FG Trade/E+ via Getty Images

Thesis

Fisker Inc. (NYSE:FSR) is entering the electric vehicle (EV) market with SUVs that combine cutting-edge technology at an accessible price, which presents the firm with a huge array of opportunities. In addition, FSR intends to acquire a leading position without major capital expenditures by entering into contract manufacturing arrangements with the largest and most reputable enterprises. The Ocean, FSR’s first SUV, will be produced by Magna (MGA), the automotive industry’s fourth-largest supplier with experience constructing 3.7mm cars. This not only decreases execution risk and time to market, but also increases early-cycle profitability. The business strategy and skateboard design of FSR should enable the company to introduce more models and acquire market share more quickly.

Why am I bullish on FSR?

Growing opportunity into a large TAM

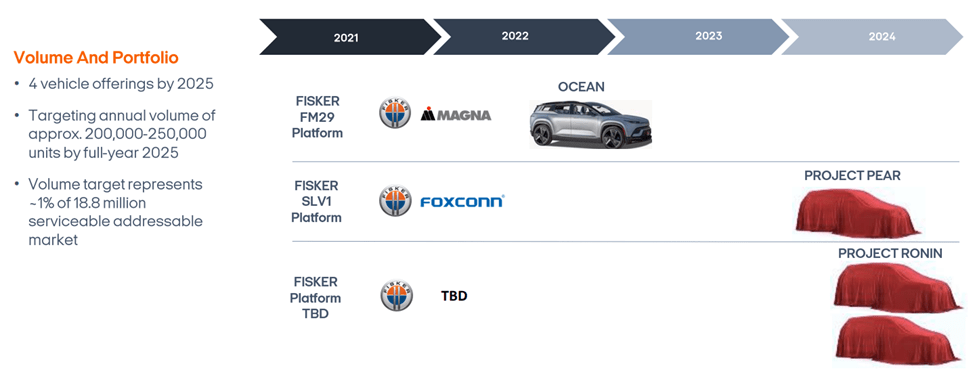

The company plans to bring a total of four vehicles to market by 2025, including the Ocean. Fisker’s second vehicle is the PEAR, which stands for personal electric automotive revolution. The PEAR targets the lower end of market where new EV OEM entrants have been less focused. I believe Fisker’s planned PEAR model could be a game changer in the lower end of the segment, with a starting price below $30k. Although details are still forthcoming, this model should incorporate a similarly winning profile of attractive design and more advanced technology, which buyers of EVs seek out and which ICE vehicles lack at a compelling price point. Management expects three derivatives of the PEAR to enable ~1mm unit sales annually in 2027. For context, the Toyota RAV4, one of the best-selling car models worldwide, sold ~1mm units in 2021. I recognize the PEAR’s high-volume potential but model more conservatively, looking for production to grow to ~214k units in 2027. While I expect production of the PEAR to eventually overtake Ocean, I still expect Ocean to contribute the majority of revenue, driven by its comparatively greater ASP. Fisker’s third planned model, Project Ronin, targets the ~ $100k price range, and will compete against the Lucid Air (LCID). Details on Fisker’s fourth model are limited, however, I suspect it may be a pickup truck.

Fisker Planned Portfolio (Company Presentation)

The SUV market in which Fisker Ocean competes is the largest segment in the passenger vehicle category. About half of the passenger vehicles sold in the US end the EU are SUVs. I believe these markets could comprise annual sales of ~10mm EV SUVs by 2030, and FSR could hold a 5% share of this segment. My forecast for FSR does not assume any new vehicle launches beyond the two already announced and no presence outside the US and the EU. These factors could provide additional upside.

Upside from pricing

I see the potential for price increases, given a robust pricing environment for EVs. Demand for top-selling trims has sold out, and there is a waitlist for the limited edition One trim. Fisker has committed to not raising MSRPs until after 40k units are sold. I see tangible future incremental revenue opportunities from monetizing OTA updates. The Ocean’s lower-priced trims contain a sub-set of full ADAS functionality despite having the same hardware as the most expensive versions. My model does not incorporate any upside from opportunities such as company-provided insurance, software enhancements, acceleration boost, entertainment subscriptions, and other connectivity-related features.

De-risked model

Fisker deliberately chose not to vertically integrate, in contrast to EV OEMs such as Tesla (TSLA). This set-up should minimize development costs and time to market, while also targeting a high-volume segment in which newer entrants cannot profitably compete, given heavy start-up costs. I like Fisker’s strategy of partnering with an experienced contract manufacturer for the Ocean SUV. Magna Steyr has produced more than 3.7mm vehicles over time for nine OEMs, which includes EVs for major OEMs. Magna has a vested interest in the success of the Ocean due to its ownership of warrants in FSR. Furthermore, Magna’s credibility as a sophisticated EV assembler is on the line. I believe this de-risked business model, strong manufacturing partnerships, and the company’s skateboard design should allow Fisker to launch more new models sooner than its competition and support market share gains.

