BlackJack3D

Investment Thesis

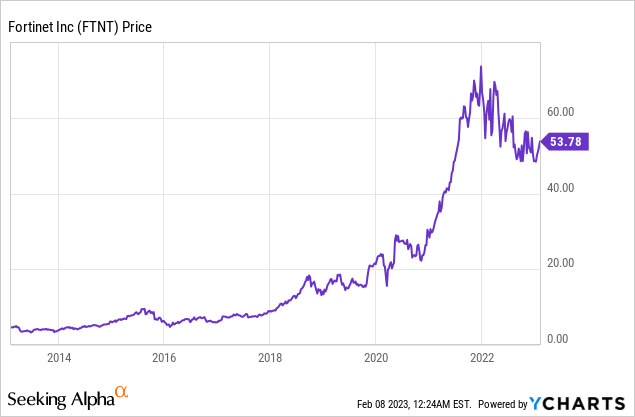

Fortinet, Inc. (NASDAQ:FTNT) is a U.S.-based cybersecurity company founded by Xie Jing back in 2000. The company has been one of the best compounders in the past decade, with the stock up over 1,000% during the period. The share price has also been holding up well despite the broad market selloff.

Cybersecurity has a massive TAM (total addressable market) and continues to benefit from secular tailwinds. It is one of the most resilient industries that capture non-discretional spending. The company is also expanding its TAM by entering other verticals, which should open up more growth opportunities moving forward. Some investors are skeptical about the company’s prospects, as it generates a large portion of revenue from on-premise products, but the segment continues to grow rapidly despite the shift to cloud security. This is reflected in its latest fourth quarter earnings reported yesterday with upbeat product growth and profitability. The current valuation also isn’t too expensive on a historical basis, especially when considering the growth it is showing. Therefore I rate Fortinet, Inc. as a buy.

Huge Market Opportunity

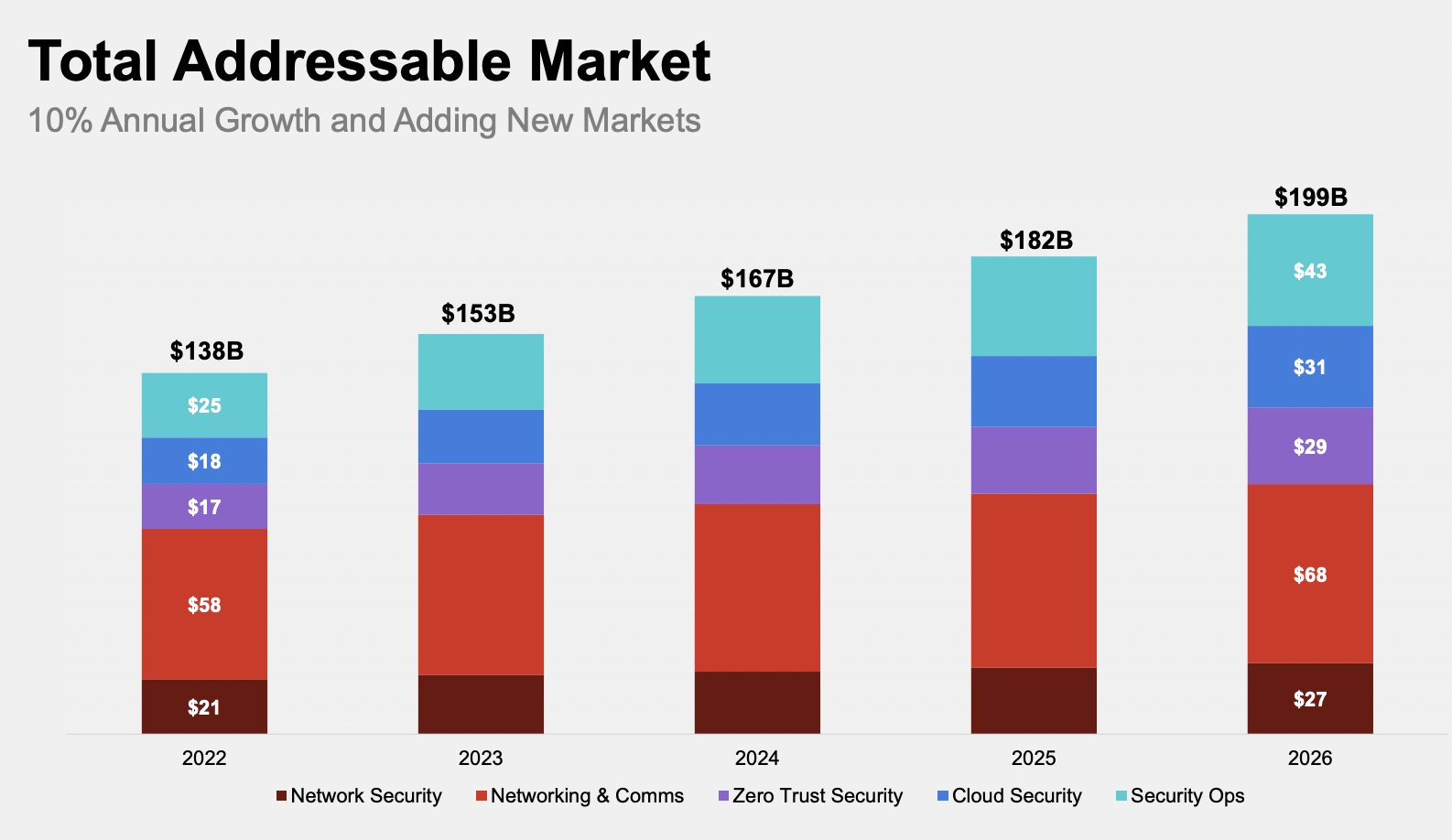

Cybersecurity is a massive and fast-growing market. According to Grand View Research, the TAM for the industry is $222.66 billion in 2023 and is forecasted to grow to $500.7 billion in 2030, representing a CAGR (compounded annual growth rate) of 12.3%. Fortinet estimates its own TAM to be $153 billion in 2023, and it should grow at a CAGR of 10% to $199 billion in 2026. While network security often seemed to be overlooked due to the shift to cloud, it actually accounts for $22.5 billion of the TAM. although it is growing at a slower rate. The company’s expansion into new markets like cloud security and zero trust also added nearly $40 billion in TAM, and these segments are also growing much faster. Fortinet’s current penetration rate is only around 2.4% despite being such a large company.

Fortinet

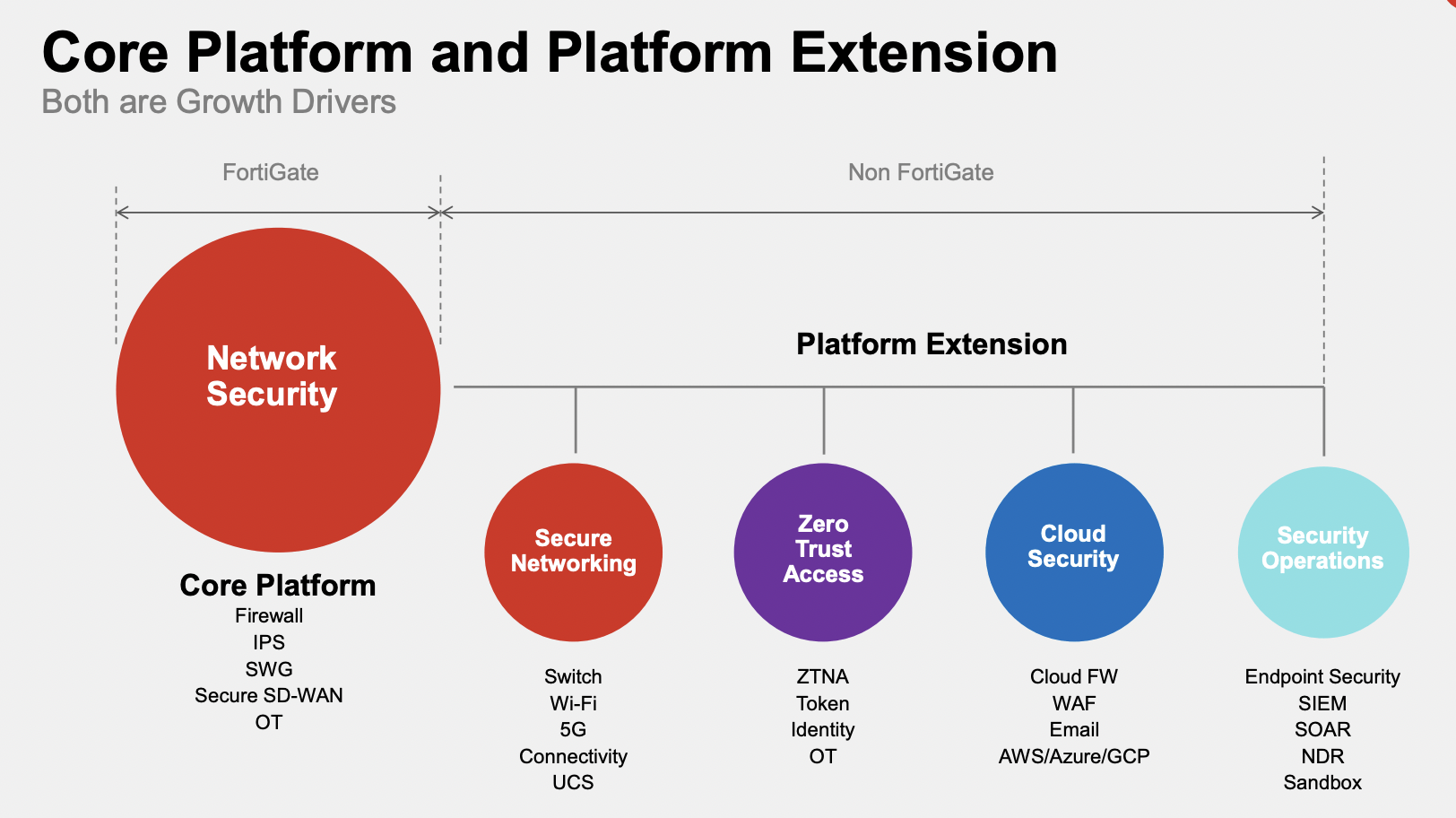

The industry is growing quickly due to digital transformation and IoT (internet of things). The penetration rate of the internet and cloud has increased significantly in the past few years which also increased the number of cyberattacks. This vastly increased the demand for more sophisticated cybersecurity solutions as the cost of cyberattacks is huge, especially for big firms. While cloud security benefits from workloads shifting to the cloud, network security is also relevant as many companies are adopting a hybrid approach. Companies still need firewalls and the company dominates in this space. The industry is also seeing a consolidation in vendors as customers want to reduce complexity. This benefits larger vendors like Fortinet as it has a broad product portfolio that addresses different areas.

Keith Jensen, CFO, on vendor consolidation:

There’s been an explosion of devices that must be connected to the cloud, data center and edge compute. As a result, the infrastructure has expanded to support secure connectivity via distributed firewalls, it is no longer feasible to overlay security on top of networking in the data center. They must be deployed as a converged solution. Firewalls need to work seamlessly with networking and security applications across the company’s entire infrastructure. Fortinet is leading the convergence trend with a wide range of technologies, including network firewalls, Secure SD-WAN, 5G and OT security, all embedded in our single operating system delivered as hardware, software, cloud and as a service.

Fortinet

Q4 Earnings

Fortinet just reported Q4 earnings, and I think the results are very strong considering the macro environment, especially product revenue and the bottom line. The company reported revenue of $1.28 billion, up 33.1% YoY (year-over-year) compared to $963.6 million. The growth is mainly driven by product revenue, which increased 42.5% from $378.9 million to $540.1 million, now accounting for 42.2% of total revenue. During the year, it added over 23,000 new customers for its firewall products. Service revenue grew 27.1% YoY from $584.7 million to $742.9 million, driven by the increase in security subscriptions. Billings for the quarter was $1.72 billion, up 31.6% YoY. Gross profit was $985.7 million compared to $735.3 million with the gross margin flat YoY.

Ken Xie, CEO, on FY22 results:

For the full-year, revenue growth accelerated to 33%. We continue to gain market share in the service security industry with customers increasingly recognizing how Fortinet integrate and a single platform approach to security delivers along total cost of ownership and a greater return on investment than competing solutions.

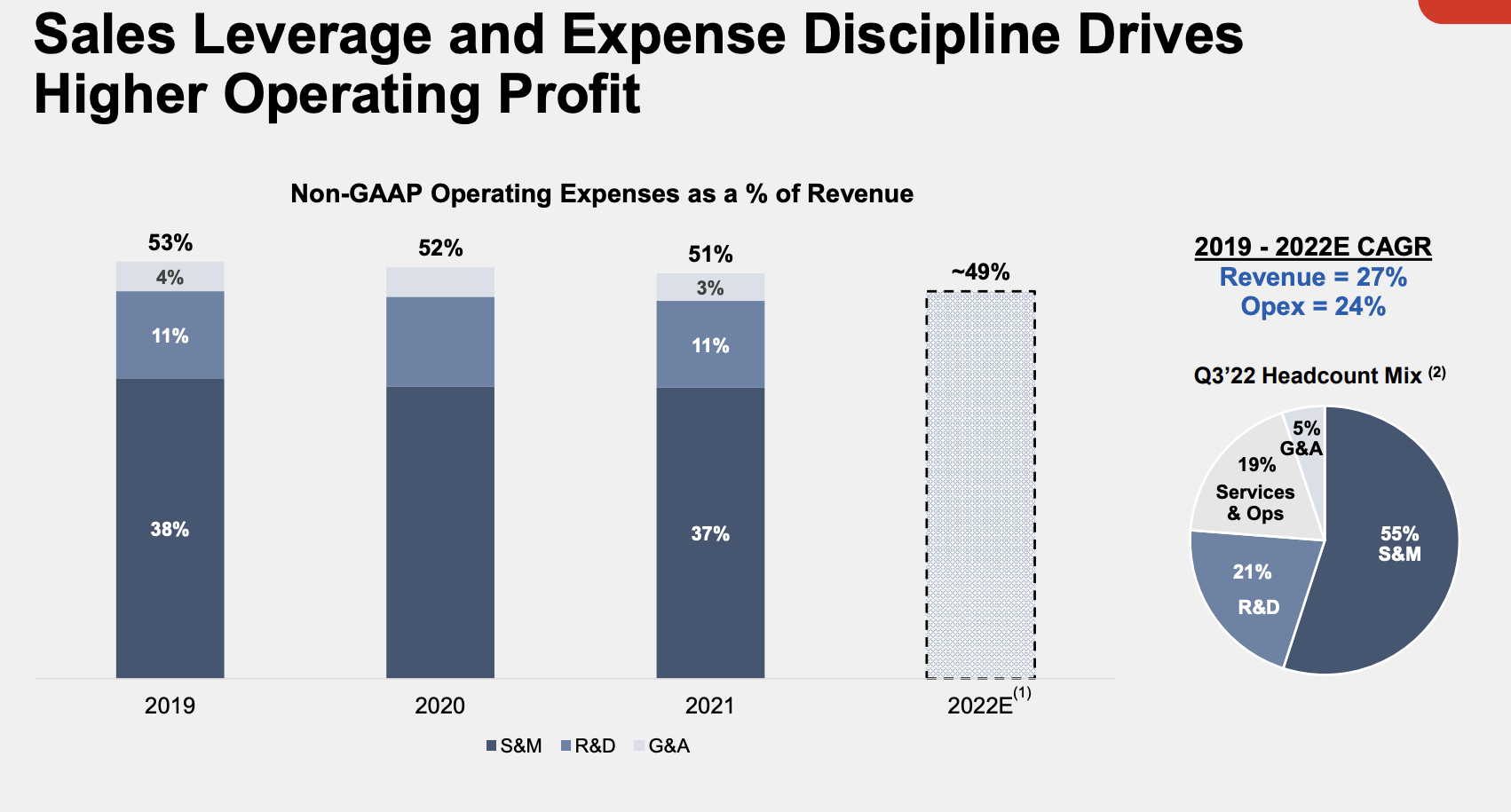

The bottom line is extremely impressive as the company continues to show strong operating leverage. Despite revenue up over 33%, operating expenses only increased by 20.7% to $627.9 million. This is mostly contributed by S&M (sales and marketing) expenses which grew 24% YoY from $367.7 million to $455.9 million. The discipline in operation spending resulted in operating income increasing over 66.5% YoY from $214.9 million to $357.8 million. Operating margins also improved significantly from 28.5% to 32.5%. EPS for the quarter was $0.40 compared to $0.24, or a 67% increase YoY. It guided revenue for FY23 to be $5.37 billion to $5.43 billion vs $5.35B consensus, representing a solid growth of 22% at the midpoint. The company ended the quarter with only $990 million in debt and $1.68 billion in cash, with provide ample financial flexibility for investments or further share repurchases.

Fortinet

Investors Takeaway

Fortinet, Inc.’s Q4 earnings once again demonstrated why it is one of the best cybersecurity companies in the world. Despite investors’ pessimistic view of the product segment, Fortinet still managed to grow product revenue by a whopping 42.5% and added over 6,200 new logos during the quarter. Its strong reputation also helps minimize the S&M spending needed, which resulted in an exponential increase in operating income and EPS.

Considering the huge TAM and its low penetration rate, I believe Fortinet, Inc. can continue to put up consistent growth over the long run, not to mention its opportunities in newer and emerging segments. The current valuation is also not really expensive by historical standards. Fortinet is trading at a fwd price-to-FCF ratio of 23.92x which I believe is very fair, considering its strong growth rates. This is slightly lower than its 5-year historical average of 24.17x. As Fortinet, Inc. continues to scale, the ratio should go down pretty quickly, given the strong operating leverage it has. Therefore, I rate Fortinet, Inc. as a buy.

Be the first to comment