ferrantraite

High-momentum tech stocks are hard to come by these days. Higher interest rates and harsh selling in the growth-heavy sector continue to plague investors. One name, however, features a strong Momentum rating by Seeking Alpha along with impressive valuations and free cash flow. Is there more upside to come in Flex Ltd. (NASDAQ:FLEX) which not too long ago broke out technically? Let’s check it out.

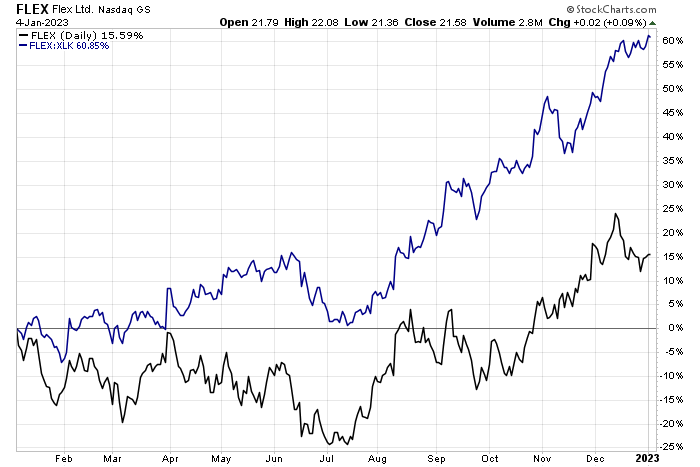

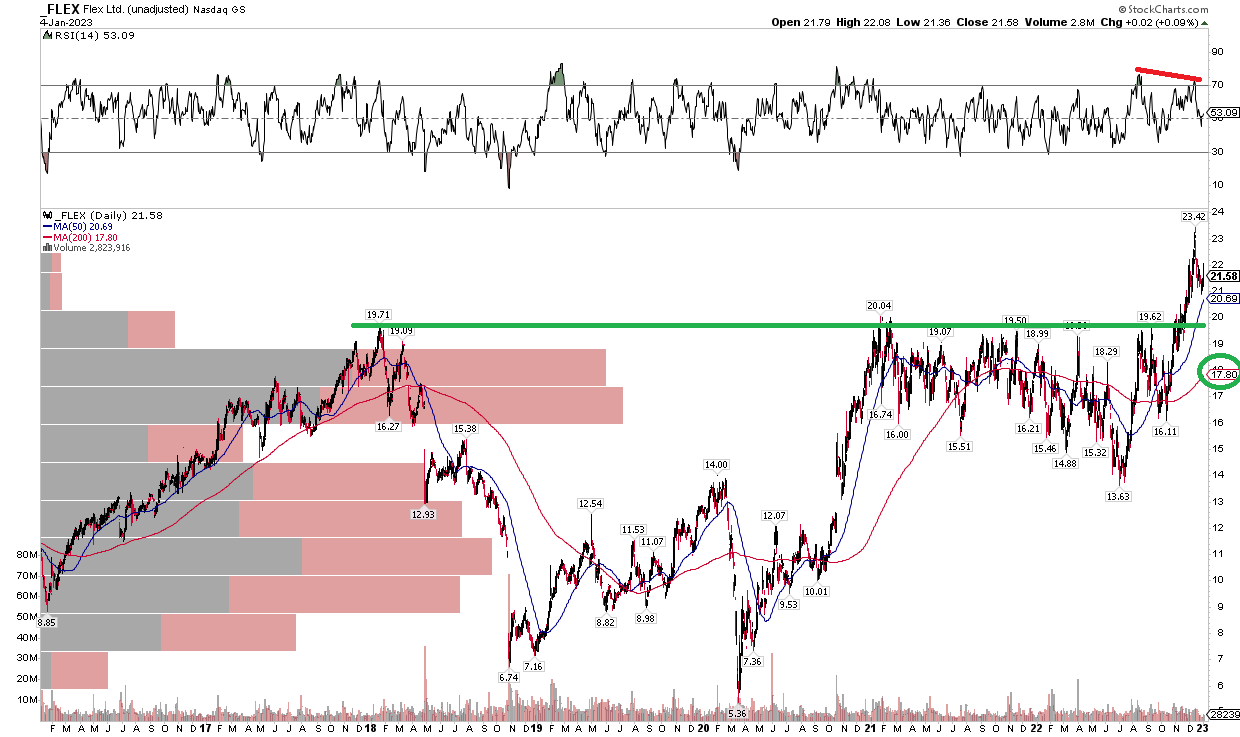

FLEXing Momentum

StockCharts.com

According to Bank of America Global Research, Flex is a global provider of vertically integrated supply chain services starting from PCB fabrication, design, engineering, and manufacturing services through after-sales support. The core business includes the Reliability Solutions and Agility Solutions segments.

The California-based $9.8 billion market cap Electronic Equipment Instruments & Components industry company within the Information Technology sector trades at a low 12.3 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal.

