US Dollar Fundamental Forecast: Bullish

- US Dollar remained on the offensive as prices whipsawed around the Fed

- 75-basis point hikes were downplayed, but balance sheet tightening is near

- All eyes are on US CPI data and a slew of Fedspeak amid jittery markets

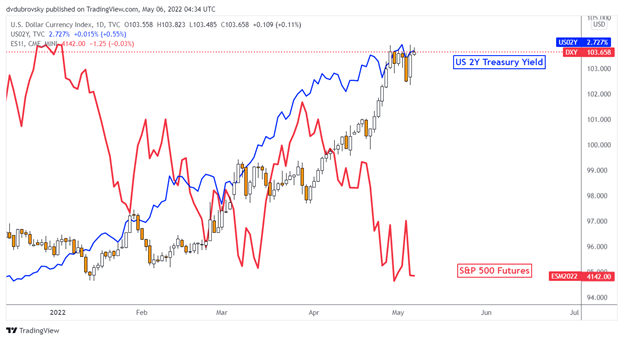

The US Dollar experienced volatile performance this past week, where all eyes were on the Federal Reserve. The central bank delivered, raising benchmark lending rates 50-basis points. The initial reaction was a dovish hike as Fed Chair Jerome Powell downplayed 75-basis point rate hike expectations that markets were pondering in the months ahead. As a result, the greenback turned lower.

As traders digested the information, sentiment reversed course and the US Dollar regained its footing. At the end of day, quantitative tightening is just around the corner. On the chart below is how this could look like. Starting at an initial pace of USD 47.5 billion per month in June, speeding up to 95b 3 months after, the size of the balance sheet would still be higher than the midpoint of the Covid boost by 2024.

How is the Balance Sheet Supposed to Look as 2024 Starts?

In the week ahead, the US Dollar will be watching the next US inflation report on May 11th. Headline inflation is expected to cool to 8.1% y/y in April from 8.5% prior. This is as core CPI is anticipated at 6.1% from 6.5% before. While this would represent some disinflation, it remains far above the central bank’s target. A stronger report could further propel the US Dollar and amplify risk aversion.

Interesting, looking at the Citi Economic Surprise Index, US data is still tending to beat economists’ expectations. However, the margin of rosy outcomes relative to estimates has been shrinking. There was a high of 70 in April before falling to 18 prior to the non-farm payrolls report. Values below 0 would represent increasingly softer outcomes relative to the consensus.

A slew of Fedspeak will also cross the wires. These include from Loretta Mester, Raphael Bostic and John Williams, presidents of the Cleveland, Atlanta and New York branches respectively. To some degree, they could instill confidence in the economy being able to withstand aggressive monetary tightening. This could offer near-term relief for sentiment, perhaps threatening the US Dollar.

However, all things considered, the greenback still remains in a position to continue capitalizing against its major peers. The central bank arguably remains the most hawkish amongst its G-10 counterparts. Meanwhile, the stagnant balance sheet remains an obstacle for sentiment to materially change course. It is thus a bullish call for the world’s reserve currency this coming week.

US Labor Market Data

— Written by Daniel Dubrovsky, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter

Be the first to comment