Khanchit Khirisutchalual

Fair Isaac Corporation otherwise known as (NYSE:FICO) is a leading financial software company that was founded back in 1956. The business was known for pioneering its credit scoring model the “FICO score” which has become an industry standard across organisations to assess credit risk. FICO has a strong blue chip customer base which includes 95% of the largest financial institutions in the US. Even more amazingly its not just about the quality of its customers but also its high dollar based retention rate which was 110% in the most recent quarter. This means its customers are finding its products “sticky” and continue to spend more through account expansion. In Q1,FY23, FICO released strong financial results as it beat both top and bottom line growth estimates. In this post, I’m going to break down its financials, and valuation, let’s dive in.

Note: In January I covered FICO’s business model in detail, so you can check that out here, if you want to learn more. This time arounds I will just be discussing its financials in this post.

Fourth Quarter Financials

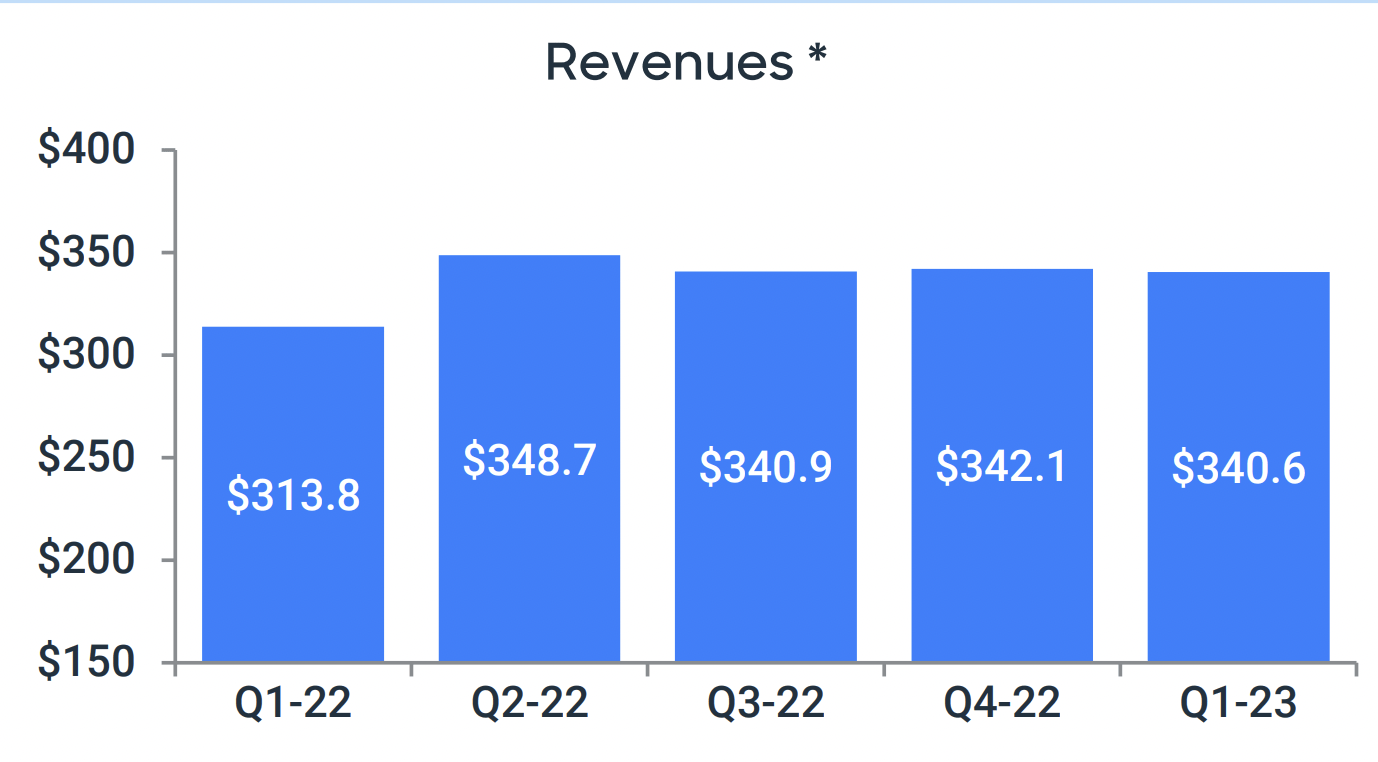

FICO reported strong financial results for the first quarter of fiscal year 2023. Revenue was $344.9 million, which increased by 6.97% year over year and beat analyst expectations by ~$432,000. It should be noted that the chart below shows the revenue adjusted for the divesture of Siron, its financial crime solution (I will discuss more on this later). Even with the divestiture we can see its revenue still increased from $313.8 million to $340.6 million, or 8.54% year over year.

Revenue (Q1,FY23)

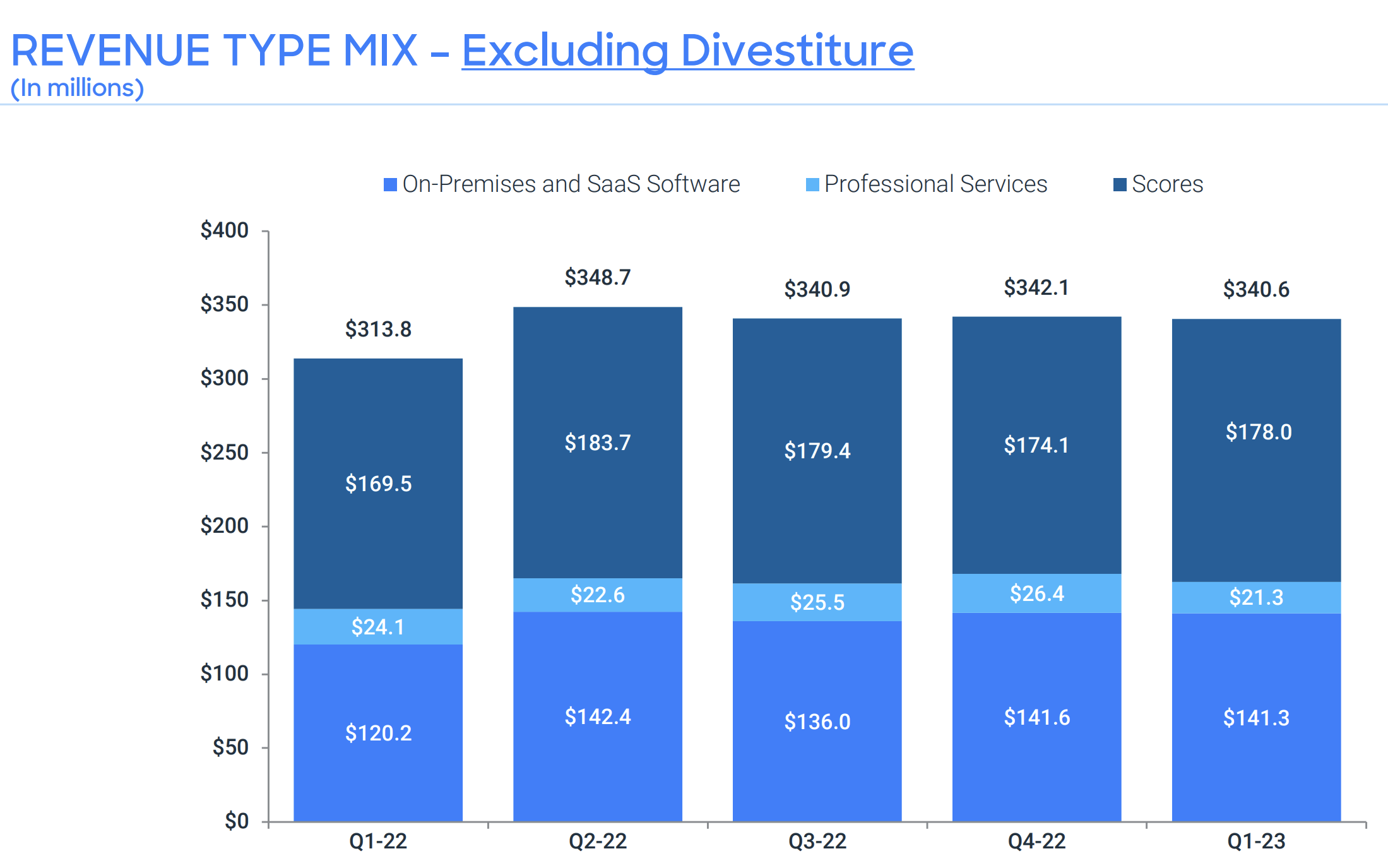

Breaking revenue down by segment, FICO reported software and professional revenue of $166.9 million, which increased by 9% year over year. On an divestiture adjusted basis, On premises and SaaS software increased by a rapid 16.7% to $141.3 million. Its legacy “Scores” business reported $178 million in Q1,FY23, which increased by a steady 5% year over year. This was driven by 11% B2B revenue growth, which was bolstered by solid personal loan and credit card origination volumes, which increased by 19% year over year. In addition, to strong auto loan originations which rose by a substantial 24% year over year. It was great to see this segment wasn’t massively impacted by the “recessionary” environment. However, It should be noted that mortgage origination volumes did decline by an eye watering 42% YoY, but this was expected due to the rising interest rate environment which has impacted the affordability of housing. It is estimated that three quarters of all home loan originations are based upon a FICO score, thus this is testament to the company’s ubiquity in the industry. B2C revenue also declined by 6% as expected to the high inflation and “recessionary” environment, which has squeezed the consumer.

Overall I don’t deem these declines to be a major issue long term as the economy tends to be cyclical by nature. Thus I forecast mortgage originations to bounce back in the future as interest rates are expected to be scaled down post 2023. This is not definite but we are already seeing inflation on a downward trend with 6.1% reported on the CPI, down from a 9.1% high in June 2022. As the Fed originally raised rates to curb inflation, it only seems logical that rates would eventually fall. However, I don’t believe we will see a 0%-1% interest rate environment as in previous years.

