We Are

We had previously covered Ford Motor Company (NYSE:F) here, discussing the massive tailwind for growth, attributed to the robust consumer demand for the F-150 Lightning. Its partnership with multiple battery makers also proved critical to the 2M EV ramp-up through 2026, particularly with Contemporary Amperex Technology [CATL]. These strategies might boost the stock closer to the consensus price target, partly attributed to CATL’s new technology’s doubled battery capacity.

For this article, we will focus on F’s strategic choice in announcing a supplemental dividend in the FQ4’22 earnings call, supporting its stock price despite the underperforming quarter. However, the stock may remain volatile over the next few weeks, attributed to the temporary price appreciation from short-term traders and the potential margin compression from the price war to retain its market share in the EVs market. We shall discuss this further.

The Dividend Investment Thesis Remain Somewhat Safe For Now

There had been many whom voiced their doubts on whether F’s dividends remained safe moving forward, which we echoed as well.

F generated a robust Free Cash Flow of $9.1B (+97.8% YoY) in FY2022, with the guidance of $6B in FY2023. While the FY2023 number may indicate a notable -34.1% headwind YoY, we must highlight that it is attributed to the projected capital expenditure of up to $9B in FY2023, growing by 31.1% YoY from FY2022 levels of $6.22B and 17.9% from FY2019 levels of $7.63B.

This highlights F’s continued investments towards the BlueOval City in the US, which may expand its total EVs production output to 2M by 2026. We reckon these efforts may eventually be top and bottom line accretive, justifying its aggressive planned EV spending of $50B over the next few years.

In the meantime, F reported robust cash/investments of $32.18B in FQ4’22 (-11.7% YoY from $36.45B and +44.4% from FQ4’19 levels of $22.28B), despite “leaving $2B of profits on the table” due to cost and supply chain issues.

Much of this was attributed to the growing leverage in F’s long-term automotive debts at $18.71B by the latest quarter, +11.9% YoY against $16.71B in FQ4’21, and +37.4% from $13.61B in FQ4’19. However, investors must also note these already constituted massive improvements from the peak pandemic debt levels of $37.87B in FQ2’20. In addition, its net debts levels appeared more than decent at -$13.47B, compared FQ4’19 levels of -$8.67B.

In addition, the F management had been highly prudent in monitoring its leverage, switching from the original high-interest hyper-pandemic debts to lower-interest longer-term debts. By FY2022, the company only paid $1.28B of annual interest expenses, compared to $1.79B in FY2021 and $1.65B in FY2020. Its debt maturity had also been extended through 2062, suggesting the capital market’s confidence about its forward execution and the improved intermediate term liquidity even considering its expansion plans.

Therefore, while we may not agree with the F management’s choice to introduce a supplemental dividend worth approximately $2.6B, based on the latest share count of 4,005M shares outstanding, it appears that F may well afford it now.

However, investors must not expect another supplemental dividend in the short-term, since it was attributed to the monetization of F’s stake in Rivian Automotive, Inc. (RIVN). By selling approximately 91M shares, F unlocked $3B worth of proceeds in FY2022, with only 1.15% RIVN-stake remaining at the time of writing. Notably, we must also highlight that the company had reported -$7.37B of RIVN-related write down at the same time.

We posited that the strategic timing of the supplemental dividend had tempered some of the FQ4’22 profitability headwinds, since the F stock continued to trade optimistically nearer to its November 2022 resistance levels. This was significantly aided by decent FY2023 guidance in adj. EBIT of up to $11B, against FY2022 levels of $9.69B and FY2019 levels of $4.92B.

On the other hand, the F management decided to unexpectedly engage Tesla (TSLA) in the EV price war, discounting the Mustang Mach-E by -$4.5K to an average price of $45.99K. This was odd, since the model was already priced reasonably below the $55K cap prior to the discount, qualifying buyers to the $7.5K Inflation Reduction Act tax rebate then. It was opposed to TSLA’s reduction by -$8K for the Model Y at $54.99K, below the SUV price cap of $80K.

