wildpixel

By now, Freeport-McMoRan Inc. (NYSE:FCX) bears should have given up their bearish calls, arguing that FCX and its copper-producer peers should fall back to reality as the global economy moves closer to a potential recession.

Dr. Copper’s price action in the futures market (HG1:COM) from its highs in June 2022 possibly led copper bears to assume the worst. However, we also highlighted in a note in August to our members that copper futures price action indicated a robust bottoming process, well before the Fed even telegraphed that it could slow down its rate hikes:

HG futures is also getting supported resiliently along its 200-week moving average (purple line) over the past five weeks, undergirded by a bear trap re-entry at its July lows. So, nothing has changed our bottoming thesis on copper; it’s constructive for the economy and the market. – 8 August 2022 Ultimate Growth Investing Pre-market briefing

Moreover, Freeport-McMoRan management also cautioned in October that the futures market didn’t reflect the physically tight supply/demand dynamics. CEO Richard Adkerson accentuated:

It’s striking how negative financial markets feel about this market and yet the physical market is so tight. We’re not seeing customers scaling back orders. Customers are really fighting to get products. – Bloomberg

Crucially, FCX made most of its gains from its bottom in July and September (pre-Q3 earnings in October). We also urged investors in July and early October to ignore the market pessimism and anticipate a recovery as the futures market forced a capitulation move. Hence, investors who managed to set aside their fears have outperformed the SPX substantially by picking those lows.

Also, high-conviction investors who believe that Freeport-McMoRan’s role as a leading copper producer in the metal undergirding the world’s transition to renewable energy sources would have found those levels attractive.

China’s rapid reopening from its COVID restrictions has also gotten the market excited recently. Weak holders who were forced by the market’s capitulation moves likely realized that the Chinese government is committed to returning the economy back into growth in 2023. As such, the government will likely continue to strongly support a recovery of China’s industrial activity and property sector, which augurs well for copper’s near- and intermediate-term demand.

With the IMF’s more sanguine outlook suggesting that the global economy could potentially avoid a hard landing this year, Dr. Copper has recovered well ahead of the SPX. Also, with the Fed likely closer to the end of its rate hike cadence, with the market anticipating an earlier pivot, copper futures price action has normalized.

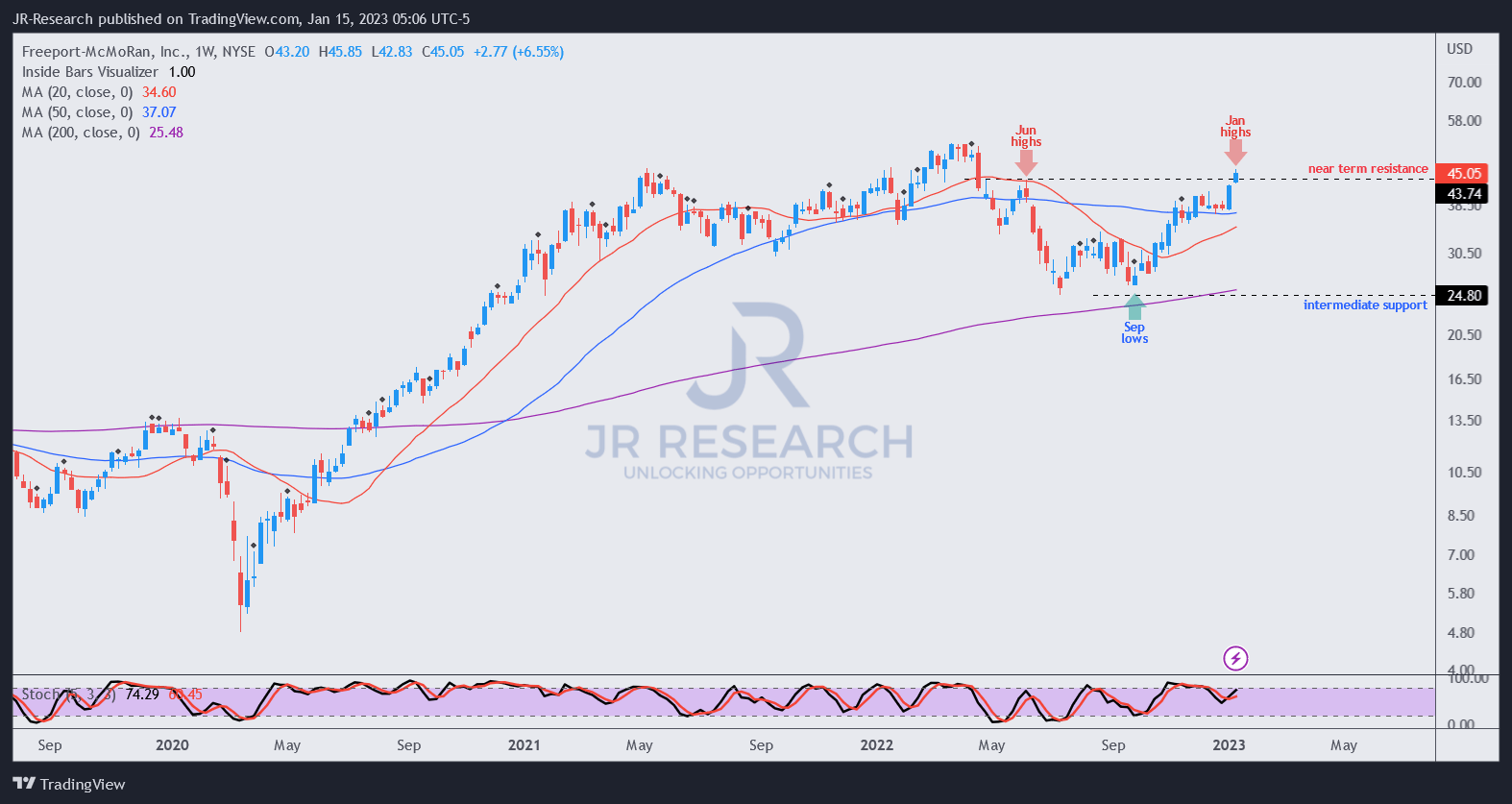

FCX price chart (weekly) (TradingView)

But, for weak holders who bailed out at the lows and waited for all the “stars to align” before returning to FCX, they would have missed out on its tremendous recovery, with FCX retaking its June highs last week. Yes, FCX has recovered the entire capitulation move from its June 2022 highs to its July/September lows. It has been an amazing run for FCX investors who braved the storm to add those lows.

FCX last traded at an NTM EBITDA of 9x, well above its 10Y average of 6.3x. With an expected recovery of its profitability through 2024 likely baking in a further recovery in copper prices, FCX’s FY24 EBITDA multiple of 6.7x is in line with its 10Y average.

Hence, FCX’s valuation seems well-balanced, and we don’t expect it to revisit the dislocations seen in July and September. Still, we anticipate a pullback to digest some of its near-term froth and help improve the reward/risk for investors who missed those lows.

Rating: Hold (Reiterated).

Be the first to comment