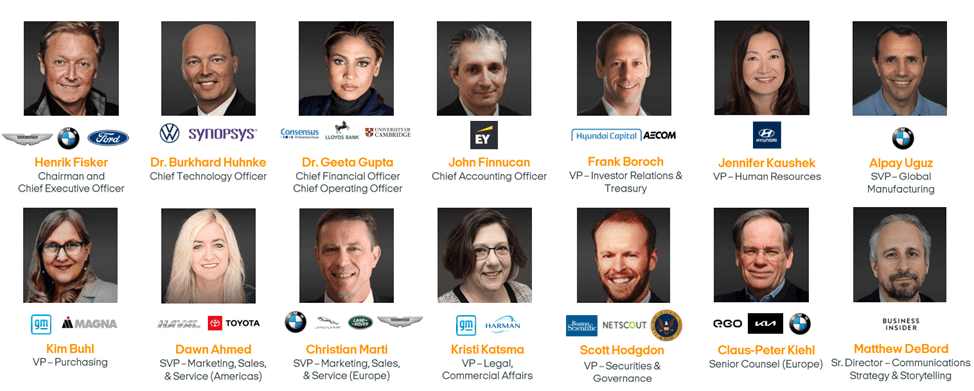

Seasoned management team

CEO Henrik Fisker is an accomplished designer and, has delivered on creating an affordable mid-sized SUV that combines both attractive styling and the latest in automotive technology. Mr. Fisker has previously worked at Ford Motor Company. Before that, Mr. Fisker was a designer at BMW, where he designed the Z7 and Z8 models. The other executive team members have rich experience with highly regarded companies that are leaders in their respective fields.

FISKER Executive Team (Company Presentation)

Valuation

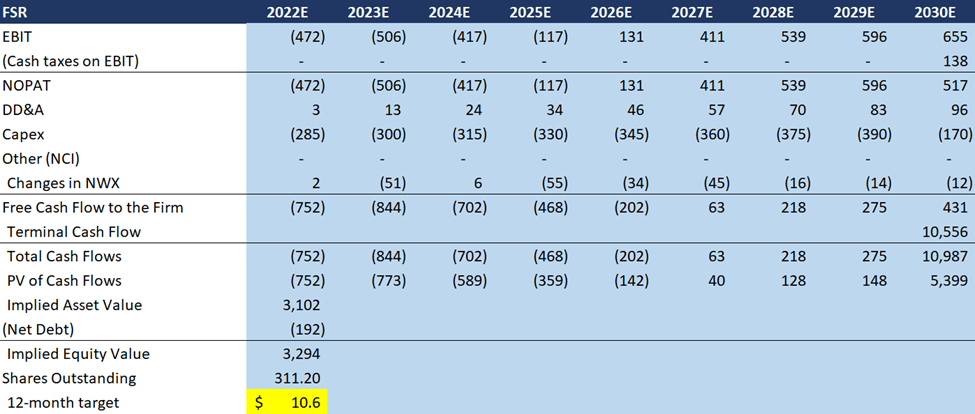

I have valued FSR shares using the long-term discounted cash flow. I have derived a cost of equity of ~12% based on a long-term risk-free interest rate of 2.5%, a risk premium of 5.5%, and a beta of 1.65. My valuation assumes 30/70 debt to equity in the long term, which implies a WACC of ~9%. Using the long-term forecast for cash flows and terminal growth of 5% in FY30, I derive a value of $10.6/share for FSR.

FSR forecasted P&L (my estimates)

Risks

The risks to my price target include:

-

Potential significant dilution from further capital raises.

-

Fate of the PEAR model for which there are very limited details publicly available.

-

Intensified competition from both incumbent OEMs and from new entrants who can replicate the contract manufacturing model.

Final Thoughts

FSR’s reliance on contract manufacturers lowers capital requirements, mitigates the risk of delays to production, and means that initial profitability may be higher than fully integrated OEMs. Production by Magna gives the company a foothold in the large EV market of Europe, into which newer entrants like Rivian (RIVN) have yet to expand. I recognize that some investors may take time to digest the benefits and tradeoffs of a contract manufacturing approach, particularly as securing access to battery supply has become top priority for EV makers. I believe the company’s outsourcing model with strong manufacturing partners and its skateboard design should allow Fisker to launch more new models sooner than its competition and lead to market share growth. Therefore, I keep a December 2023 price target of $10.6 on the company’s stock.

Be the first to comment