A 11.6% decline in professional services revenue from $24.1 million to $21.3 million was also expected in my eyes, as business customers pullback the need for custom integrations. Professional Services contributed 6.2% of revenue in Q1FY23, down from 7.6% of revenue in Q1,FY22. Overall I believe this is a positive as professional services is resource intensive and thus lower margin and less scalable, than the software segment. Professional Services work also tends to involve “one off” projects which isn’t great for revenue consistency. I believe some professional services work is necessary in complex segments of the financial industry to help with custom integrations of software products etc, but caution must be taken as being a “consultancy” is a very different business model.

Revenue by type (Q1,FY23 report)

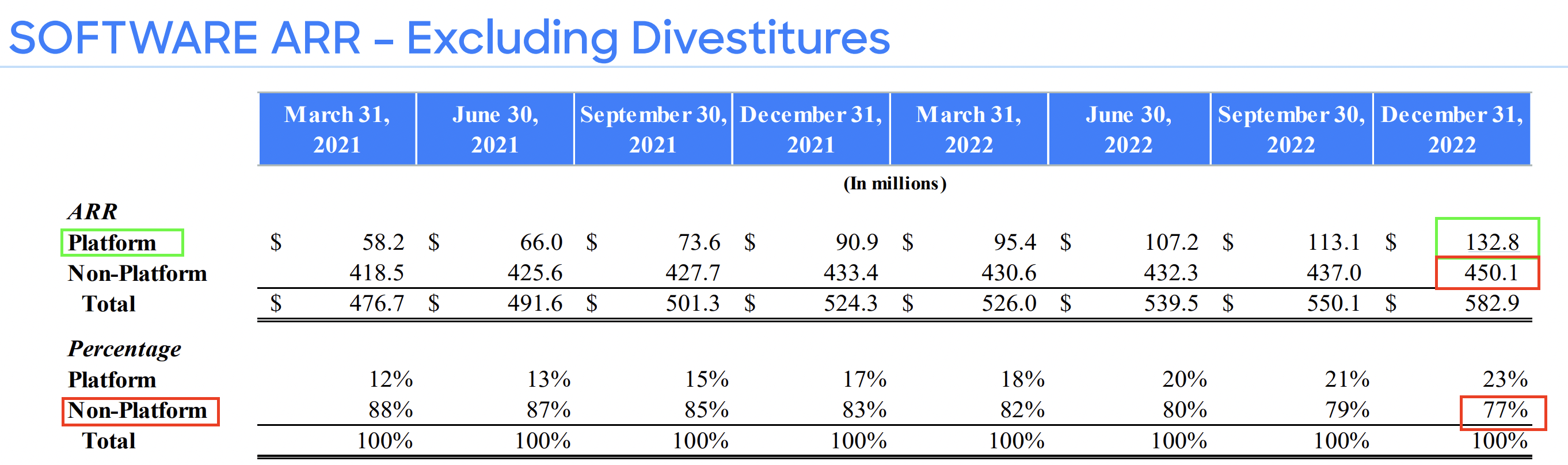

Another metric to track the potential margin and scalability growth for FICO in the future is to calculate the percentage of “Platform” customers which I believe refers to its cloud native solution. In this case, the company has steadily grown its Platform Annual Recurring Revenue [ARR] by a rapid 46% year over year from $90.9 million in Q4,21 to $132.8 million by Q4,22 (calendar year). This is a positive sign but even more important is the percentage of total ARR. In this case, Platform ARR contributed to just 12% of the total in Q1,21, this rose to 17% of the total in Q4,21 and 23% by Q4,22. This increasing trend is a positive sign as its “platform” solution is likely the highest margin deployment which also offers a greater user experience, due to more seamless updates.

FICO also reports its “Non Platform” revenue, which they define as those with “custom integrations” or modifications and I believe is the “on premises” solution. This revenue type is for its legacy customers and contributed to a massive 77% of total ARR in Q4,22. The positive is this has declined as a portion of the total from 82% in Q4,21, as the “platform” SaaS solution has scaled. The company still has a long way to go reducing its number of “non platform” customers but the trend is in the right direction. Apart from the aforementioned software side of the company, FICO should also be able to reduce its split support function, which will then free up resources to focus purely on cloud native software growth.

Software ARR (Q1,FY23 with author Annotations)

Super Retention Rates

One of the great things about FICO’s software product is its super high dollar based net retention rate. For context anything over 100% is great, as it means customers and sticking with the platform. In this case we can see FICO’s platform solution reported a staggering 130% retention rate, which was up 1% over the prior quarter and means customers are staying with the solution and spending more through upsells. It should be noted this retention rate is down from the 146% rate in Q4,21 and Q4,21, but I believe this is mainly driven by slightly lower contract expansion through cross selling given the macroeconomic environment. Either way its retention rate is still strong. Its Non Platform business is much more mature and thus “only” reported a 103% retention rate, but this may be impacted by the aforementioned cloud migrations, which is a positive sign overall.

Retention Rates (Q1,FY23)

Streamlining through Divestitures

FICO has made approximately 12 acquisitions over the past few years from Hnc Software for $810 million in 2002 to Braun Consulting for $30 million in 2004, and Adeptra for $115 million in 2021, which integrated with FICO’s Falcon Fraud Manager. However, now the company is aiming to streamline its business. In 2021, the company sold its collection & recovery business to Constellation software and more recently (Q4,22) FICO divested its Siron Compliance solution to IMTF a former partner, who is also buying Fair Isaac Germany GmbH. I believe this was a positive move overall as FICO’s platform growth rate is “substantially higher” than the Siron business the company sold off, according to management insights on its earnings call. In addition, the sale of its Germany based division is also a positive sign in my eyes. This is because Germany is a very tough market to grow financial credit products in, with a very slow moving and heavy regulatory process. Previously I have attended financial conferences and many FICO competitors explained to me how tough the market is. Thus I believe FICO Germany was a slow growing part of the company also, thus it makes sense to divest this business and focus on its higher growth segments.

Margins, Expenses and Balance Sheet

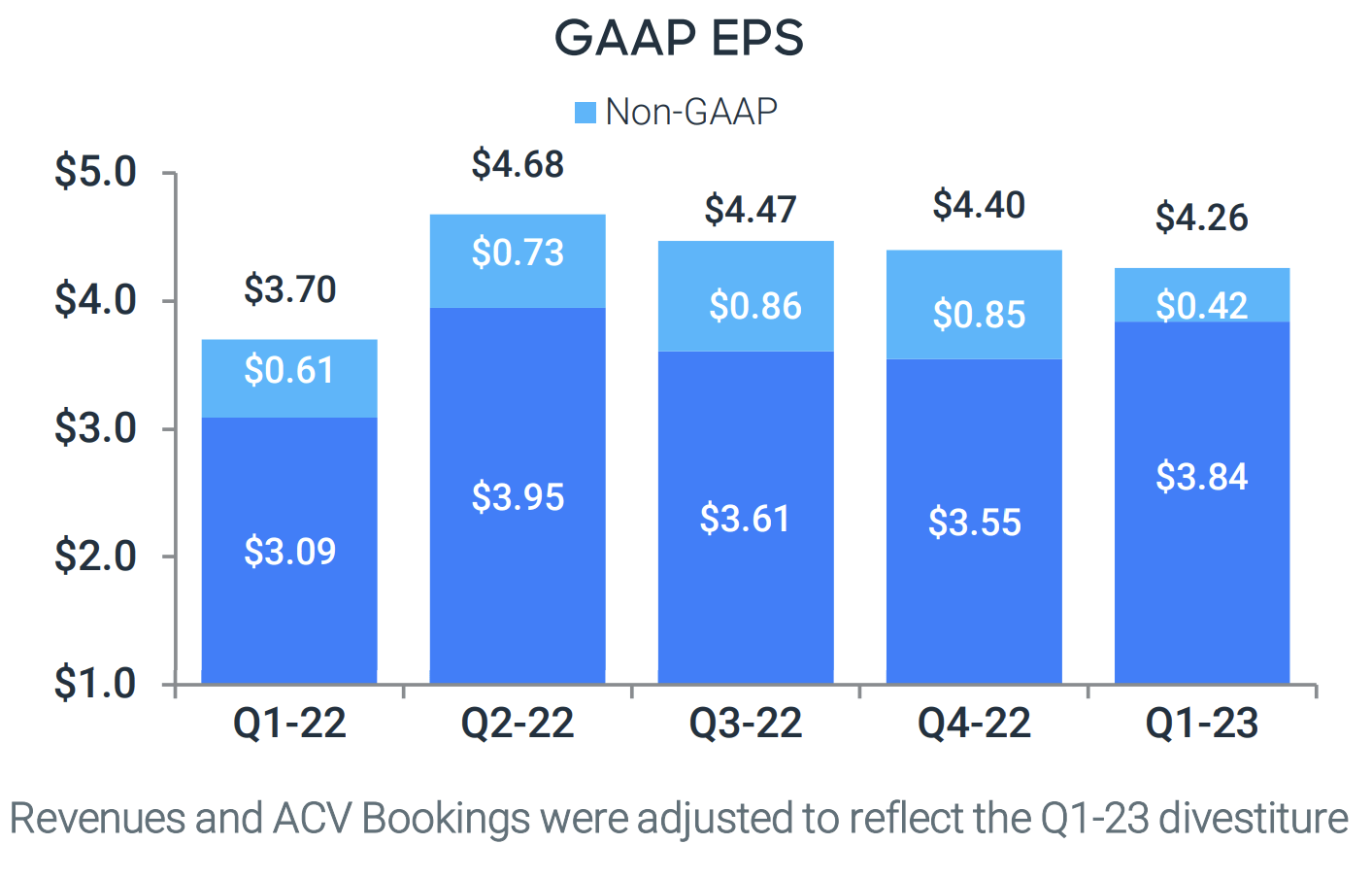

For Q1,FY23, FICO reported earnings per share [EPS] of $3.84, which beat analyst expectations by $0.32 and increased by a rapid 24.67% year over year. On a Non GAAP basis EPS was $4.26, which increased by 15.1% year over year.