Then again, since the discount is only applicable to the Mustang Mach-E, the impact may be muted indeed, due to the model’s projected annual production output of 130K in 2023. Those numbers suggest an estimated $585K impact on F’s top line in FY2023, which may prove necessary to retain market share, since TSLA’s Model Y arguably remains better-ranked that F’s Mach-E thus far. Marin Gjaja, Chief Customer Officer in Ford, said:

We are not going to cede ground to anyone. We are producing more EVs to reduce customer wait times, offering competitive pricing and working to create an ownership experience that is second to none. (Seeking Alpha)

For now, TSLA could well afford the compressed margins, since it recorded stellar gross margins of 25.6% and adj. net income margins of 17.3% in FY2022. On the other hand, F might suffer from reduced profitability ahead, since it reported very tight margins of 10.9% and 5.1% in FY2022, respectively.

Combined with FY2022 results that were “below expectations attributed to execution issues,” only time will tell how this strategy may play out for F.

So, Is F Stock A Buy, Sell, or Hold?

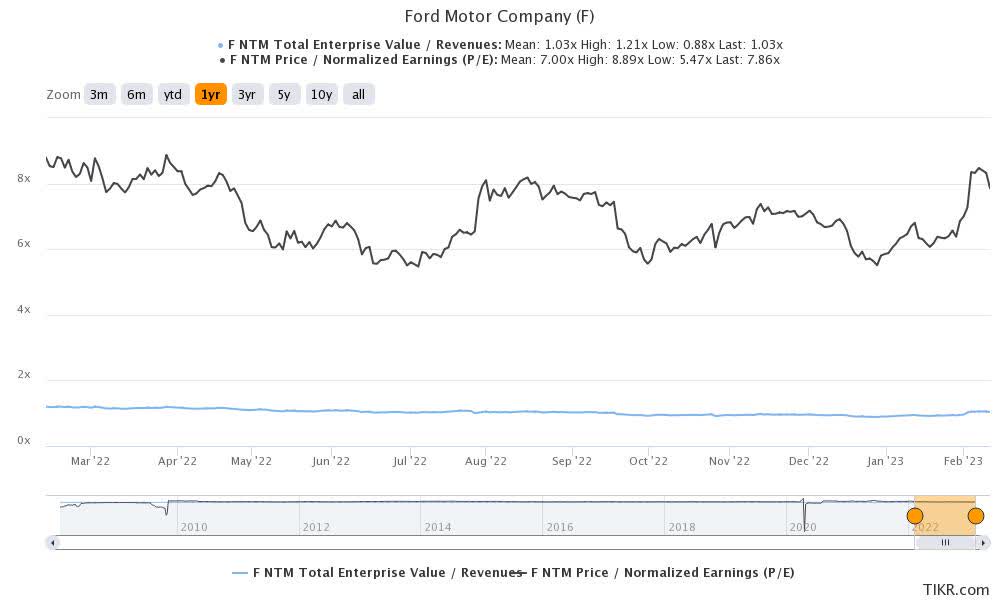

F 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

F is currently trading at an EV/NTM Revenue of 1.03x and NTM P/E of 7.86x, lower than its 3Y pre-pandemic EV/Revenue mean of 1.16x though higher than its P/E mean of 7.11x. Otherwise, it is still higher than its 1Y mean of 1.03x and 7.00x, respectively.

Based on F’s projected FY2024 EPS of $1.67 and current P/E valuations, we are looking at a moderate price target of $13.12. This mirrors the consensus estimates of $13.00 as well, suggesting a minimal upside potential from current levels.

