MartinPrescott/E+ via Getty Images

By Daniel Prince, CFA

Key Takeaways

- The market selloff this year has a silver lining: It may provide opportunities for a strategy known as “tax loss harvesting,” in which an investor can unlock potential tax benefits.

- Tax loss harvesting strategies can be used to realize losses in single stocks, bonds, funds, and ETFs in a taxable account. Investors can sell assets at a loss where realized losses can be used to offset realized capital gains as well as ordinary income.1

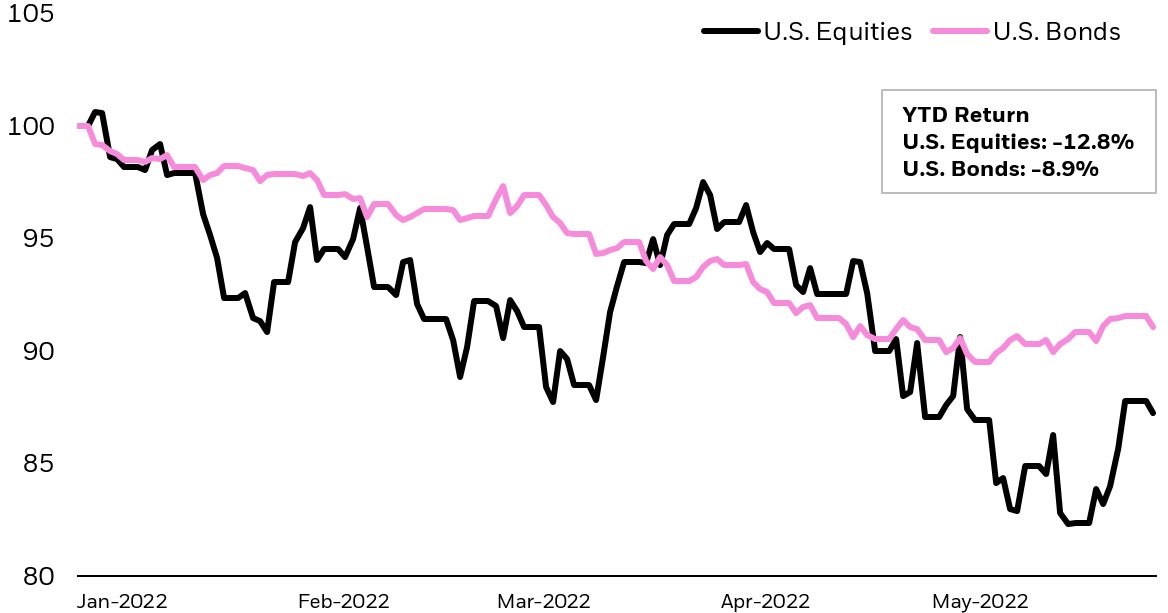

Markets have been roiled in 2022, as persistent inflation and rising rates have spooked investors. The pain has been widespread: U.S. stocks and bonds have both declined by more than 8% year-to-date.2 Since 1976, there have only been 10 months where both stocks and bonds have each posted losses greater than 2%.3

Growth of hypothetical $100: U.S. equities vs. U.S. bonds

Line chart showing the growth of hypothetical $100 invested in US equities vs. US Bonds from Jan. 1, 2022 to May 30th, 2022. US Equities, represented by the S&P 500 Index, lost 12.8% while US Bonds, represented by Bloomberg US Aggregate Index, lost 8.9%. (Morningstar Direct as of May 31, 2022. US Equites and US Bonds are represented by the S&P 500 Index and Bloomberg US Aggregate Index respectively. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.)

It can be difficult to hold on to investments while markets whipsaw and to learn the bitter truth that markets don’t always deliver outsized, orderly returns. But as the old saying goes, “what seems like a curse may be a blessing.” Investors can keep their long-term goals in sight, while taking steps to mitigate some of the pain of seeing their investments decline.

Tax Loss Harvesting With ETFs

Tax-loss harvesting is the act of selling an investment below its purchase price to realize a loss in a taxable account. Investors may use sales proceeds to purchase a comparable investment to maintain a similar exposure. Harvested losses can be used, dollar for dollar, to offset realized capital gains. In addition, investors can offset up to $3,000 per year of regular income with realized losses. If an investor recognizes more losses than gains, or has already offset the $3,000 income cap, losses can be carried forward indefinitely.

Rules preclude investors from recognizing losses and then quickly buying back their original investment. These “wash sale” restrictions mandate that an investor cannot realize a loss on the sale of an investment and then buy a “substantially identical” security, beginning 30 days before and ending 30 days after a security sale.4 Depending on the specific securities involved, executing a tax loss harvesting strategy and reinvesting to maintain a similar exposure can be accomplished with ETFs.

