Mercury outboard engine

Cineberg/iStock Editorial via Getty Images

- Brunswick is dominant in boating, has a good financial position, low P/E ratio, and a capable management.

- Demand for its products is highly sensitive to macroeconomic conditions — especially unemployment and short-term interest rates.

- On balance, the probability is that currently “good” low unemployment rates will rise while interest rates remain relatively high. If so, earnings growth will face headwinds and the share price is unlikely to surpass its peak price of 2021, at least not anytime soon.

- A neutral-to-moderately bearish rating seems appropriate.

Overview

Brunswick management has done a good job in focusing on the marine business and leaving the bowling/sporting goods sector to others. No more bowling for dollars: the division was sold to a private equity firm in 2015.

The marine product line includes high-quality brand names like Mercury, Sea Ray, Fliteboard, Boston Whaler (saltwater fishing), Bayliner, Quicksilver, Lund (freshwater fishing) and Veer in electrics.

Brunswick is not a tiny company, as it employs 18,000 people in 27 countries and has been awarded 650 patents since 2017. And it’s the only company making outboard engines above 450 horsepower.

This branding and underlying technology accounts for an important part of Brunswick’s intangible value and has helped make the company the largest boat manufacturer in the world. In conjunction, Brunswick has also added the Freedom Boat Club to its services offerings. Brunswick projects that by the end of 2027 paid memberships will total 80,000 and spread over 500 locations.

Post-pandemic demand for consumer goods has been boosted by federal fiscal stimulus, low unemployment, and interest rates that have risen sharply above zero but have not been too prohibitive yet. As a result, the company forecasts/hopes that annual boat unit sales will soon start to move above the 215,000 unit peak of 2020. Recent stabilization of interest rates has been of some, probably modest, benefit to consumers financing purchases with monthly payment loans. In all, boat registrations have remained within the 10.3 to 10.5 million units per year for at least a decade.

Estimated diluted earnings per share are expected to be something above $7.00 for 2024 and $8.00 for 2025 as compared to diluted continuing operations EPS of $6.13 in 2023 versus $9.06 in 2022. Revenues in 2023 were $6.4 billion versus $6.8 billion in 2022. Company projections suggest, however, that EPS of $15 are attainable in 2027.

In my opinion, the only way for this to happen will be if there’s at worst a brief “soft landing” for the overall economy. Given a still inverted yield curve and ongoing wars, this outcome seems unlikely to me.

The balance sheet is also in good condition with long term liabilities of $2.4 billion (debt of $1.98 billion) that can be readily handled by company-estimated free cash flow in 2024 of around $500 million and company projections of cumulative $2.5 billion over the next three years. Low-rate debt ($450 million at 0.85%) however, will need to be refinanced in 2024. The share repurchase plan assumes $150 million per year through 2027.

New product line additions include electric boat engine versions that might reduce the company’s sensitivity to oil price increases in the future. However, the electrics’ unit volume is still too small to have a meaningful impact, and I’d personally question the viability of placing charging stations in open waters.

Rather than further duplicating the deep financial analyses and projections that appear in previous Seeking Alpha articles by other authors, I present an econometric approach that leads me to conclude that near and medium term investors ought to consider sale of the shares.