EPS (Q1,FY23)

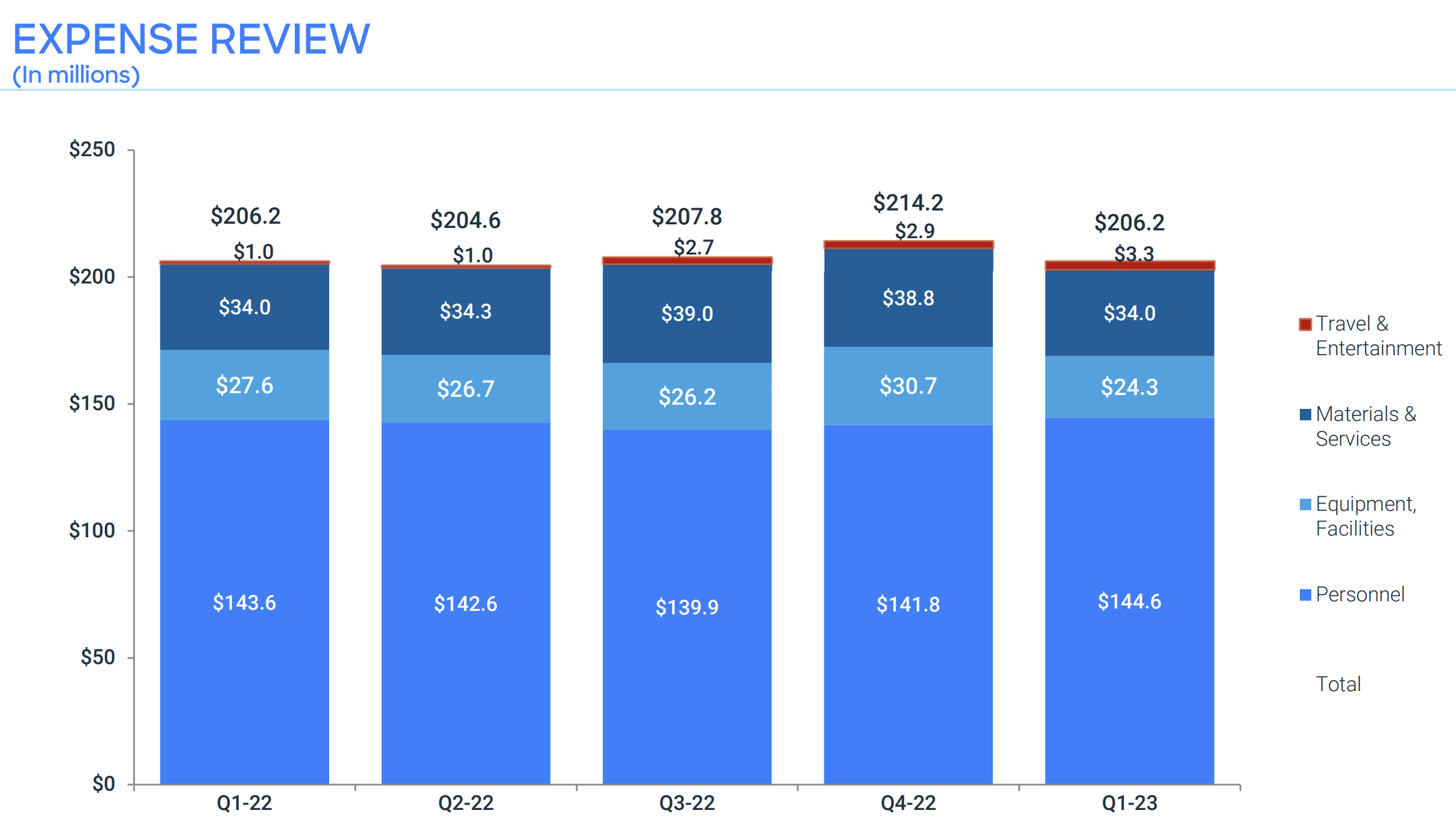

Its profitability improvements was driven by solid revenue growth as well as a stable operating expenses with $206.2 million reported. Operating expenses were also down from the $214.2 million reported in the prior quarter.

Breaking down expenses by segment, we can see Personnel costs make up the majority (70%) of expenses or $144.2 million. This is followed by equipment and facilities at $24.3 million or 11.8% of total revenue. In addition, to material & services revenue of $34 million.

Expenses (Q1,FY23)

FICO reported $166 million in cash and marketable investments on its balance sheet. The company does have fairly high total debt of $1.92 billion. This may seem like a red flag given the rising interest rate environment, but there is a positive. Approximately 67% of its debt is at a fixed interest rate, while its variable rate debt can be paid back at any time. Therefore management plans to utilise excess cash flow to reduce this debt, which I believe is a prudent and positive.