Illustration showing an equation and a hypothetical way to tax loss harvest. The three components of the first side of the equation are: 1) Sell investments that have declined in value, 2) realized losses offset gains on income tax returns, and, 3) buy an ETF with similar exposure; consider iShares ETFs. The sum of these three parts provide a tax benefit and help you stay invested. (For illustrative purposes only)

Opportunities Abound

Over 70% of stocks of in the U.S. stock market have fallen in price year-to-date, while U.S. bonds recently saw their largest drawdown since 1980.5 Selling single U.S. stocks at a loss and buying an ETF that seeks to track a U.S. broad based index may avoid violating wash sale rules while helping to stay invested. To be sure, tax loss harvesting opportunities are plentiful; many formerly high-flying stocks have fallen considerably, some of them as much as 50% year-to-date. Similarly, investors can consider selling out of individual bonds and buying diversified fixed income ETFs as a way to bank losses.

Tax loss harvesting can also apply to funds. Selling out of a mutual fund/ ETF at a loss and buying a different fund with a similar objective can help position your portfolio for future growth while attempting to reduce your total tax bill. Alternatively, investors may want to consider shifting some holdings to an ETF with a different objective. In both scenarios, tax benefits may be unlocked with the aim of staying invested.

Conclusion

In addition to sticking to your overall investment plan, maintaining good portfolio hygiene can include striving to achieve more favorable after-tax results. While current market volatility may get your portfolio down, consider tax-loss harvesting to get your tax offsets up.

© 2022 BlackRock, Inc. All rights reserved.

1 Source: IRS Topic No. 409 Capital Gains and Losses, as of 12/31/2021. Harvested losses can be used, dollar for dollar, to offset realized capital gains, thereby eliminating tax liabilities. In addition, investors can offset up to $3,000 per year of regular income with realized losses. If an investor recognizes more losses than gains, or has already offset the $3,000 income cap, current rules allow for losses to be carried forward indefinitely.

2 Source: Morningstar Direct, as of May 31st, 2022. The S&P 500 Index (stocks) and Bloomberg US Aggregate Index (bonds) fell 14.4% and 8.5%, respectively from Jan. 1, 2022, to May 26, 2022. Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

3 Source: Morningstar Direct, as of May 31st, 2022. US Equities and US Bonds are represented by the S&P 500 Index and Bloomberg US Aggregate Index respectively.

4 The Internal Revenue Service has not released a definitive opinion regarding the definition of “substantially identical” securities and its application to the wash sale rule and ETFs. The information and examples provided are not intended to be a complete analysis of every material fact respecting tax strategy and are presented for educational and illustrative purposes only. Tax consequences will vary by individual taxpayer and individuals must carefully evaluate their tax position before engaging in any tax strategy. The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective. The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

5 Source: Morningstar Direct, as of May 30th, 2022. U.S stock market refers to the S&P 500. U.S. bonds refers to the Bloomberg U.S. Aggregate Bond Index. The Bloomberg U.S. Aggregate Bond lost 12.74% from August 1, 1979, to Feb. 29, 1980, and 11.08% from August 2020 to April 30, 2022.

Carefully consider the Funds’ investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds’ prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/ developing markets or in concentrations of single countries.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

Diversification and asset allocation may not protect against market risk or loss of principal.

This material contains general information only and does not take into account an individual’s financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial professional before making an investment decision.

No proprietary technology or asset allocation model is a guarantee against loss of principal. There can be no assurance that an investment strategy based on the tools will be successful.

The information provided is not intended to be tax advice. Investors should be urged to consult their tax professionals or financial professionals for more information regarding their specific tax situations.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Bloomberg, BlackRock Index Services, LLC, Cohen & Steers, European Public Real Estate Association (“EPRA®”), FTSE International Limited (“FTSE”), ICE Data Indices, LLC, NSE Indices Ltd, JPMorgan, JPX Group, London Stock Exchange Group (“LSEG”), MSCI Inc., Markit Indices Limited, Morningstar, Inc., Nasdaq, Inc., National Association of Real Estate Investment Trusts (“NAREIT”), Nikkei, Inc., Russell or S&P Dow Jones Indices LLC or STOXX Ltd. None of these companies make any representation regarding the advisability of investing in the Funds. With the exception of BlackRock Index Services, LLC, which is an affiliate, BlackRock Investments, LLC is not affiliated with the companies listed above.

Neither FTSE, LSEG, nor NAREIT makes any warranty regarding the FTSE Nareit Equity REITS Index, FTSE Nareit All Residential Capped Index or FTSE Nareit All Mortgage Capped Index. Neither FTSE, EPRA, LSEG, nor NAREIT makes any warranty regarding the FTSE EPRA Nareit Developed ex-U.S. Index or FTSE EPRA Nareit Global REITs Index. “FTSE®” is a trademark of London Stock Exchange Group companies and is used by FTSE under license.

© 2022 BlackRock, Inc. All rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, BUILD ON BLACKROCK, ALADDIN, iSHARES, iBONDS, FACTORSELECT, iTHINKING, iSHARES CONNECT, FUND FRENZY, LIFEPATH, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, BUILT FOR THESE TIMES, the iShares Core Graphic, CoRI and the CoRI logo are trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

iCRMH0622U/S-2249676

This post originally appeared on the iShares Market Insights.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment