Douglas Rissing/iStock via Getty Images

By Seema Shah, Chief Global Strategist

The first month of summer came in hotter than expected. Data released in June showed that annual headline CPI inflation – previously thought to be cooling – had touched a new 40-year high. In response, the United States Federal Reserve (Fed) raised its benchmark interest rate by 75 basis points (bps) – 25 bps more than initially forecast and the largest increase since 1994. Eyeing the rest of 2022, further substantial rate hikes are possible as the Fed remains focused on stabilizing prices; however, in the process, a recession may become unavoidable. With broad equities and fixed income both facing difficult months and quarters ahead, investors need to actively seek out the opportunities that can still perform well in this tough investment environment.

Inflation sticking around longer than expected

It had been widely assumed that inflation had peaked in March. Later, in early May, Fed Chair Powell’s assertions that a 0.75% increase to the federal funds rate would not be a serious consideration at the next meeting of the Federal Open Market Committee (FOMC) led many investors to assume the Fed policy rates would follow only a modest tightening path. Some optimists even went so far as to predict a Fed policy pause in September.

Then the data came out. Rather than slowing in May, the consumer price index showed that annual headline inflation rose from 8.3% to 8.6%, the highest level since 1981.

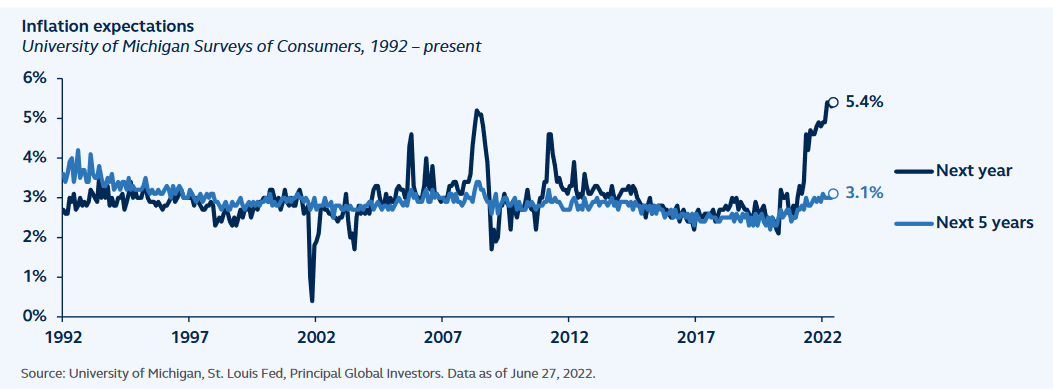

Perhaps more significantly, the flash reading of the University of Michigan Index of Consumer Sentiment, released right before the FOMC meeting, showed inflation expectations for the next 5-10 years rose from 3.0% in May to 3.3% in June, as consumers faced higher prices for gas and groceries.1 These two upside inflation surprises were enough to convince the Fed to break its recent forward guidance, demonstrate its data dependence, and introduce the first 75 bps increase since 1994.

1The flash reading of the University of Michigan indicator was on June 10. The official release, on June 24, and after the FOMC meeting, was revised down to 3.1%.

Inflation Expectations – University Of Michigan Surveys Of Consumers (Author)

More tightening may be coming

The inflation challenge facing the Fed today is more nuanced than what it was just 12 months ago. Driven by surging energy and food inflation, and lingering COVID supply chain-driven disruptions, both inflation expectations and wage pressures are rising. Without swift and decisive actions from the Fed (such as 75 bps rate hikes…), the situation could move beyond their control. Therefore, with Chair Powell emphasizing their “unconditional” commitment to price stability just a week after the June FOMC at the House Financial Services Committee, investors should prepare for significantly more tightening.

With the June move, the federal funds rate now stands between 1.5% and 1.75%. The median entry on the FOMC dot plot – used to chart committee members’ data forecasts – sees rates ending the year at 3.4%. This represents a 250 bps upward revision from the FOMC’s March forecast of 1.9% and brings policy rates sharply into restrictive territory. For the rest of 2022, investors should expect that the federal funds rate will likely rise an additional 175 bps to reach 3.5% by year-end. This accelerated tightening may imply fewer hikes are required next year, so the federal funds rate may rise only a further 75 bps in 2023, potentially peaking at 4.25%. Later in 2023, as economic data slows meaningfully, it is reasonable to think that rate cuts could once again be on the table.

FOMC Dot Projections (Author)

Immaculate disinflation may be wishful thinking

The Fed’s Summary of Economic Projections in March had forecast that the unemployment rate would remain broadly unchanged at 3.6% through to 2024. The new Summary of Economic Projections introduced an important upward revision to this forecast. They now see the unemployment rate rising gradually from 3.6% to 4.1% by the end of 2024.