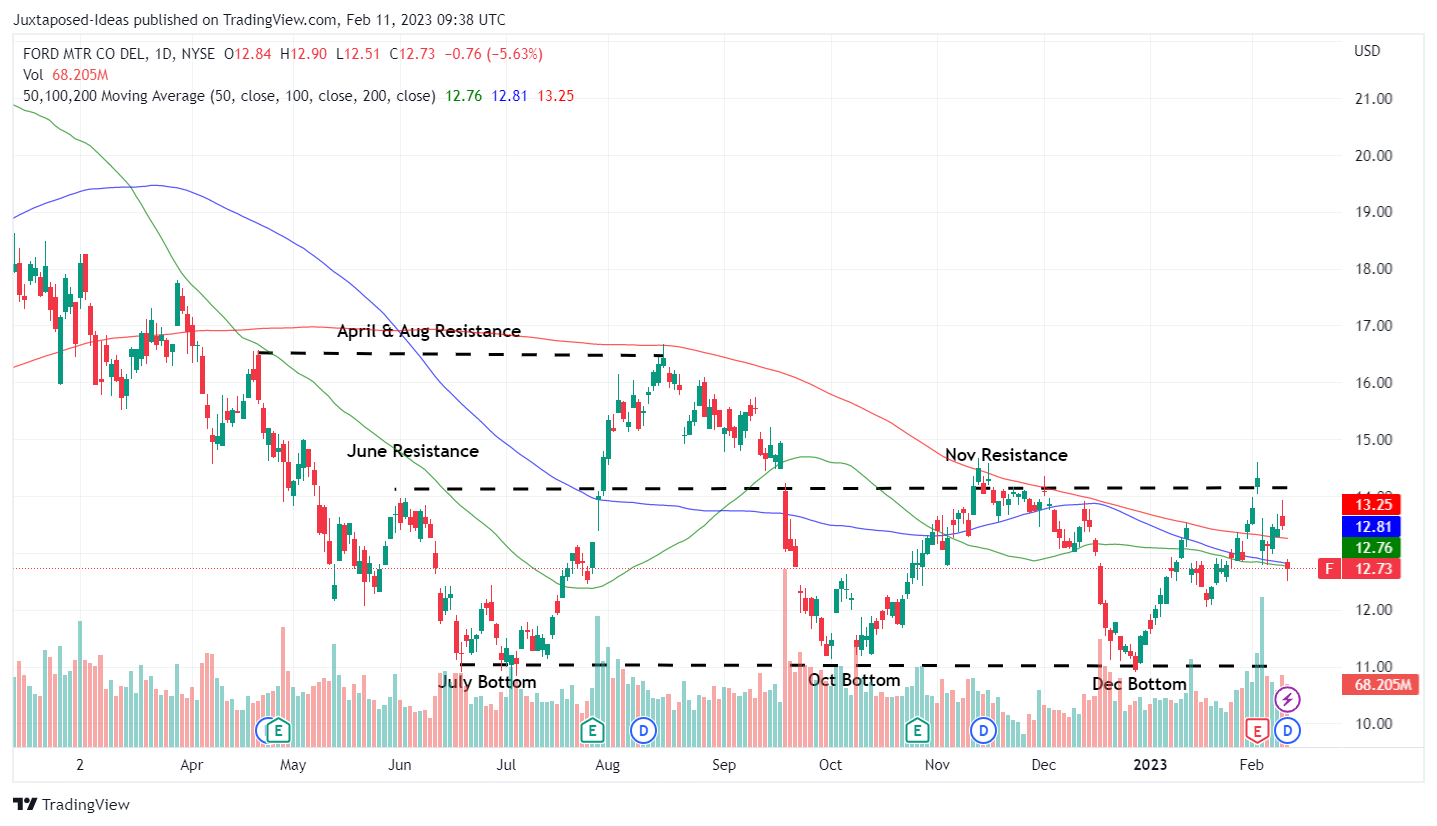

F 1Y Stock Price

Trading View

The recent optimism was likely attributed to management’s decision to declare a supplemental dividend of $0.65 payable on 01 March 2023, on top of the quarterly dividend of $0.15.

As with most cyclical stocks, we reckon there might be some volatility in the short term, caused by opportunistic traders looking for a quick profit. This may be corrected by mid-February 2023, once some selling pressure occurs now that the ex-dividend date of February 10, 2023 has passed.

Otherwise, long-term F investors should simply sit back and enjoy this special gift, especially due to the stellar forward dividend yield of 4.54%, against the 4Y average of 3.75% and sector median of 2.05%. Investors looking to drip may wait for another dip, preferably at $11.

Be the first to comment