Guidance

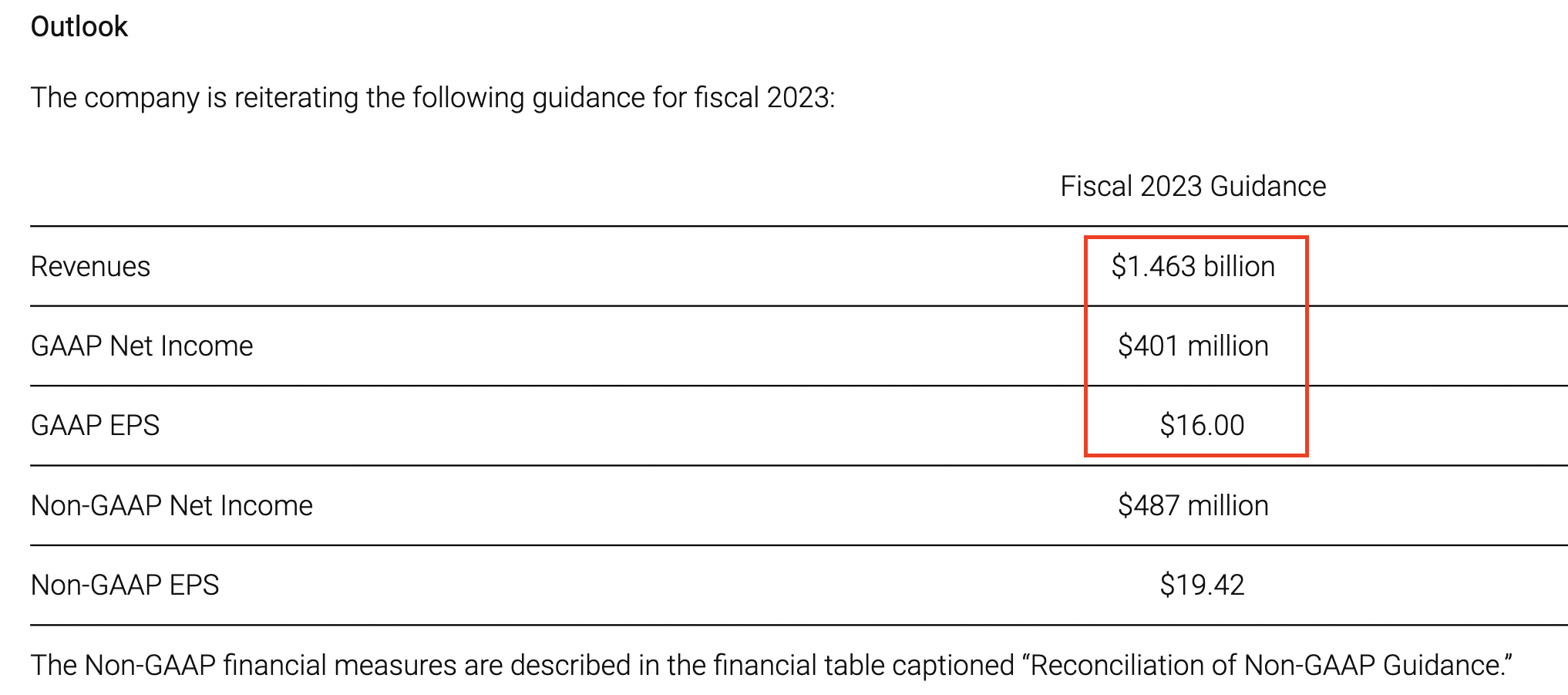

Moving forward for the full fiscal year of 2023, management has forecast $1.463 billion in revenue, which would represent a steady increase of 6.24% year over year. This is not a blistering growth rate, but it would be higher than the 4.61% growth rate reported in FY22 and measly 1.7% growth rate reported in FY21. I suspect this growth rate improvement is actually driven by the aforementioned divestitures of its slow growing businesses, which has bolstered its growth profile. Management has also forecast GAAP net income of $401 million, which would represent an increase of 7.36% year over year, which would be solid given the “recessionary” environment forecast.

Guidance (Q1,FY23)

Valuation?

