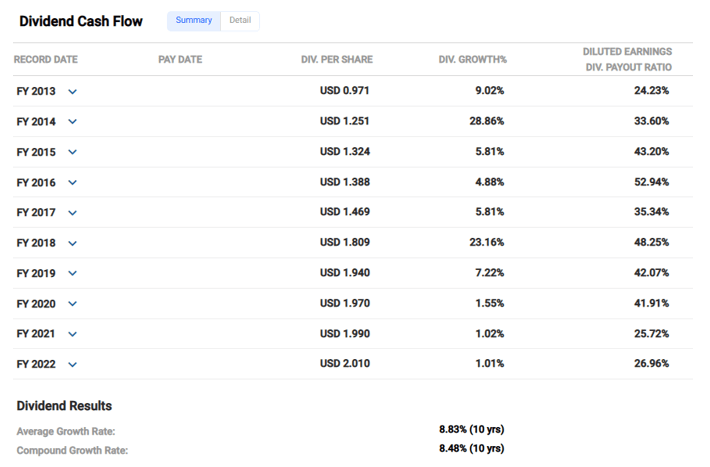

Dover currently has a 1.43% dividend yield and has raised its dividend for the last 66 years. Over the last 10, it’s increased that payout at an average growth rate of 8.83%. And it had a low earnings payout ratio of 26.96% in 2022.

FAST Graphs

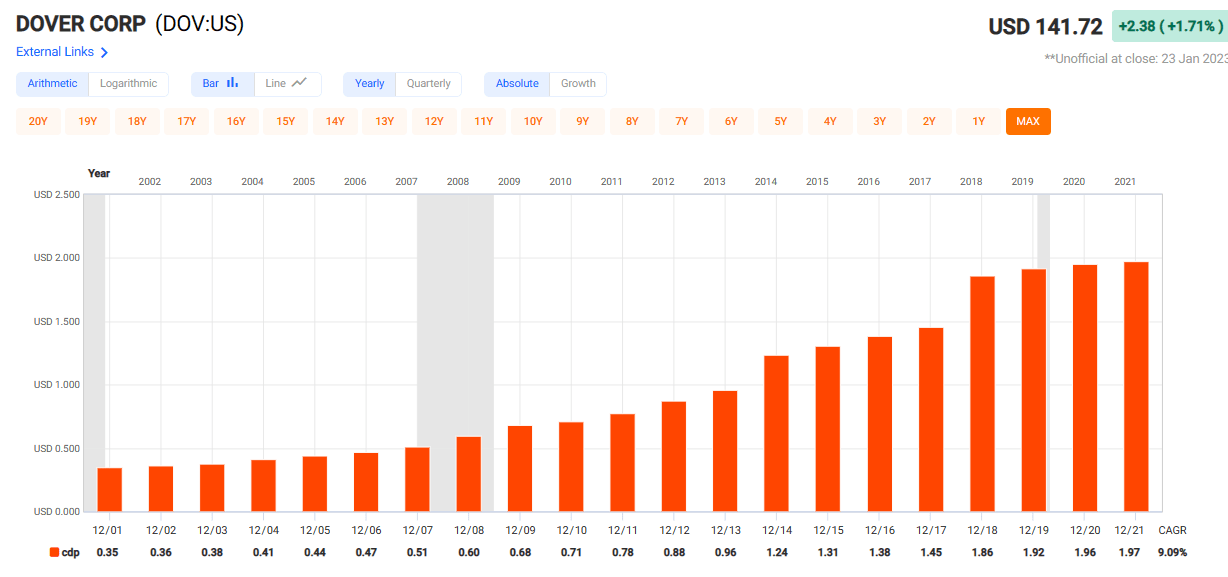

Essentially, Dover’s dividend has been safe and reliable for longer than most of us have been investing. It’s increased its dividend through multiple recessions and bear markets, wars, inflation rates up to 15%, interest rates up to 20%, the 2007-2009 financial crisis and, most recently, the pandemic.

FAST Graphs

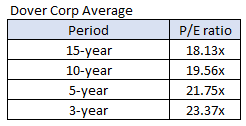

Over the past 15 years, it’s averaged a P/E of 18.13x and has seen multiple expansions for each of the periods listed below.

FAST Graphs – data compiled by iREIT

Currently, DOV is trading at a P/E of 16.51x next year’s earnings, which is well below its historical average – especially over the last five years. We rate it a Strong Buy.

Seeking Alpha

Step Up to the Plate

You should know me by now…

I don’t pitch curve balls. I only provide you with high-quality picks so that you can sleep well at night.

I wish I could promise you that all of my picks would end up being home runs…

But that’s virtually impossible.

However, my track record speaks volumes, and with over a decade of Seeking Alpha articles under my belt, my scorecard is pretty darn good.

I’m confident that my conservative mindset has led to a record 106,000 followers.

I know what it’s like when you swing for the fences and strike out.

I may have been the “home run king” when I was in middle school, but these days I’m perfectly content with doubles and triples.

“Whether I was in a slump or feeling badly or having trouble off the field, the only thing to do was keep swinging.” Hank Aaron

Brad Thomas

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Be the first to comment