Brett_Hondow

If you’ve been to a restaurant anytime over the past year, you’ve likely been hit by sticker shock. In an inflationary environment, cash becomes less and less valuable, and that’s why I prefer to own dividend stocks that can help me buffer against higher costs of living.

Plus, it’s always nice to have interactions with businesses that you are a part owner of. For example, I always enjoy visiting a Simon Property (SPG) mall or outlet and with all else equal, would rather spend my money there than at another mall due to having shares in SPG.

This brings me to Four Corners Property Trust (NYSE:FCPT), which owns properties leased to a number of family-favorite restaurants across the U.S. This article highlights why FCPT is an appealing choice for income and growth, so let’s get started.

Why FCPT?

Four Corners Property Trust is a net lease REIT that specializes in restaurant properties across the U.S. Its portfolio is leased to major brands such as Olive Garden, Chili’s and Red Robin. At present, the company has ownership interests in 982 properties that are leased to 121 brands.

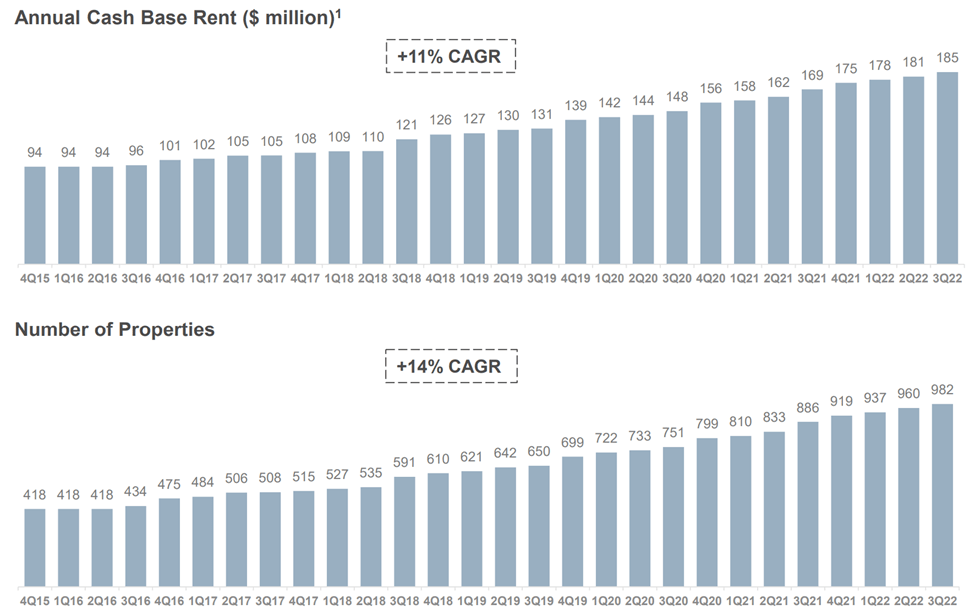

As shown below, FCPT has been a net consolidator, raising both its total cash rents and property count at a low to mid teens CAGR over the past several years.

FCPT Growth (Investor Presentation)

FCPT has also made good progress in diversifying its portfolio in recent years, since being spun off from Darden Restaurants in 2015. It’s since reduced its exposure to Darden from 100% at time of spin to 56% at present. It’s also diversified into essential non-restaurant retail properties, which now comprise 13% of its annual base rent.

Meanwhile, FCPT appears to be doing just fine in the current environment, with a 99.8% rent collection rate and 99.9% occupancy rate. Its tenant base also appears to be overall healthy, as they have on average 4.0x EBITDAR to rent coverage, and 86% of the properties are either corporate operated or guaranteed. Like most other net lease REIT, FCPT also enjoys a long-weighted average remaining lease term of 8.6 years.

Moreover, FCPT has demonstrated accretive growth on a per share basis, with AFFO per share growing by 5.1% YoY to $0.41 during the fourth quarter. It also benefits from a highly fragmented market, as reflected by the $166 million worth of acquisitions in the first nine months of 2022 alone, with an attractive initial cash yield of 6.4%.