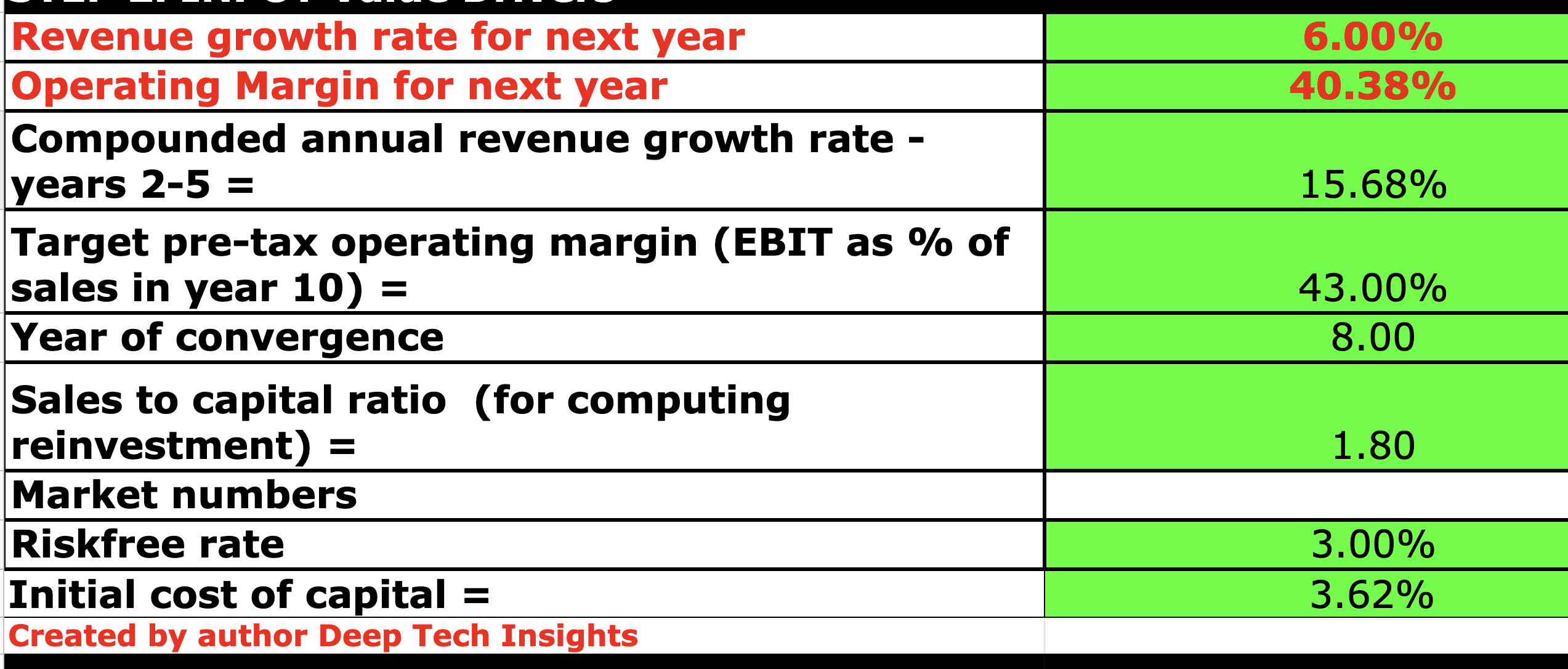

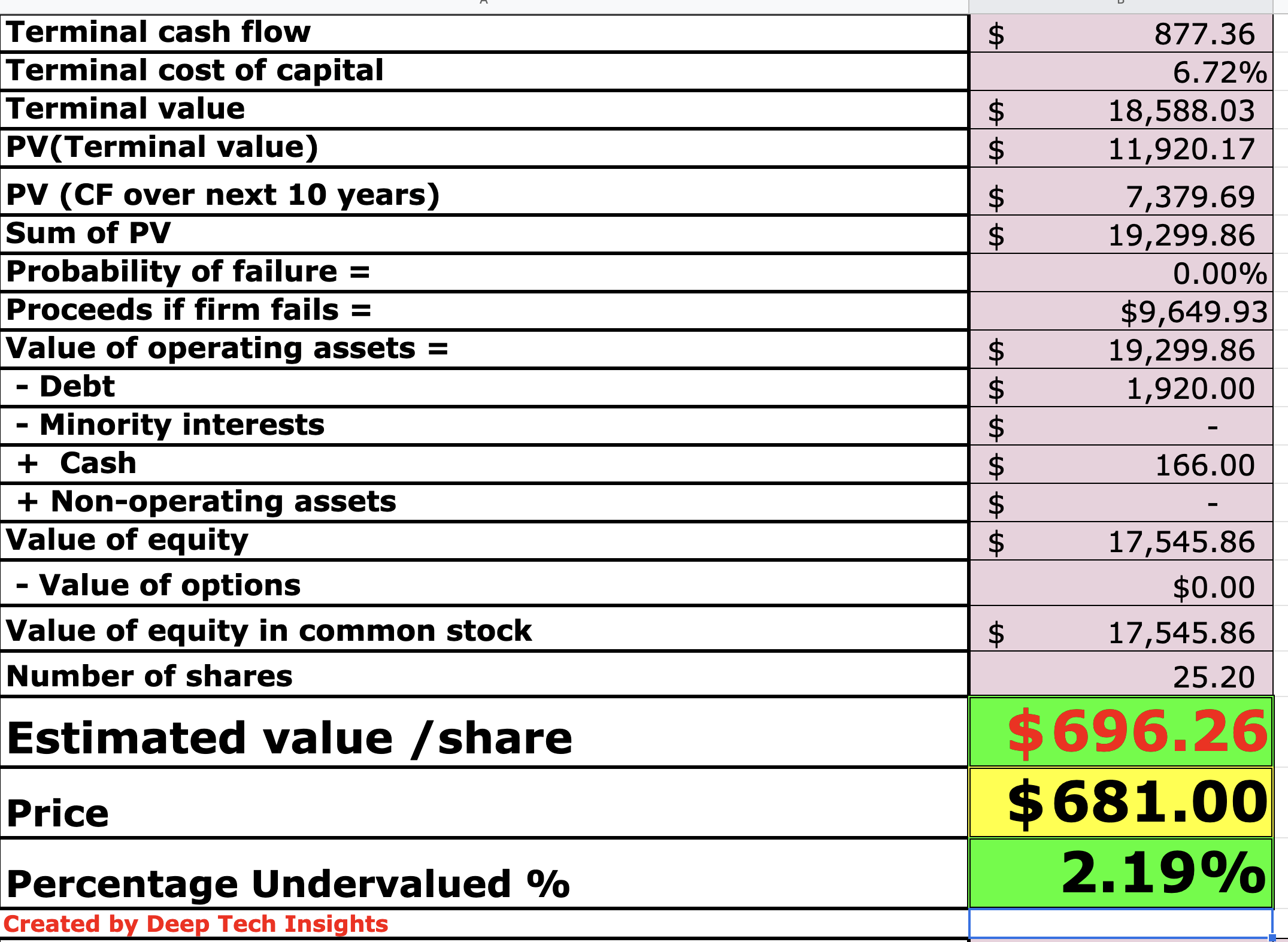

In order to value FICO I have plugged its latest financial data into my discounted cash flow model. I have forecast just 6% revenue growth for “next year” which is the full year of 2023 in my model, this growth rate is in line with analyst forecasts. In years 2 to 5, I have been slightly more optimistic and these metrics are based upon analyst forecasts on Yahoo Finance. I believe growth rate will driven by improving macroeconomic conditions, as the mortgage originations part of the business and its consumer FICO scores will likely rebound. In addition, its software on “platform” solution increased its ARR by 46% year over year, thus as more of its customers convert to this solution, I believe overall revenue growth would accelerate. FICO has also been moving into Africa, a largely untapped market through a variety of partnerships which could prove to be lucrative.

FICO stock valuation 1 (Created by author Deep Tech Insights)

Onto to margins, I forecast expenses to increase slightly for the full year of 2023, as management alluded to salary increases and headcount growth, which would increase the expense figure for its large line item (personnel) which makes up 70% of its total expenses. However, over the next 8 years in aggregate I forecast its operating margins to increase by over 2.4%, due to a large portion of software on platform customers and strong account expansion through its cross-selling strategy, which has been effective so far in driving high net dollar retention rates discussed previously.

FICO stock valuation 2 (created by author Deep Tech Insights)

