RiverNorthPhotography

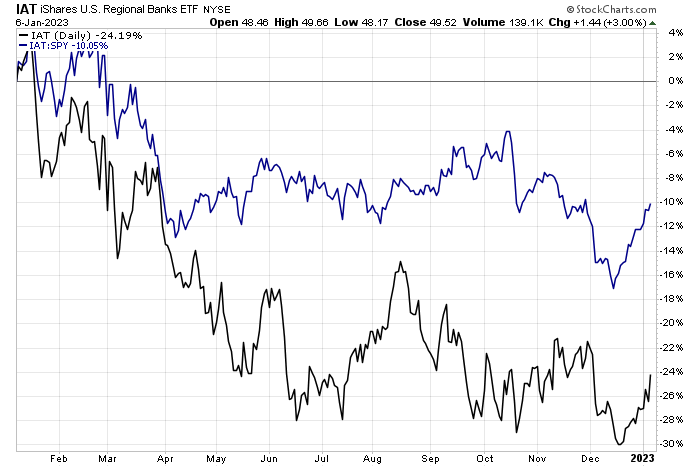

Regional banks have had their fits and starts lately. The group that is both economically sensitive and somewhat defensive in its value niche has rallied hard on both an absolute and relative basis in the last few weeks after enduring a drubbing from mid-October through mid-December (relative to SPY).

So, is the group set up to be a 2023 market leader? Hard to say, but let’s start with one well-known regional with earnings due out soon.

Regional Banks Rising (Relative) Again

Stockcharts.com

According to Bank of America Global Research, Fifth Third (NASDAQ:FITB) is a large-cap regional bank with over $200 billion in assets that operates primarily in the Midwest and Southeast. The company’s lending portfolio focuses primarily on C&I, residential real estate, and auto loans. It engages in the provision of banking & financial services, retail & commercial banking, consumer lending services, and investment advisory services through its subsidiary Fifth Third Bank. It operates through the following segments: Commercial Banking, Branch Banking, Consumer Lending, and Wealth and Asset Management.

The Ohio-based $23.7 billion market cap Banks industry company within the Financials sector trades at a low 10.6 trailing 12-month GAAP price-to-earnings ratio and pays a high 3.8% dividend yield, according to The Wall Street Journal. A key risk for the bank is what happens with the domestic macro economy – slowing loan origination and higher loan loss reserves could be a risk.

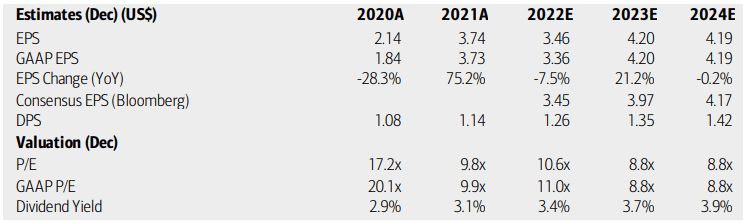

On valuation, analysts at BofA see earnings having fallen by more than 7% in 2022 after robust growth in 2021. Per-share profits are expected to recover significantly in 2023 before stabilizing near $4.20. The Bloomberg consensus forecast is slightly less than what BofA sees, though. Dividends, meanwhile, are expected to rise despite some EPS volatility.

Both FITB’s operating and GAAP P/Es should remain attractive over the coming quarters considering the profit recovery. The stock features a solid B valuation rating from Seeking Alpha, but its price-to-book ratio, a key gauge of banks, is significantly above both its 5-year average and the sector median, so that’s a concern. Overall, solid earnings growth and a growing dividend are positive features that outweigh a slightly elevated P/B.

Fifth Third Bancorp: Earnings, Valuation, Dividend Forecasts

BofA Global Research

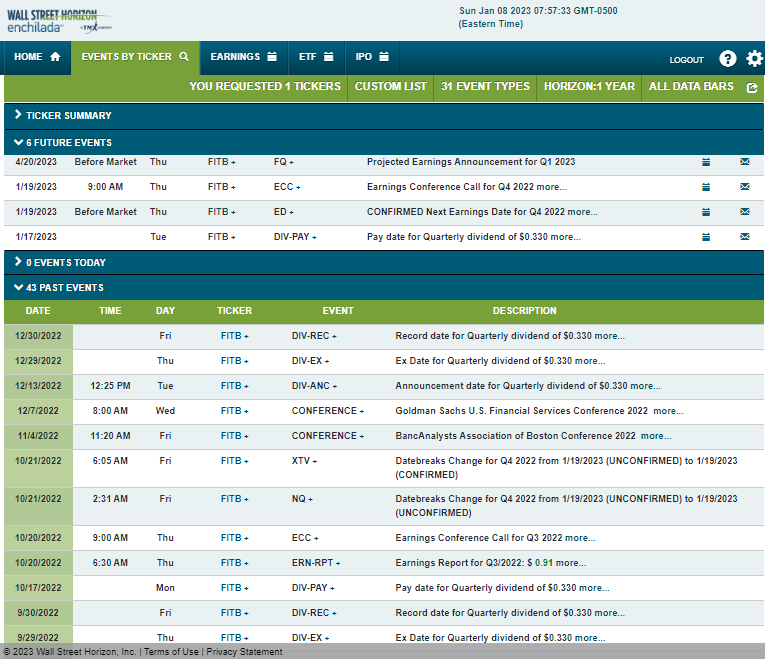

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Thursday, January 19 BMO with a conference call later that morning. You can listen live here. The event calendar is light aside from a quarterly dividend pay date the Tuesday before earnings.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

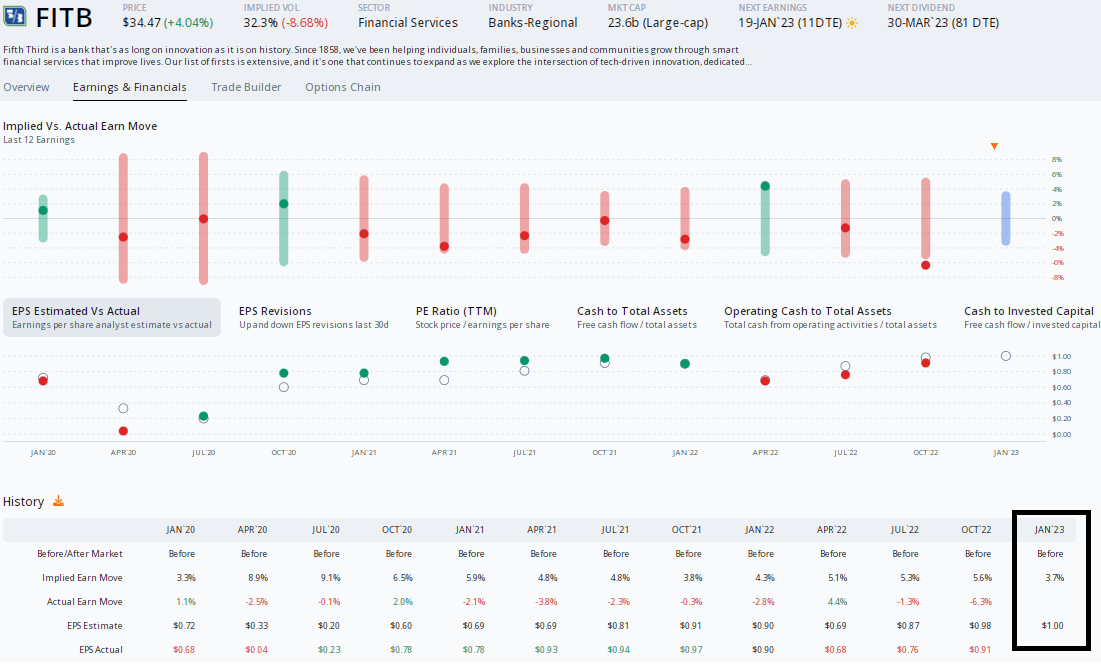

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $1.00 which would be an 11% increase from $0.90 of per-share profits earned in the same period a year ago. Unfortunately for the bulls, FITB has missed bottom-line numbers in each of the three previous reports and the stock has traded lower-post earnings in 7 of the last 8 reports.

This time around, options traders have priced in a small 3.7% earnings-related stock price swing using the at-the-money straddle expiring soonest after the January 19 date. With implied volatility near 32%, those are somewhat cheap options considering some recent moves around earnings. I would err on the side of being long that premium.

FITB: A String of EPS Misses, Cheap Options

ORATS

The Technical Take

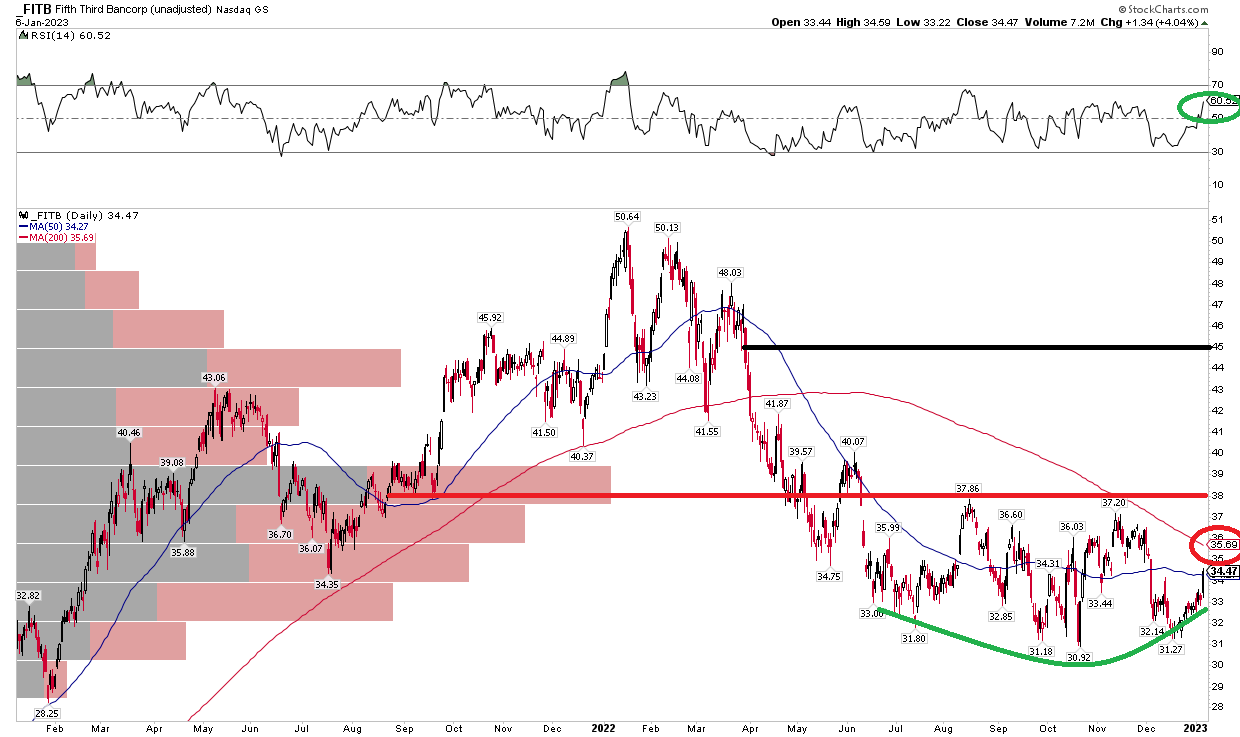

FITB appears to be in the initial stages of putting in a bullish rounded bottom when looking back over the last several months. I noted key support just above the $30 level back in October, and that played out so far. I see resistance, though in the $37 to $38 range. Should shares rise above that zone, a bullish measured move price target of $45 would be in play.

Also, notice in the chart below that the RSI at the top of the chart is creeping higher, which I like to see. The bullish zone is 40 to 90 while the 20 to 60 range is considered bearish. Still concerning is a falling 200-day moving average, but a thrust last week helped take FITB above its 50-day moving average. Overall, I think there are improving signs on the chart.

FITB: Bullish Rounded Bottom Forming?

Stockcharts.com

The Bottom Line

I continue to generally like the valuation on FITB and the chart is doing the right things to establish a floor. The Q4 earnings date could be tough based on history, but I see more longer-term upside potential than downside risks.

Be the first to comment