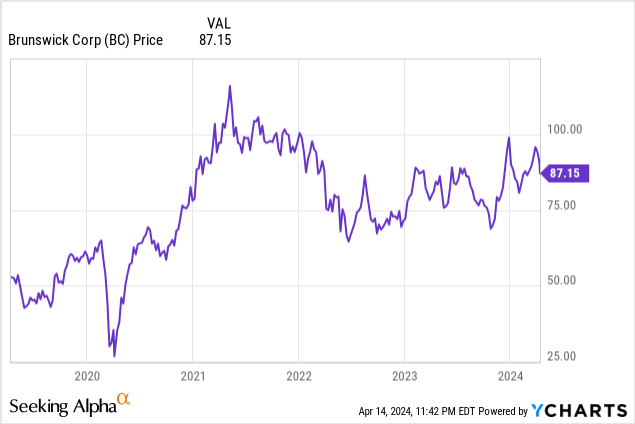

According to reported government data, not all of which in my opinion is an accurate reflection of true conditions, the unemployment rate is low, the inflation rate has decelerated, the Fed might soon be cutting interest rates at least once or twice, and the wealth effect of a stock market near an all-time peak presents an ideal environment for purchases of pleasure boats and related services. One would think that under such “ideal” conditions that BC shares would be scratching at new highs rather than more or less going sideways since the high of $107 back in April 2021.

It seems to me that the probability of something “going wrong” with such a rosy current economic scenario is rather high. Wars in the Middle East and Ukraine are at the top of the list, but there’s also probable re-acceleration of inflation, record consumer credit card debt exceeding $1 trillion, default rates on auto and boat loans rising, insurance costs going up noticeably, some commercial real estate values cut in half (or more), and so forth.

Econometric Considerations

Econometrics is a mix of art and science, and the statistics spewed by regression models should only be taken as suggestions, not conclusive proofs.

In the following analysis, however, the strong suggestion is that pleasure boating sales — the key component of Brunswick’s operational performance and therefore stock price — are inversely sensitive to changes in unemployment and short-term interest rates (3-month t-bills). Oddly, perhaps, rising oil prices seem to have a small positive effect on demand.

In this case, I’ve regressed obvious annual metrics such as the unemployment rate, 3-month t-bill interest rates, and oil price changes on personal consumption expenditures for pleasure boats. There are other variables that might also be included: insurance costs, consumer sentiment metrics, new and used car and boat prices, etc. But for the sake of time, space, and effort, I’ve tried to keep this analysis as simple as possible.

The significant variables here (with p-values near zero) are unemployment and interest rates, which as expected have negative coefficients, while the change in the price of oil has a positive coefficient. (This is probably an effect of oil price volatility over the 44-year sample, and I’d suspect that higher oil prices may actually sometimes dissuade pleasure boat purchases.)

|

Dependent Variable: BOATS |

||||

|

Method: Least Squares |

||||

|

Date: 04/14/24 Time: 21:53 |

||||

|

Sample: 1980 2023 |

||||

|

Included observations: 44 |

||||

|

Variable |

Coefficient |

Std. Error |

t-Statistic |

Prob. |

|

UNEMPLRATE |

-1968.332 |

326.3169 |

-6.031965 |

0.0000 |

|

TBILLS |

-472.4244 |

166.1198 |

-2.843877 |

0.0069 |

|

LOG(OIL) |

6903.098 |

514.4650 |

13.41801 |

0.0000 |

|

R-squared |

0.732837 |

Mean dependent var |

11150.52 |

|

|

Adjusted R-squared |

0.719805 |

S.D. dependent var |

7180.578 |

|

|

S.E. of regression |

3800.931 |

Akaike info criterion |

19.38963 |

|

|

Sum squared resid |

5.92E+08 |

Schwarz criterion |

19.51128 |

|

|

Log likelihood |

-423.5718 |

Hannan-Quinn criter. |

19.43474 |

|

|

Durbin-Watson stat |

0.721282 |

|||

Personal Consumption Expenditures for pleasure boats as a function of unemployment, interest rates, and oil price changes, 1980-2023.

Conclusion

I like Brunswick’s products, its management, basic financials, dominant product market positions, and technology.

What I don’t like at this time is its stock, as I think there’s great sensitivity to potential near-term adverse macroeconomic conditions that are largely outside the company’s control.

For those who expect no economic recession and no further inflation and unemployment headwinds — hold on to or buy the shares. Under such circumstances, there is a reasonable probability that EPS might double over the next three years.

But I remain a macroeconomic skeptic and from this brief review expect the share price to at best continue going sideways but probably lower. A neutral-to-moderately bearish stance based on my outlook thus seems appropriate.

Be the first to comment