Flex reported a solid earnings and revenue beat back in October, and shares moved higher in the weeks following that report. The good news is perhaps a reason fund managers are overweight the stock, according to BofA. Finally, Credit Suisse is high on FLEX as of December 12.

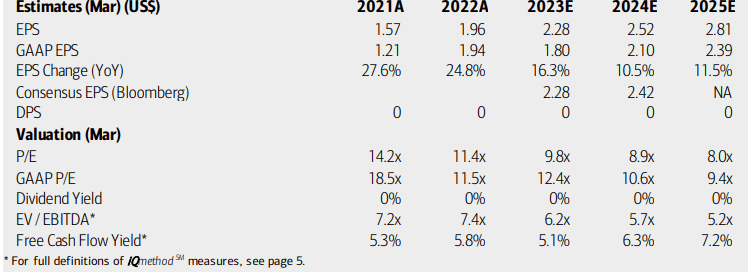

On valuation, analysts at BofA see earnings having risen sharply in 2022 after a strong 2021. Per-share profit growth is then seen as rising at a slower pace, but still robust, through 2025. The Bloomberg consensus forecast is not quite as sanguine as what BofA sees.

Even with solid free cash flow growth expected, no dividends are forecast to be paid on this high-growth tech name. What’s ideal, though, is that the forward PEG ratio is exceptionally low at just 0.57, according to Seeking Alpha. Overall, I agree with the A- valuation rating.

FLEX: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

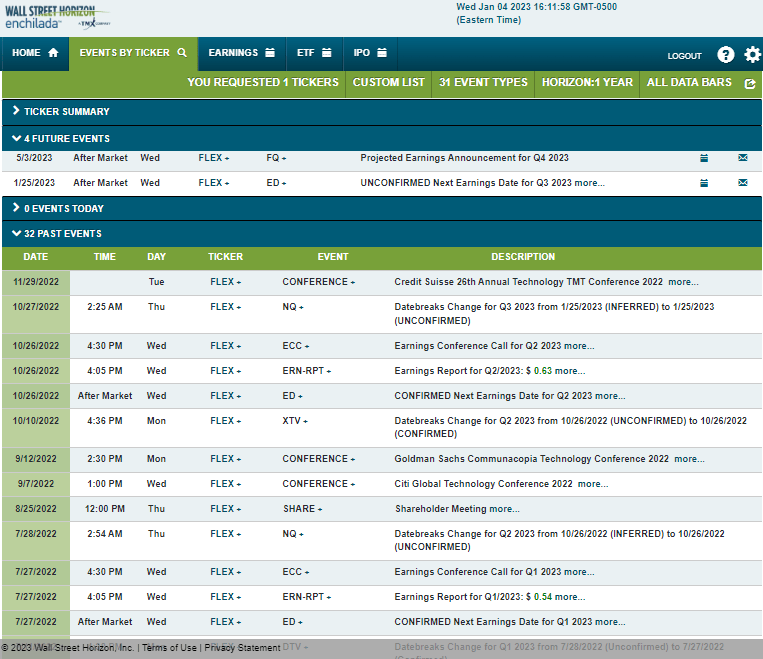

Looking ahead, corporate event data from Wall Street Horizon shows a confirmed Q3 2022 earnings date of Wednesday, January 25 AMC. The calendar is light on volatility catalysts aside from that reporting date.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

