Luis M

First Financial Bankshares (NASDAQ:FFIN) is a small ($4.9 billion market cap) but growing Texas bank based in Abilene but with a strong presence in the Dallas/Fort Worth and Houston markets. The bank has a long-tenured management team, with three of its top executives having spent at least 30 years at the bank and its CEO having been there 46 years.

FFIN is an efficiently operated bank with a strong loan book and 36 consecutive years of earnings growth.

The problem? Somewhat inexplicably to me, even after a ~30% stock price decline over the past year, FFIN continues to trade at a high premium to close peers.

Is FFIN a growth stock? Certainly it was up to 2021, registering double-digit EPS growth in the latter years of the 2010s and into the early 2020s. But analysts expect flat earnings in 2023 and only 5.5% growth in 2024. So growth has significantly cooled down, at the very least.

Is FFIN a value stock? No, not since it still trades at a premium to similarly well-run Texas bank peers.

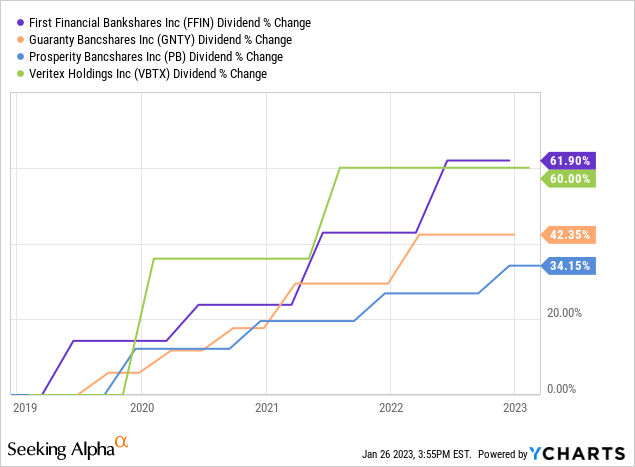

Is FFIN a dividend stock? Well, its dividend growth has been very strong, turning in 11% average annual dividend growth over the last five years, and with a payout ratio of around 40% the bank has room for further hikes. But its low starting yield of 2% won’t appeal to most dividend investors.

Unless and until FFIN can revive its growth rate, the stock will likely be rangebound as investors try to figure out what to expect from this premium-priced Texas bank in the future.

Overview of First Financial

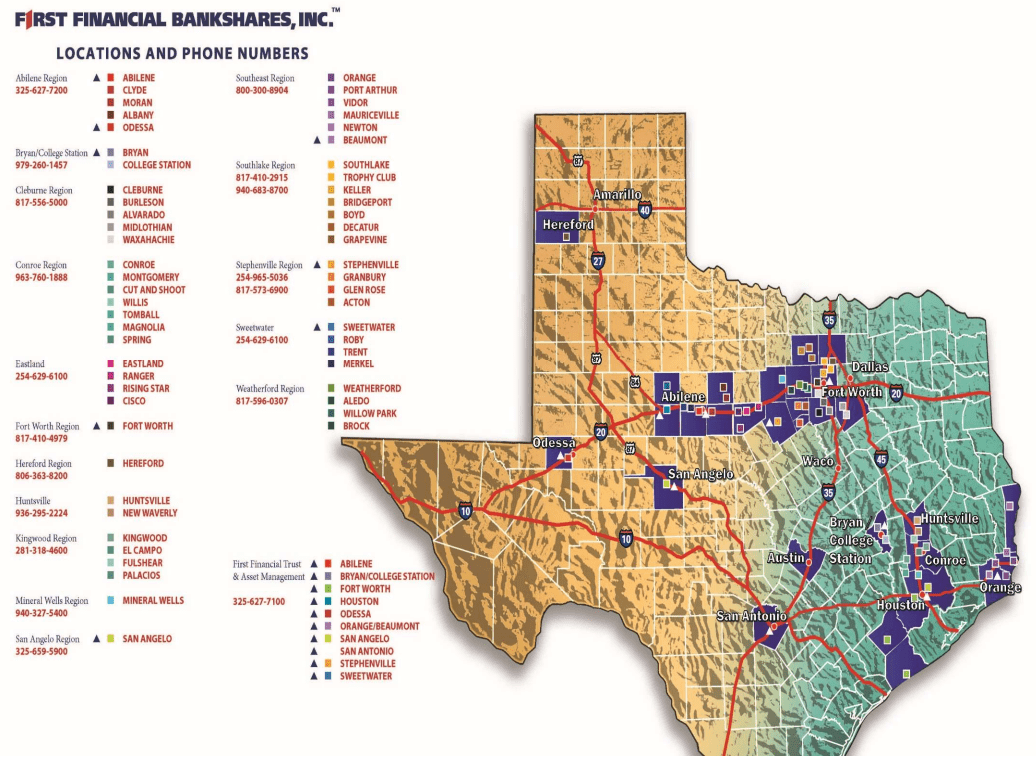

Based out of Abilene, Texas, FFIN has a strong presence along the I-20 highway from Abilene to Dallas/Fort Worth but also has branches as far North as Hereford and as far South as Victoria.

FFIN Q3 2022 Presentation FFIN Q3 2022 Presentation

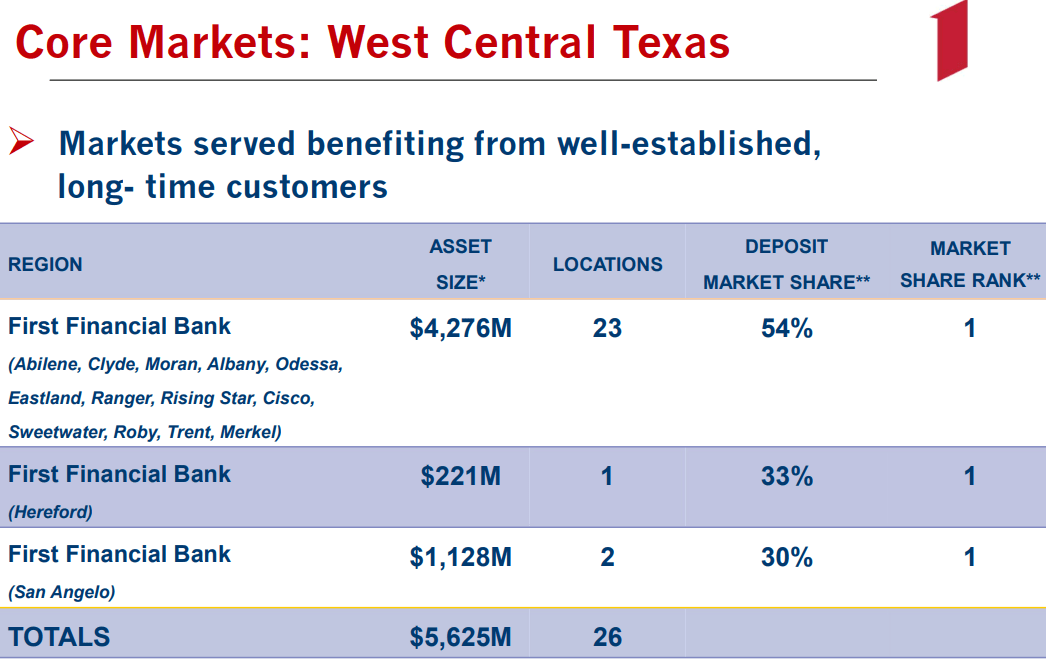

FFIN enjoys dominant a dominant market position in what it calls “West Central Texas,” or the region West of the I-35 stretching as far as Odessa.

But this part of Texas is not growing nearly as fast as the urban metro areas around Dallas/Fort Worth, Houston, and Austin. As such, FFIN has made a concerted effort to expand its operations into these areas in recent years. How successful they will be in capturing market share in these highly competitive markets is difficult to assess.

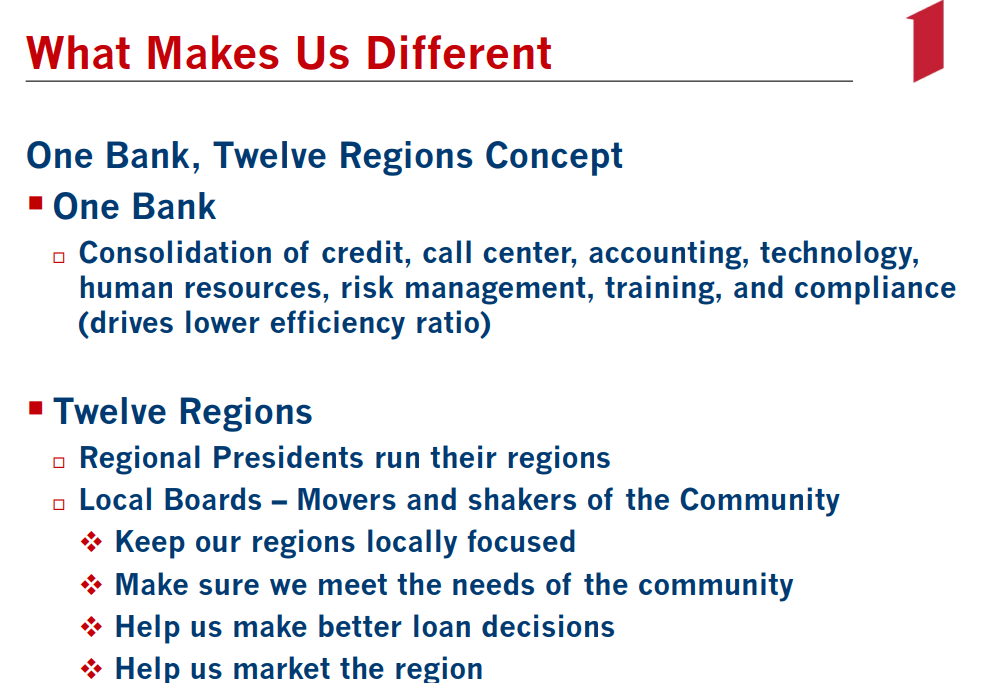

Something interesting about FFIN is the bank’s decentralized structure. The bank operates in 12 defined regions, and each region has its own regional president and local board.

FFIN Q3 2022 Presentation

This, presumably, allows each First Financial-branded bank to have a local feel and perhaps also allows the right type of loans to be approved – and to be approved faster. For the average borrower of a regional bank loan, the interest rate is not the only consideration, but also the ease of doing business and the feeling that one’s banker is a known figure in the community.

I am guessing that this aspect of FFIN helps the bank thrive in smaller markets but may not translate as well to larger, more transient markets like Dallas and Austin.

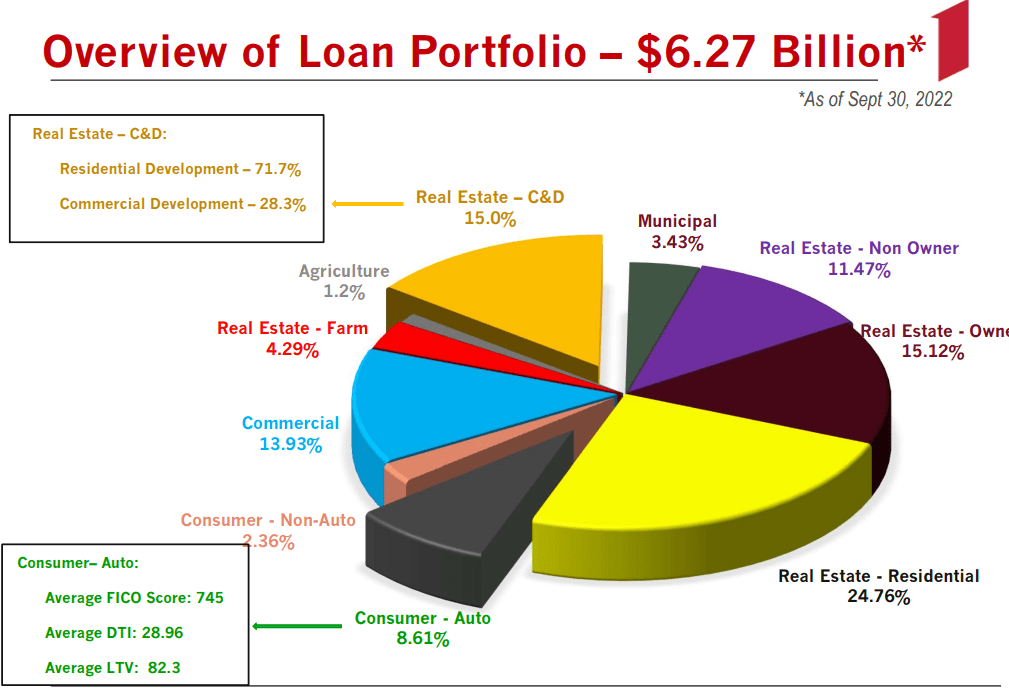

When it comes to the loan book, I find it one of the more diversified portfolios that I’ve seen among regional banks, although most loans are understandably tied to real estate in some form of fashion. Real estate offers a very obvious, tangible form of collateral.

FFIN Q3 2022 Presentation

FFIN is quick to point out that, though 15% of loans are for construction projects, most of that is for residential development. Meanwhile, though 8.6% of loans are consumer auto loans, the bank exercises high underwriting standards and extends loans only to creditworthy borrowers.

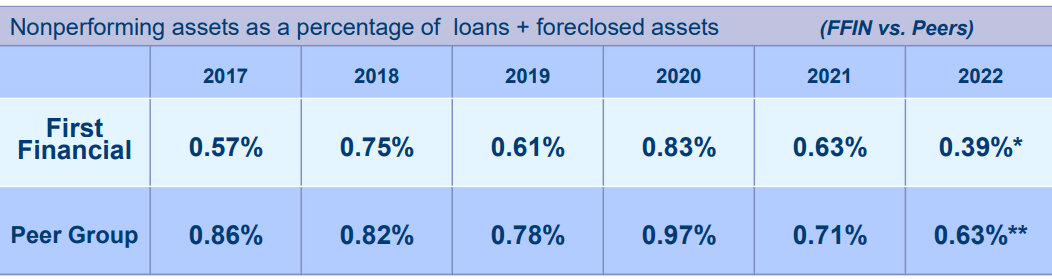

With many irons in the lending fire, one might expect FFIN’s nonperforming assets to be higher than peers, but that is not the case. In fact, FFIN’s NPA as a share of total loans is significantly lower than peers’.

FFIN Q3 2022 Presentation

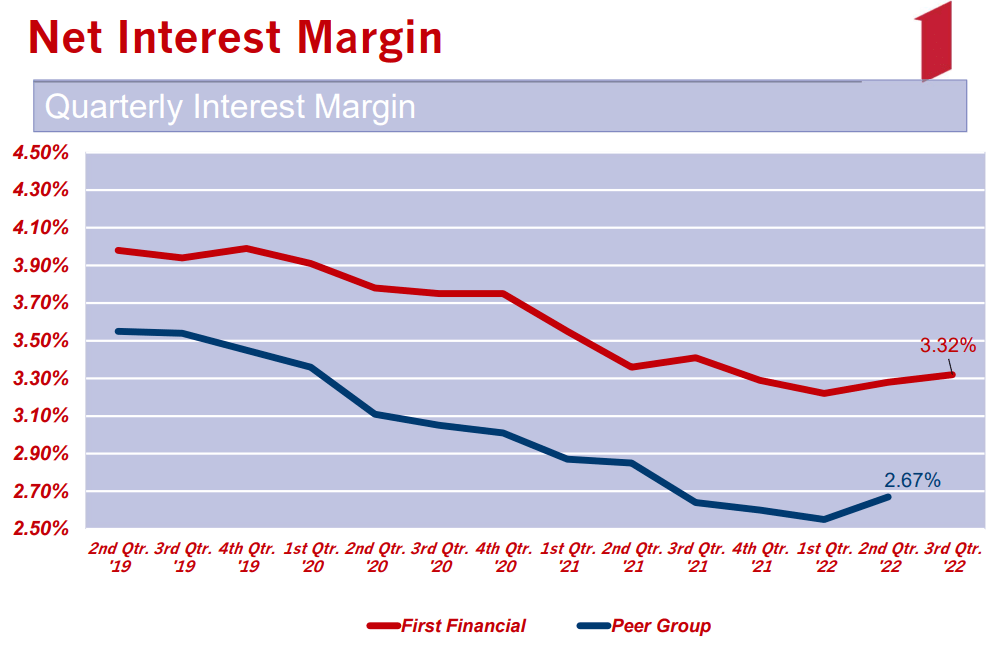

Despite a solid track record, at least in recent years, of maintaining lower NPA to total loans, FFIN also enjoys a substantially higher net interest margin than peers.

FFIN Q3 2022 Presentation

In the fourth quarter, the NIM ticked up further to 3.36%. This is not quite as much of an improvement as I would have expected in the midst of sharply rising interest rates. The factors seeming to suppress further upside in the NIM are a sharp rise in interest expenses and the roll off of PPP loans extended a 2-3 years ago.

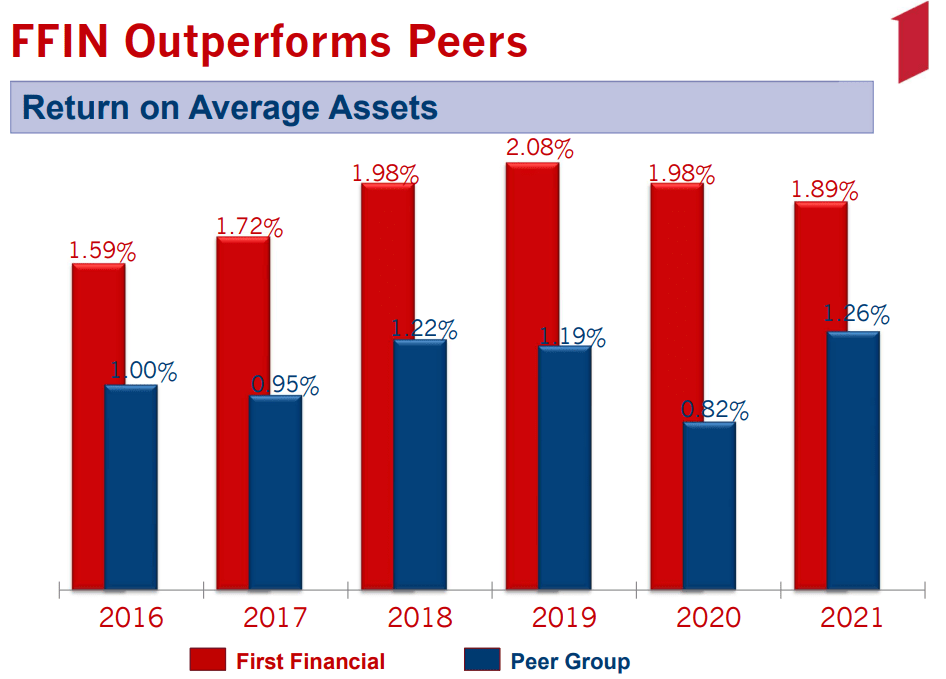

FFIN’s return on average assets has also trended down since peaking in 2019 for reasons unknown to me.

FFIN Q3 2022 Presentation

Return on average assets ended Q4 at 1.76% and also averaged 1.76% for the full year, a drop from 2021’s 1.89% but still above the average of peers.

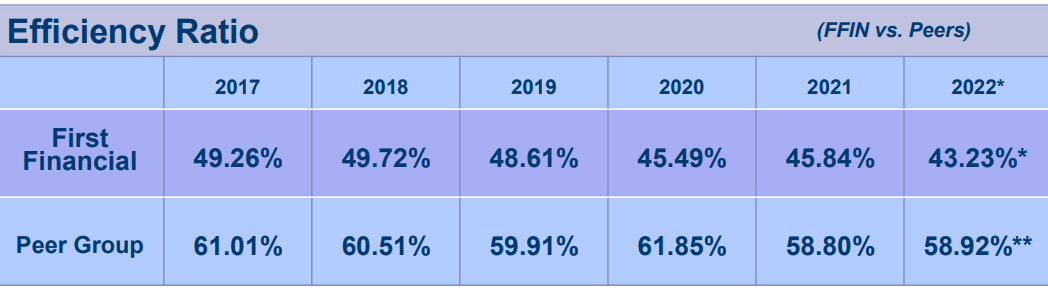

Turning to the bank’s efficiency ratio (lower is better, because it indicates less non-interest expenses required to generate a dollar of income), we find FFIN to be an extraordinarily efficiently run bank with an efficiency ratio almost down to 43%, compared to peers’ ~59%.

FFIN Q3 2022 Presentation

For the full year of 2022, FFIN’s efficiency ratio came in at 43.3%, a nice drop from 2021’s 45.8%. Clearly, as the bank scales up, it has been able to keep expenses under control.

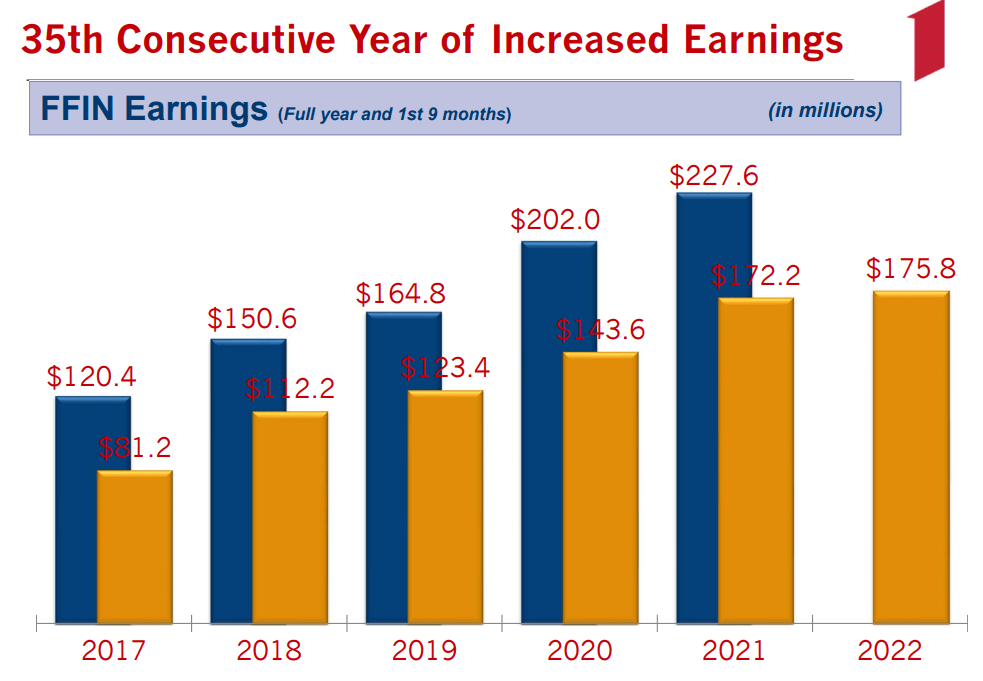

Finally, it’s important to note that one of the bank’s primary strengths is consistency. As of the creation of the chart below, FFIN boasted 35 consecutive years of earnings growth, but 2022 saw that streak extend to 36 years.

FFIN Q3 2022 Presentation

For the full year of 2022, total earnings came to $234.5 million, a 3% bump from 2021’s $227.6 million.

In its recently reported Q4 2022 and full year 2022 results, FFIN reported another quarter and year of earnings growth with EPS of $0.41 in Q4 and $1.64 for the year. That annual EPS number is a mere 3.1% growth over 2021’s $1.59, but it was enough to extend FFIN’s earnings growth streak to 36 years straight.

This demonstrates a remarkable consistency and defensiveness to FFIN’s operations over the decades. Perhaps this has something to do with the particular markets FFIN has traditionally served. The smaller West Central Texas towns that make up FFIN’s bread and butter are more economically linear and stable than larger cities, which tend to be more cyclical in nature.

Comparison To Texas Bank Peers

So, FFIN has some visible and undeniable strengths.

But as Warren Buffett has said, “Price is what you pay; value is what you get.” Is FFIN worth the price investors must pay for it?

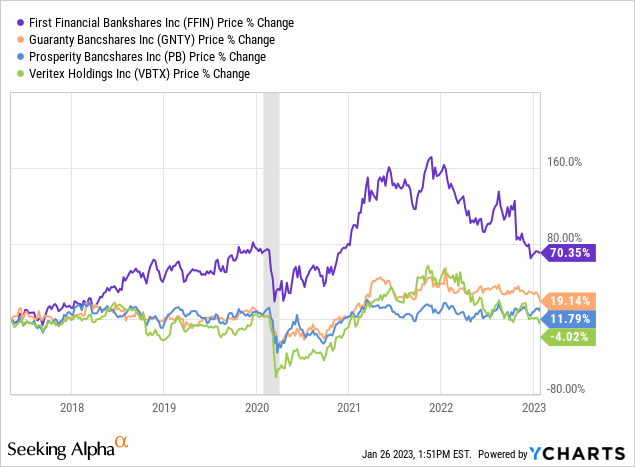

Over the last five and a half years, FFIN has vastly outperformed its close peers:

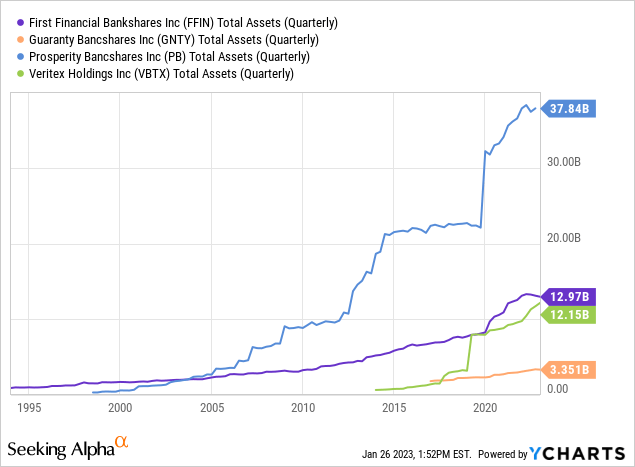

However, while FFIN’s total assets have grown nicely over the last several years, they have not seen quite the same amount of growth as some peers, namely PB and VBTX.

As of Q3 2022, FFIN had total assets of $13.1 billion, total deposits of $11.1 billion, and total loans of $6.3 billion. That indicates a very conservative loan-to-deposit ratio of 0.56x, or 56%.

Here’s how FFIN compares to close peers based on a few key metrics:

| FFIN | GNTY | PB | VBTX | |

| Loan-to-Deposit | 56% | 89% | 66% | 104% |

| Efficiency | 43% | 62% | 41% | 48% |

| Net Interest Margin | 3.36% | 3.57% | 3.05% | 3.87% |

| Return On Average Assets | 1.76% | 0.95% | 1.47% | 1.35% |

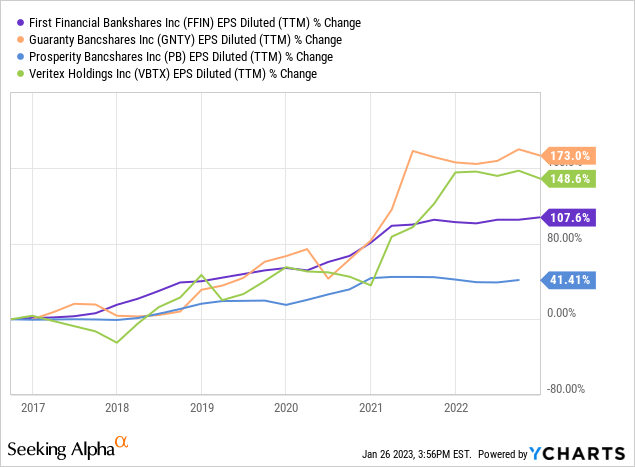

And though FFIN boasts a very long streak of consecutive annual earnings growth, its EPS growth in the last few years has not been quite as impressive as that of GNTY and VBTX.

However, despite a lower dividend yield than peers, FFIN has delivered faster dividend growth over the last four years than its peers.

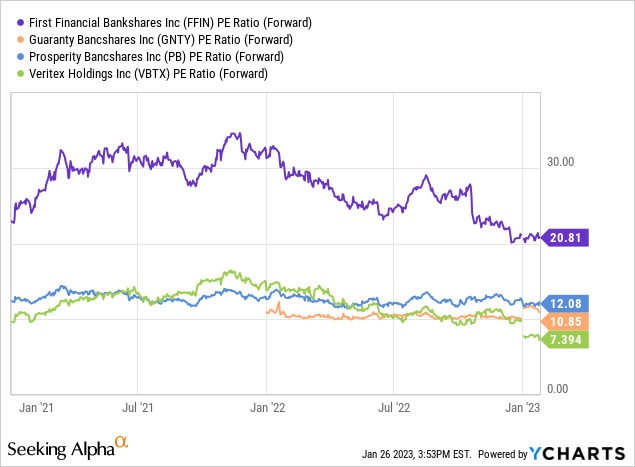

And yet, despite FFIN’s many strengths, I continue to scratch my head at the bank stock’s valuation compared to peers. FFIN’s price-to-earnings ratio is roughly double that of its Texan bank peers.

FFIN’s current stock price of $20.39 (as of this writing) represents a P/E ratio just shy of 21x.

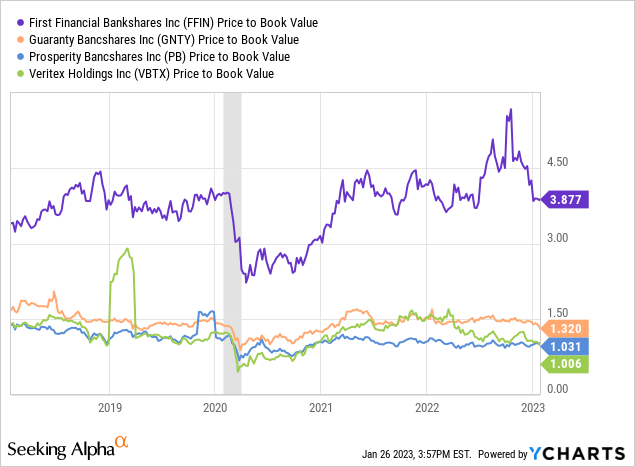

Moreover, when it comes to price to book value (for whatever that metric is worth), FFIN has long traded at a roughly 4x premium to peers.

Admittedly, there was a decent wave of insider buying (mostly from board members) in October 2022 at around $37-38 per share. Presumably, those same insiders should see FFIN as being even more attractive at $34-35 per share, but there has not been any more insider buying since October.

Bottom Line

FFIN is undoubtedly a well-run Texas bank, as 36 consecutive years of earnings growth is no easy feat to accomplish. I am no mathematician, but by my calculations, it takes a little over three and a half decades to rack up that kind of record.

FFIN has also been raising its dividend since 1997, with a two-year pause from 2008-2010 during the Great Recession. A pause, however, is a sign of strength, given the depth of pain suffered by many other small banks during that difficult period.

My uneducated assumption is that FFIN’s impressive record of consistent earnings growth and strong management are the reason why the market has awarded it with a valuation premium. But I would worry that the formula for FFIN’s successful and consistent growth in smaller Texas towns will not prove repeatable in the more highly competitive and faster growing Texas cities.

I would surmise that the reason FFIN has shed nearly a third of its market cap since the beginning of 2022 is because the market fears the same thing I do.

FFIN remains a “Hold” for now.

Be the first to comment