Nathan McDaniel

Introduction

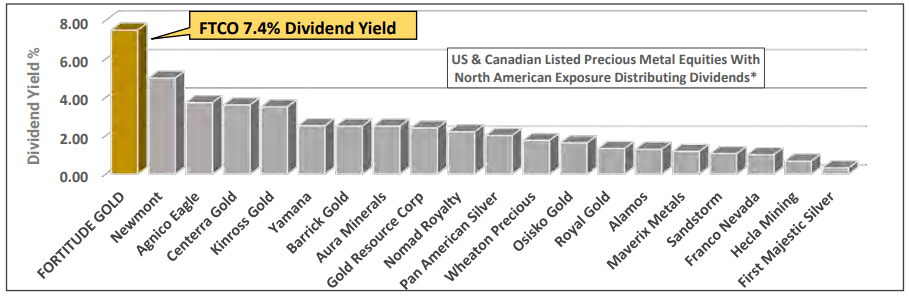

Fortitude Gold (OTCQB:FTCO) is a high-dividend gold producer focused on Nevada, which I covered on SA in November 2021. The company has all-in sustaining costs (AISC) of below $800 per ounce and currently pays out a monthly dividend of $0.04 per share. This translates into a yield of over 7% which puts it miles ahead of other gold mining companies.

Fortitude Gold

However, the life of mine of Fortitude Gold’s flagship project is now less than 3 years and even higher gold prices haven’t been able to make a difference. In my view, it’s unlikely that the company will manage to add a satellite pit with good grades before reserves run out, and I’m bearish.

Overview of the recent developments

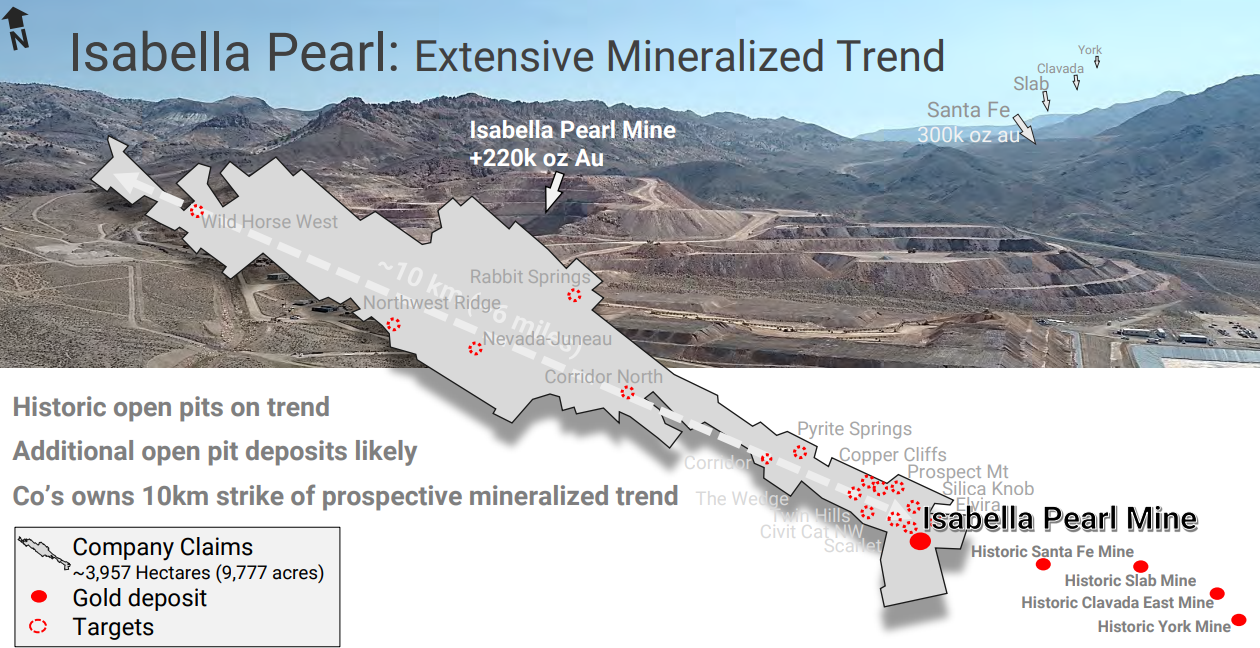

Fortitude Gold is a 2020 spin-out of Gold Resource (GORO) and its main project is the Isabella Pearl gold mine in the Walker Lane Mineral Belt.

Fortitude Gold

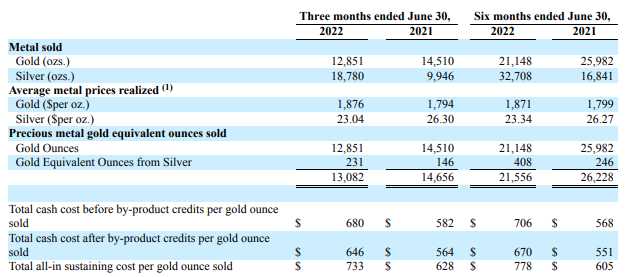

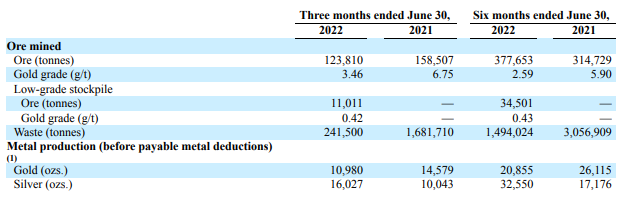

This is a relatively small heap leach mine with an annual output of about 40,000 ounces of gold, but its grades are really high, which leads to one of the lowest unit costs in the entire world. In Q2 2022, Fortitude Gold sold a total of 13,082 ounces of gold equivalent at AISC of just $733 per ounce. Gold production for the period stood at 10,980 ounces and the average grade was 3.46 g/t. Considering most gold mines today have average grades of about 1-2 g/t, this is pretty high. Yet, it’s much lower than a year ago, as it seems that higher grade zones are exhausted.

Fortitude Gold Fortitude Gold

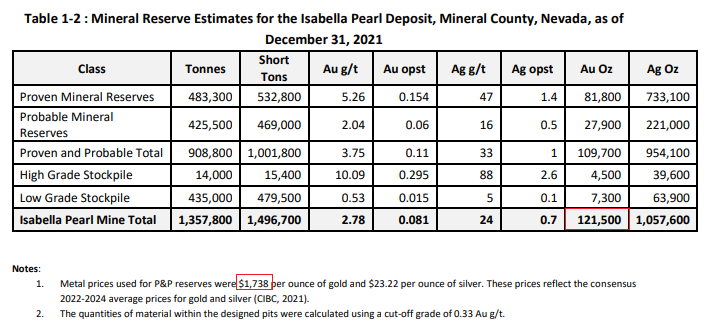

I think costs could increase to about $900 per ounce in the near future as the grade should continue to drop. After all, the average reserve grade is 2.78 g/t. Speaking of reserves, I find it weird that Fortitude gold is using 220k oz in its corporate presentation, considering this is the figure for the end of 2019. As of December 2021, Isabella Pearl’s reserves were down to only 121,500 ounces and this is despite an increase in the gold price used to calculate them from $1,306 per ounce to $1,738 per ounce in two years.

Fortitude Gold

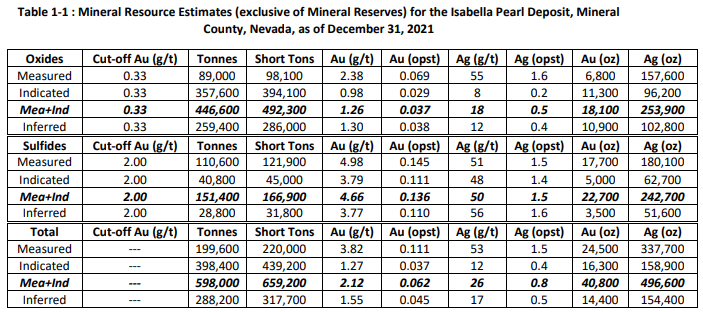

This leaves me wondering how much gold prices need to increase for the 40,800 ounces of measured and indicated gold resources to become reserves.