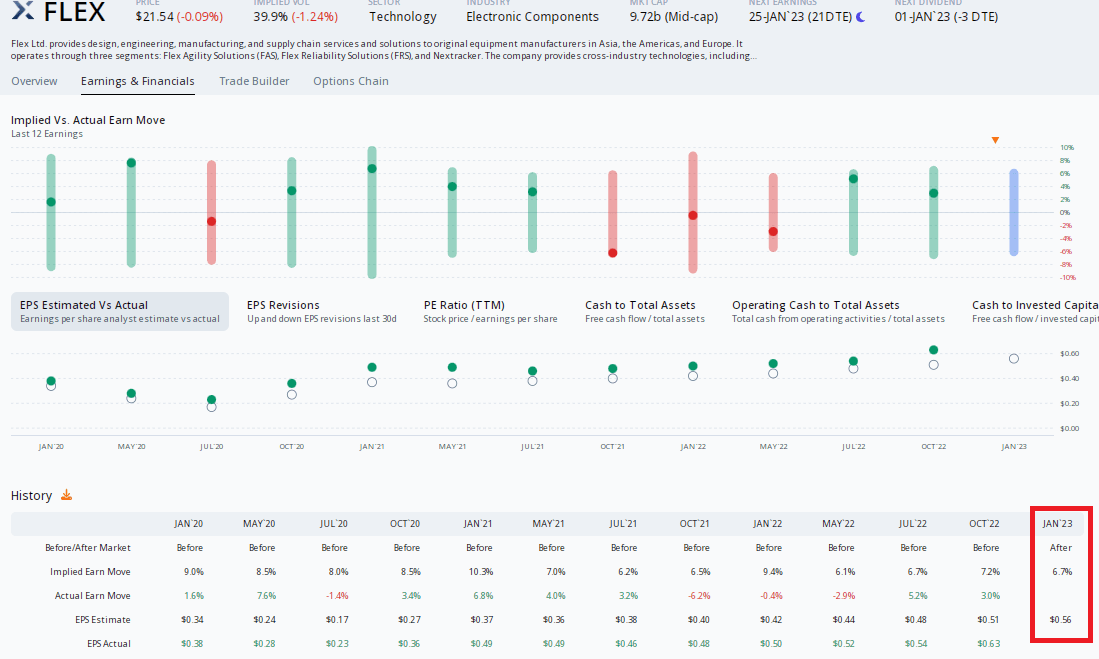

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $0.56 which would be a 12% increase from $0.50 earned in the same period a year ago. Remarkably, the company has topped analysts’ forecasts in each of the previous 12 quarters while shares have traded higher post-reporting in the last two instances.

Meanwhile, options traders expect a 6.6% earnings-related stock price swing when analyzing the at-the-money straddle that expires soonest after the Q3 report. We have not seen massive moves following recent quarterly earnings dates, so I would lean to be a seller of that premium.

FLEX: Earnings Growth Anticipated

ORATS

The Technical Take

As I was looking for in previous articles, FLEX indeed broke above the key $20 level. Technicians would say the bullish price objective based on the elongated cup and handle pattern would be to near $35. Right now, though, shares appear to be throwing back to test the prior resistance level. I would not be surprised to see the stock retreat a bit more down to near $20.

But long-term investors should like FLEX’s upward-sloping 200-day moving average while much of the rest of the tech space is moving down. Overall, a small retreat could be in the cards, but the breakout above $20 is quite bullish.

FLEX: Shares Retesting Support

StockCharts.com

The Bottom Line

I continue to like FLEX’s single-digit operating earnings multiple and its constructive chart. Moreover, a solid earnings beat rate history should be a tailwind going into earnings later this month.

Be the first to comment