In other words, the Fed is projecting a 0.5% rise in the unemployment rate over the next two years. This marks a shift from what it has called “immaculate disinflation,” a scenario in which inflation could meaningfully come down without an accompanying rise in unemployment.

Why is the pickup in unemployment relevant? According to the Sahm Rule, created by former Fed economist Claudia Sahm, a recession occurs when unemployment climbs by at least 0.5% in a short time frame. So, while the Fed hasn’t outright stated that it expects a recession in the near term, their own numbers tell a different story.

If – and when – a recession could start

Despite Chair Powell’s continued assertions that a soft landing is possible, the odds that the Fed will be able to tighten policy rates without the U.S. economy entering into a recession are not in the Fed’s favor. During the last 11 tightening cycles, the Fed has only skirted recession three times (1965, 1984 and 1994). But in each of those cycles, inflation was lower and the federal funds rate was meaningfully higher to begin with, so the Fed’s tightening measures did not have to be as dramatic as they do to achieve their goals today.

Despite sharp monetary tightening over the next 12 months, inflation will likely decline very slowly, to only around 6.5% by the end of 2022 and then to 3% by end of 2023. The consequences of the Fed’s aggressive hiking impact on the U.S. economy may be more significant, precipitating recession – likely by mid-2023 – if not sooner.

Where investors can turn

In this challenging climate, it is crucial for investors to focus on stability and high quality, particularly in the following asset classes:

- U.S.mid-cap stocks: U.S. mid-caps are more attractive than either large- or small-caps. Not only are large-cap valuations markedly more expensive, but their exposure to the relatively weaker global economy also suggests continued underperformance. By contrast, although small-cap valuations are as equally attractive as mid-cap, they will likely struggle amid rising interest rates and may continue to be challenged by the limited pricing power in this inflationary environment.

- Securitized debt: Fixed-income positioning should be more defensive and tilted toward higher quality – greater exposure to U.S. Treasurys is warranted. As the U.S. economy moves towards recession next year, the Fed will likely shift from rate hikes to rate cuts, putting downward pressure on U.S. Treasury yields. High yield will likely be challenged as recession concerns grow and remains particularly vulnerable to an oncoming drop in liquidity as the Fed reduces its balance sheet. In contrast, securitized debt products tend to provide better stability during periods of high volatility and risk, without exposure to corporate credit.

- Infrastructure: Alternatives are poised to outperform amid the pressures on stocks and bonds. Infrastructure investments offer an opportunity for diversification, inflation mitigation, and exposure to the structural decarbonization trend. They also potentially provide attractive real yield and predictable cash flows.

- Commodities: As structural supply shortages continue, commodities are another alternative asset class poised to extend positive performance.

The possibility for near-term volatility may be daunting. But the key is to remain positioned, so investors are poised for potential gains when the recovery starts.

The ongoing war in Ukraine has driven up the costs of energy, food, and other key commodities, while recent factory closures in China – part of that country’s strict response to a fresh COVID-19 outbreak – have exacerbated supply pressures that might otherwise have eased by this point in the pandemic.

Although Powell advised that markets should not expect 75 bps hikes to be “common,” as they represent an “unusually large” move, he also signaled that the July FOMC meeting could see a 50 or 75 bps hike if inflation expectations continue to drift higher.

_______________

Risk considerations

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results. Fixed-income investments are subject to interest rate risk; as interest rates rise their value will decline. Asset allocation and diversification do not ensure a profit or protect against a loss.

Investing in derivatives entails specific risks regarding liquidity, leverage and credit that may reduce returns and/or increase volatility.

Important Information

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. The opinions and predictions expressed are subject to change without prior notice. The information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity. Any reference to a specific investment or security does not constitute a recommendation to buy, sell,or hold such investment or security, nor an indication that the investment manager or its affiliates has recommended a specific security for any client account. Subject to any contrary provisions of applicable law, the investment manager and its affiliates, and their officers, directors, employees, agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in the information or data provided.

This material may contain ‘forward-looking’ information that is not purely historical in nature and may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This material is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use wouldbe contrary to local law or regulation.

© 2022 Principal Financial Services, Inc. Principal®, Principal Financial Group®, and Principal and the logomark design are registered trademarksof Principal Financial Services, Inc., a Principal Financial Group company, in the United States and are trademarks and services marks of PrincipalFinancial Services, Inc., in various countries around the world. Principal Global Investors leads global asset management at Principal®.

Principal Global Asset Allocation is an investment management team within Principal Global Investors.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment