NicoElNino

Summary

Freshworks (NASDAQ:FRSH) is still undervalued in my opinion. Maintaining my original premise, I believe FRSH provides businesses with user-centric SaaS solutions that place an emphasis on simplicity of use and specific customer requirements. FRSH has a leg up on the competition thanks to the simplicity and scalability of its solutions, which facilitates the digital transformation of businesses in record time. With the updated forecasts and forward multiple, I am increasing my price target from $17 to $21 on FRSH stock.

Earnings overview

Amid a still difficult macro environment, FRSH reported 4Q22 results that were better than expected. Billings were up 29% year-over-year, slowing only slightly from the previous quarter. With higher win rates for both its CX and ITSM offerings, 4Q22 was the company’s most successful quarter for new business to date. DBNRR fell 300 basis points during the quarter to 110% as churn rates for smaller customers increased by less than 100 basis points while expansions slowed. Last but not least, FRSH, like many other growth software companies, guided a slower revenue growth of 17.5% y/y for FY23. However, margins and FCF guidance both reset to higher levels compared to market expectations. Despite a changing macro environment, I am heartened by the solid execution thus far. In the long run, I still think FRSH is an attractive asset thanks to its strong product portfolio and the fact that the market for its offerings is sizable but underserved.

Key metrics

Even though it isn’t a major concern right now, it’s important to note that the slower expansion motion reduces NRR and FRSH saw increased churn at the bottom. With the slowdown in the economy having an effect on business expansion, FRSH reported an NRR of 110%, down 300 bps from the previous quarter’s 113%. Gross dollar churn also increased slightly as FRSH notes a rise in churn at the bottom of the market. Fortunately for FRSH, the platform has become more relevant to larger customers as a result of changes to the product market team and to the products themselves. These elements are compensating to some extent for the more muted upsell environment brought on by the slowing hiring. Looking forward, management guided that its NRR will slow to 105% in Q1 due to increased risk, before leveling off in Q2. My expectation takes into account the possibility of a slight increase in gross churn in FY23, but I do expect expansion to be the primary drag.

As the software industry as a whole is feeling the effects of the weak macro environment, I believe FRSH can get away with these worsening metrics for the time being. Once we get past this, though, we have to see an improvement in these metrics, or else FRSH may start to look like it’s losing the war.

Customer wins

In addition to improved win rates, FRSH is also having greater upmarket success, especially in ITSM thanks to FreshService. Larger customer wins appear to be a result of the market’s appreciation for FRSH’s cost effectiveness, as well as the investments to address larger customers. During the quarter, the number of customers with an annualized revenue of more than $50,000 increased by 35% year over year to 1,908, and roughly 60% of all customers are midmarket or larger customers.

Guidance

A significant slowdown in growth was signaled by FRSH’s guidance, which called for a 17.5% y/y increase in constant currency. In addition, operating profit in the range of -$14 million to -$6 million suggests a margin of 1.7% for FY23. Also, something interesting to note is management guided to positive FCF each year going forward. FRSH also forecasts a 20% y/y increase in calculated billings. All in all, the projections were in line with consensus.

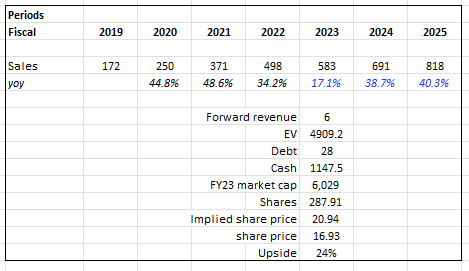

Valuation update

My previous price target was around $17, and the current stock price has hit that target. With the new guidance and valuation step-up, I believe FRSH still has another 24% upside to go before it reaches fair value.

Own estimates

Conclusion

FRSH is still undervalued in my opinion. Despite the current difficult macro environment, the company reported better than expected 4Q22 results with billings growth of 29% year-over-year and improved win rates for its CX and ITSM offerings. Fundamentally, FRSH is benefiting from its user-centric SaaS solutions that are simple and scalable, making digital transformation for businesses more achievable. However, there is some concern about the slowdown in business expansion and increased churn, but Freshworks’ success with larger customers and positive forward cash flow guidance are compensating factors. I have increased their price target from $17 to $21, implying there is 24% upside potential for the stock.

Be the first to comment