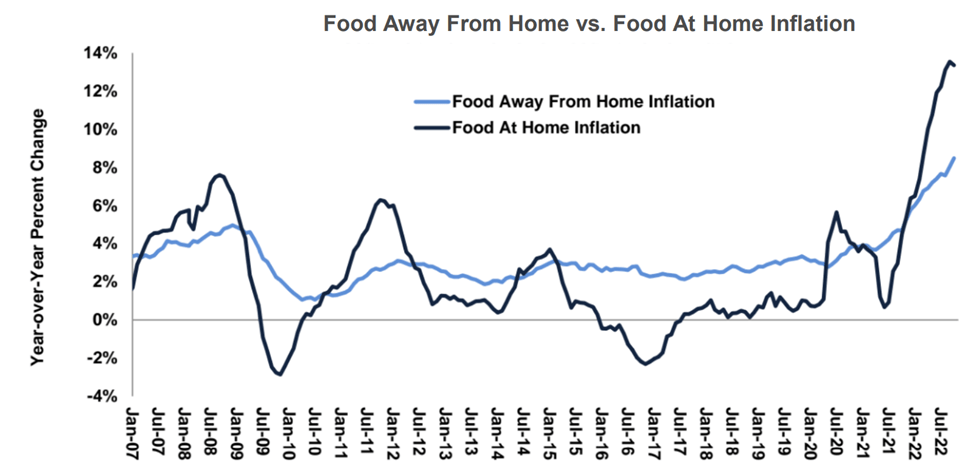

Risks to FCPT include the current inflationary environment, which may lead to consumer penny pinching. However, FCPT benefits from the fact that its restaurants are generally regarded as value brands, which appeal to cost conscious consumers. In addition, based on USDA and Bureau of Labor Statistics data, the cost of dining out has not risen nearly has much as the cost of eating at home, as shown below.

Food Inflation (Investor Presentation)

Meanwhile, FCPT maintains a strong balance sheet with BBB and Baa3 credit ratings from Fitch and Moody’s (MCO), and it carries a safe amount of leverage with a net debt to EBITDA ratio of 5.5x. Like most other REITs, FCPT’s debt maturities are staggered so that it can adjust expiring leases to match varying interest rate environments. FCPT’s next debt maturity is just $50 million in June of 2024.

Plus, while FCPT, like other REITs, now have a higher cost of new capital, property values have also come down, thereby making for more attractive pricing. This was reflected by management with regards to the deal pipeline in the recent conference call:

We are now regularly submitting offers at cap rates that are 50 basis points to 100 basis points higher than where those assets would have priced earlier this year. Some of those deals are already in the pipeline and are expected to close in the coming months.

Speaking of the rest of the year, we’ve built out a pipeline of properties with high-quality tenants in well-located retail corridors. We’re seeing more and more sale leaseback and outparcel opportunities. This influx is directly related to the rise in debt costs, making real estate sales a more attractive capital source on a relative basis. We anticipate that those opportunities will continue to present themselves into 2023.

Importantly, FCPT now yields a respectable 5.2%, and the dividend is well covered by an 83% payout ratio, based on Q3 AFFO per share of $0.41. Management has also rewarded shareholders with a 5-year dividend CAGR of 6%.

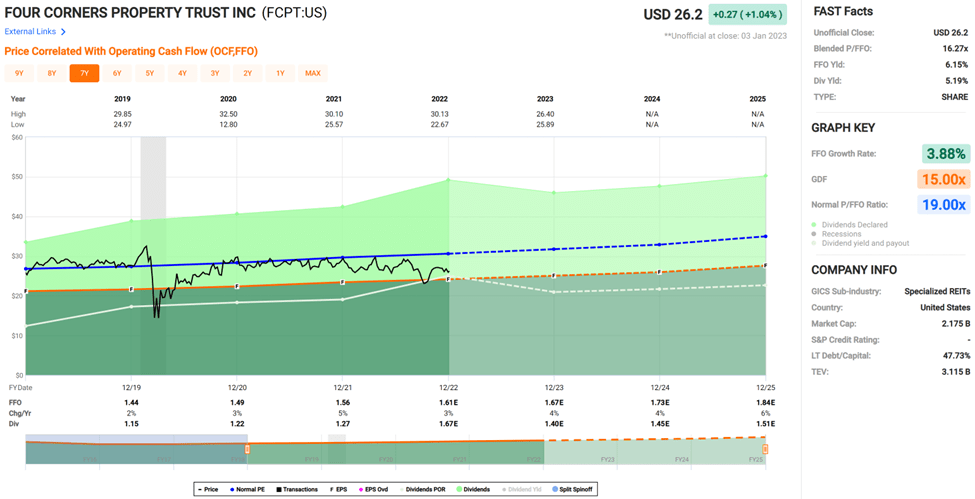

Lastly, I find FCPT to be appealing at the current price of $26.20 with a forward P/FFO of 16.2. Admittedly, FCPT doesn’t scream cheap, but it does sit below its normal P/FFO valuation of 19.0. FCPT could see a long-term FFO/share annual growth rate of 5%, which combines with the 5% dividend rate to produce a respectable 10% expected annual return. Analysts seem to think so too, with an average price target of $27.50, translating to a potential 10% total return over the next year.

FCPT Valuation (FAST Graphs)

Investor Takeaway

All in all, FCPT remains an attractive option for income focused investors. It has healthy portfolio metrics, no near-term debt maturities, and continues to find attractive acquisition targets. It also carries a strong balance sheet and pays a well-covered and growing dividend. Lastly, I find FCPT to be attractive at the current price for potentially rewarding long-term returns.

Be the first to comment