Given the optimistic growth rate forecasts for years 2 to 5, I get a fair value of $696.26 per share and thus the stock is just over 2% undervalued. In my investment strategy I generally like to look for a “margin of safety” of between 10% and 20% below an intrinsic valuation calculation to determine a stock as a “Buy”. In this case, I will deem the stock as a “Hold” as I also used fairly optimistic forecasts.

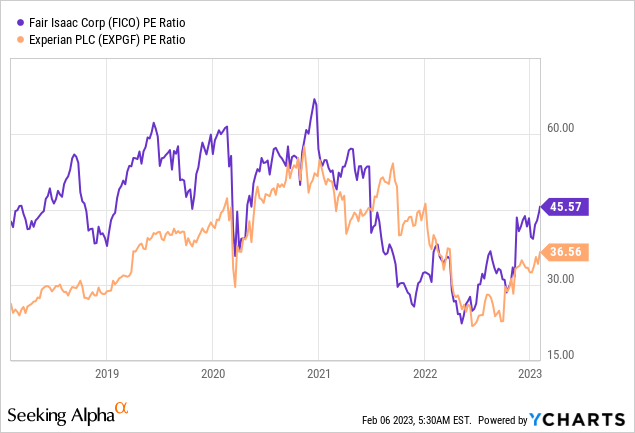

For extra information, FICO also trades a forward PE ratio = 40.6, which isn’t exactly cheap relative to the I.T sector average of 24. However, it is 9% cheaper than its 5 year average. FICO also trades at a higher valuation on a PE ratio basis, than credit score provider Experian (OTCQX:EXPGF).

Risks

Lower Demand/Recession

Many analysts have forecast a recession in 2023, thus I forecasts continued lower demand for FICO’s credit score offering and also mortgage originations due to the high interest rate environment. However, I forecast these issues to only be temporary due to the cyclical nature of the economy.

Final Thoughts

FICO is a high quality company with an elite list of large banks and financial institutions. The company’s credit score business has “share of mind” with its customers while its high product retention means stable earnings comes as standard. As the business has now divested its slower growth segments and has aligned its focus on the platform software, i forecast solid growth moving forward. However, even with these factors the stock is only slightly undervalued or “fairly valued” in my eyes.

Be the first to comment