Fortitude Gold

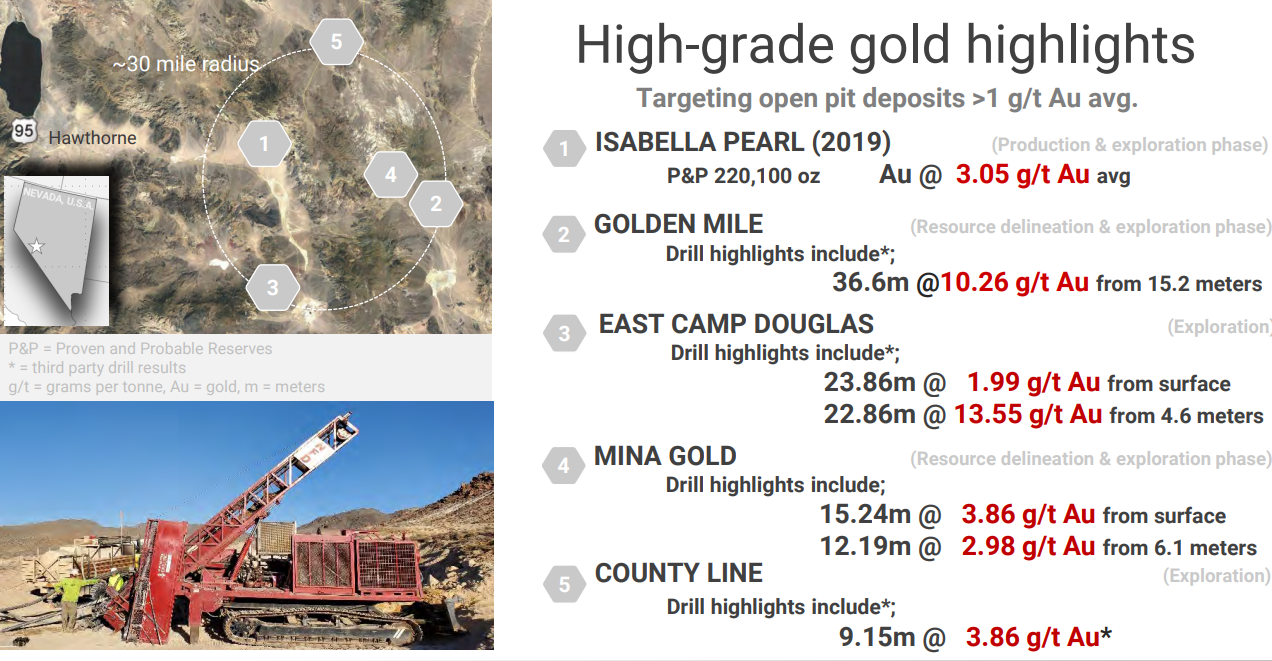

In H1 2022, Fortitude Gold produced a total of 20,855 ounces of gold which means that there are around 100,000 ounces of gold reserves left and that there are about 2.5 years before Isabella Pearl is depleted. So, what are the paths forward? Well, Fortitude Gold could try to find more gold zones at the property. However, Isabella Pearl has already been explored extensively with a total of 568 holes for 51,462 meters drilled there since 1987 so finding more gold there will be tough. The other viable option is to use some of the nearby properties as satellite deposits.

Fortitude Gold

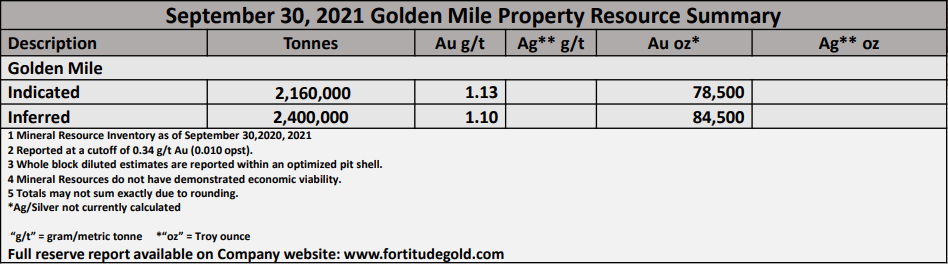

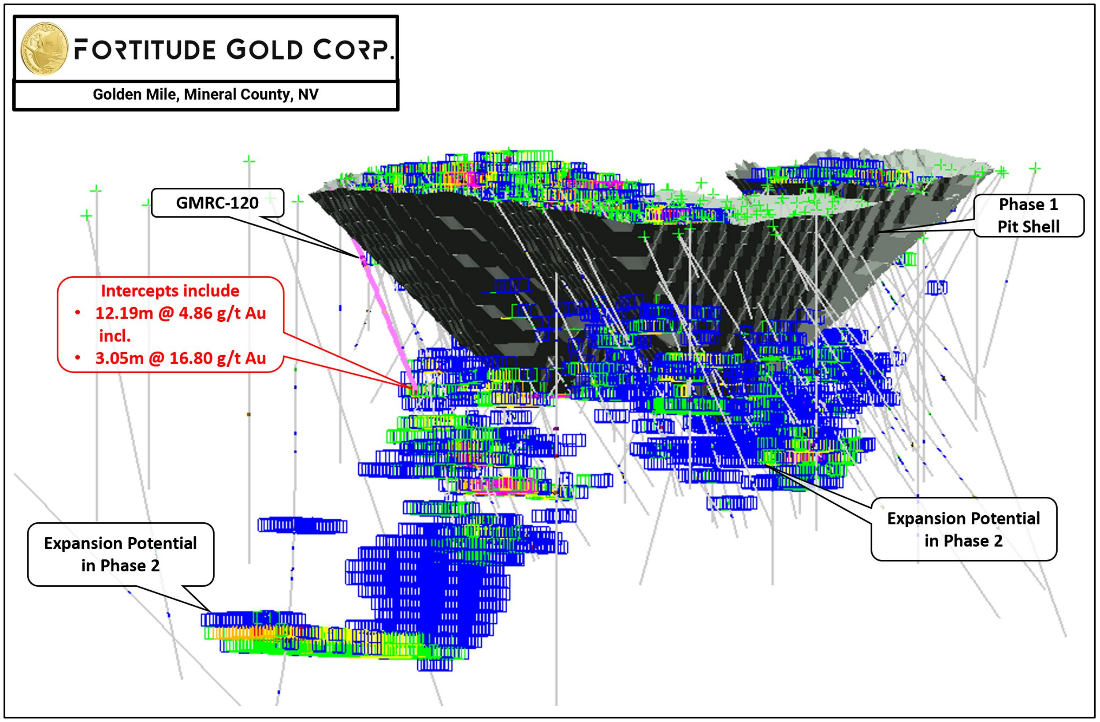

At the moment, Fortitude Gold is drilling at Golden Mile and the latest assays include an interception of 3.05m of 16.80 g/t gold. However, it seems that high-grade zones are narrow as the project indicated resources of just 78,500 ounces of gold at an average grade of only 1.13 g/t

Fortitude Gold

Considering that carbon will need to be trucked for processing into dore at Isabella Pearl’s ADR plan and that the grades are around three times lower, I doubt that this deposit is economically feasible at today’s gold price of $1,770 per ounce. In addition, a lot of the mineralization is located over 50 meters below the surface, which means that significant funds will need to be invested into pre-stripping.

Fortitude Gold

Fortitude Gold plans to complete a pre-feasibility study for Golden Mile by late 2022 or early 2023, but I’m not optimistic about the results. The issue here is that all of the other nearby projects are in an early stage, and none of them even has a resource estimate. All of this means that with reserves running out at Isabella Pearl in early 2025, the company’s only path forward is the transition of mining to Golden Mile.

Overall, I think that Fortitude Gold is overvalued at the moment, as its market valuation stands at $159 million as of the time of writing. As of June 2022, the company had $40.7 million in cash, and optimistically assuming AISC stay below $800 per ounce gives us a net income of around $59 million between July 2022 and December 2024 (based on Q2 2022 results). That being said, I think that short-selling Fortitude Gold stock could be dangerous as the prices of commodities are notoriously volatile and gold isn’t an exception. I think it could be best for risk-averse investors to avoid this stock.

Investor takeaway

Isabella Pearl is a high-grade gold mine that has allowed Fortitude Gold to deliver the highest dividend yield in the gold mining sector for the past year, but its reserves are running out soon and the company hasn’t managed to find good alternatives so far. The project has been drilled extensively, and the only advanced stage deposit nearby has grades of just above 1.1 g/t. I think that AISC for Golden Mile are likely to be around $2,000 which makes this operation uneconomical at today’s gold prices.

Overall, it seems like the Fortitude Gold’s golden age is set to end around the end of 2024 and this is why I think the company is overvalued. However, short selling is dangerous in the mining space due to price volatility, so risk-averse investors are probably better off avoiding this company. In case you have high risk tolerance, data from Fintel shows that the short borrow fee rate stands at 2.3% as of the time of writing. Unfortunately, there are no call options available, so you can’t hedge the risk, though.

Be the first to comment