Khosrork

One of the biggest challenges facing Americans this year has been maintaining their standard of living in the face of the highest inflation that we have seen in more decades. This has forced many people to take on second jobs or begin spending time performing odd tasks in order to get the extra money needed simply to keep themselves fed. Fortunately, as investors, we have other methods that we can employ to obtain the extra money that we need to cover our bills. One of the best of these methods is to purchase shares of a closed-end fund that focuses on the generation of income. These funds are not often discussed in the media but they provide investors with an easy way to obtain a portfolio of assets that can in many cases deliver a higher yield than pretty much anything else in the market. In this article, we will discuss the Flaherty & Crumrine Preferred and Income Securities Fund (NYSE:FFC), which is one fund that investors can use for purpose of income generation. This fund yields a phenomenal 7.92% at the current price so it certainly performs this task quite well. As this fund is currently trading at a reasonable price, let us investigate and determine if it could be a good addition to a portfolio today.

About The Fund

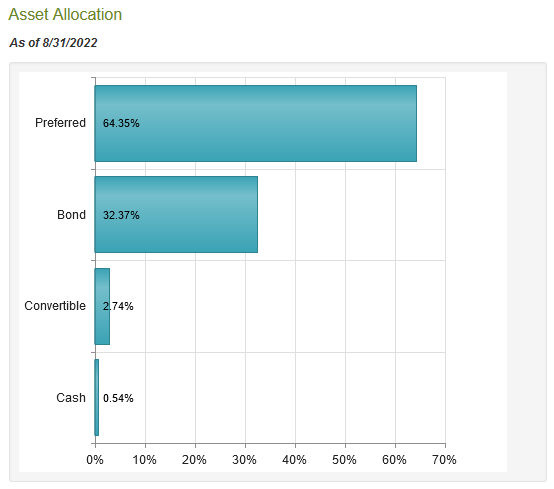

According to the fund’s webpage, the Flaherty & Crumrine Preferred and Income Securities Fund has the stated objective of providing its investors with as high a level of current income as possible without jeopardizing the preservation of capital. This is a very common objective among fixed-income funds and it should appeal to more risk-averse investors, such as many retirees. It makes sense too since fixed-income securities are generally a good investment for those investors that are interested in preserving principal. This is particularly true with bonds, as a bond will always return your principal to you if held until maturity (barring the rare default). However, as the name of the fund indicates, this one does not solely invest in bonds. In fact, the majority of the fund’s holdings are in preferred stock:

CEF Connect

Preferred stock is something of a hybrid between common stock and bonds. As is the case with bonds, the preferred stock will pay a fixed dividend to its holders. In addition, the preferred stock does not participate in the growth and prosperity of the underlying company. Thus, the dividend paid by these shares will not generally go up just because the company’s profits did. Unfortunately, the dividend is not a mandatory payment as it is with bonds. A company can fail to pay a preferred stock dividend without going into default. However, the issuing company cannot make any dividend payment to the common stockholders if it does not pay one to the preferred stockholders. This adds a margin of safety to the preferred stockholders as most companies that issue preferred stock place great emphasis on paying a reliable dividend to their common stockholders. Thus, in most cases, a company will do everything in its power to ensure that the preferred stock dividends get paid on time and in full. Finally, unlike bonds, preferred stocks do not mature so there is no guarantee that all the principal will be recovered simply by holding the asset for long enough.

As neither preferred stock nor bonds have any link to the growth and prosperity of the underlying company, they are not priced based on the performance expectations of the issuing company. Rather, they are priced based on interest rates. This is because the payment that the security makes to the investor is determined by the market interest rate in the economy at the time of issuance. As such, bonds issued when rates are high will have a higher yield-to-maturity. In that situation, no investor will pay full price for an existing bond with a lower yield so the price of those existing bonds will need to decline so that they deliver the same yield-to-maturity as a newly issued bond with the same characteristics. The same thing applies to preferred stocks, which also decline in price when interest rates rise.

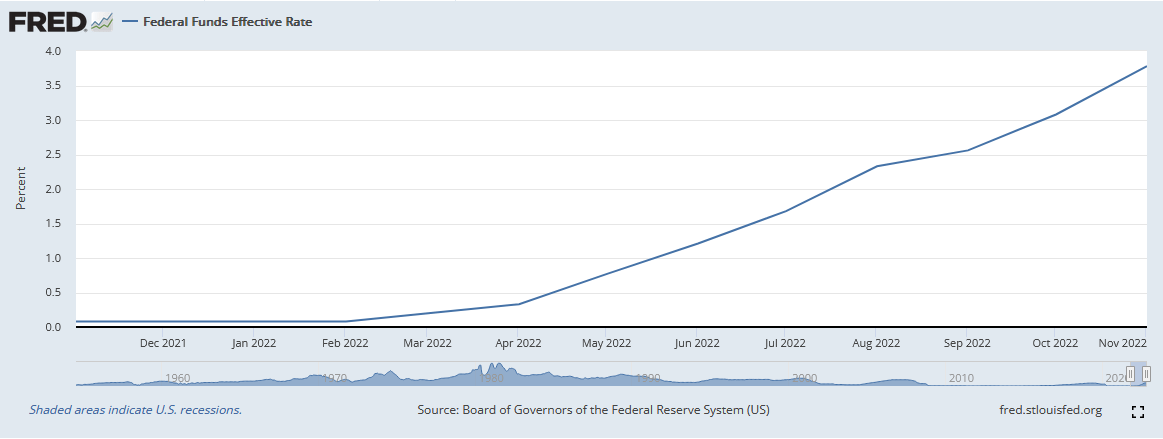

As everyone reading this is certainly well aware, the Federal Reserve has been aggressively increasing the market interest rate in the United States over most of 2022:

Federal Reserve Bank of St. Louis

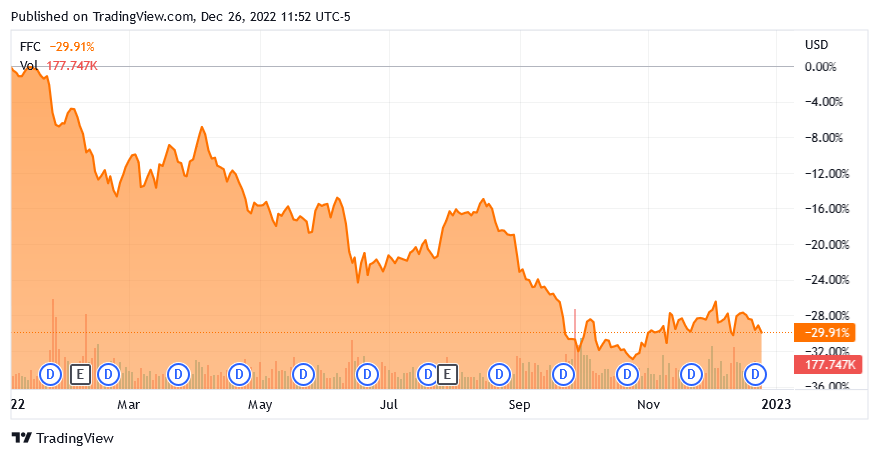

Back in February, the federal funds rate (the benchmark interest rate in the United States) stood at 0.08% but it stands at 4.25% to 4.50% today. This has caused the price of bonds and other fixed-income securities all across the market to decline. We see this in the performance of this fund as the Flaherty & Crumrine Preferred and Income Securities Fund is down 29.91% year-to-date:

Seeking Alpha

This is notably greater than the 20.38% decline of the ICE Exchange-Listed Preferred & Hybrid Securities Index (PFF). The biggest reason for this is that the Flaherty & Crumrine Preferred and Income Securities Fund uses leverage, which we will discuss in a bit. Unfortunately, the fund’s decline is unlikely to reverse itself anytime soon. The Federal Reserve has already projected that it will raise rates to at least 5.1% in 2023. I have seen independent projections that the Federal Reserve will raise rates by much more than that but the central bank is not currently making such statements. Regardless, it is a near certainty that the Federal Reserve will raise rates further and likely keep them there for an extended period. As such, anyone that suffered from the year-to-date decline will probably not see their position return to its previous size anytime soon. However, someone buying today will only have to worry about future rate hikes and will benefit when and if the Federal Reserve pivots.

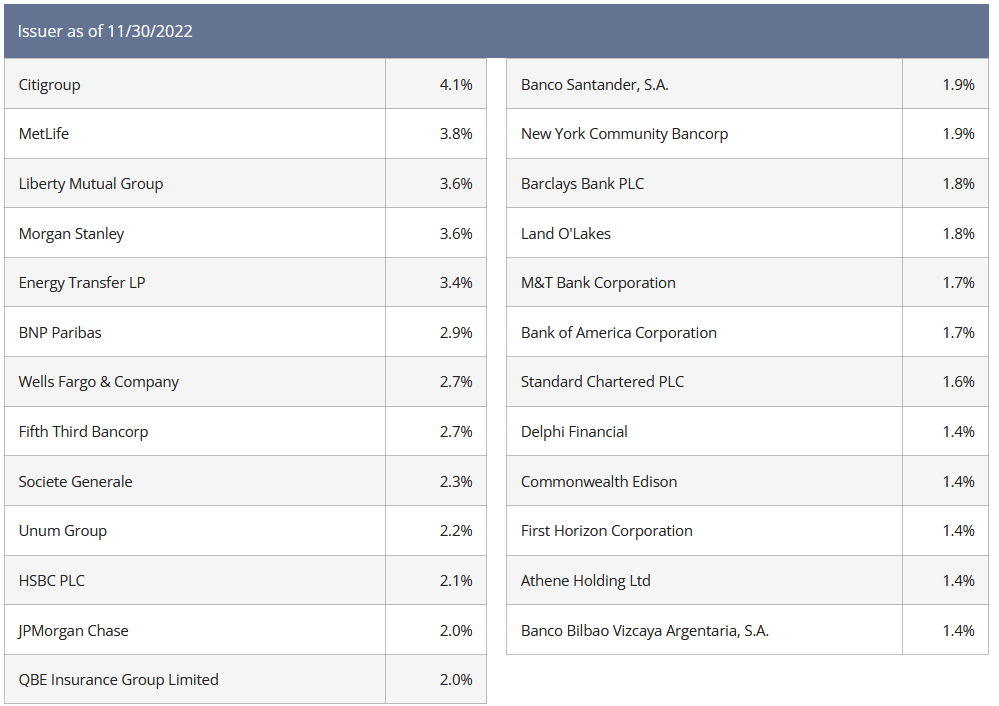

A look at the largest positions in the fund reveals that it is heavily invested in banks and other financial firms:

Flaherty & Crumrine

This is not unusual for a preferred stock fund, however, because banks are the largest issuers of preferred stock in the market. This is due to international banking regulations that require a bank to maintain a certain percentage of its assets in the form of Tier one capital. Tier one capital is that proportion of a bank’s assets that are not also a liability to someone else (such as a depositor). There are two ways for a bank to obtain Tier one capital, which are the issuance of either common or preferred stock. As such, most banks will opt to issue preferred stock when regulators require them to increase their Tier one capital in order to avoid diluting the common shareholders. These regulations are unique to banks, however, as no company in any other industry has similar rules. Thus, most other companies will opt to issue debt instead of preferred stock when they need to raise capital as debt is much cheaper. This by default leaves the banking sector as the largest issuer of preferred stock in the market. Thus, any preferred stock fund will by necessity include significant exposure to the banking sector. With that said though, this fund is only 53.9% weighted towards banks, which is much less than some other preferred stock funds and ETFs. This may be comforting to anyone that is worried about being overly exposed to the banking sector today.

As my regular readers on the topic of closed-end funds are no doubt well aware, I do not generally like to see any single position in a fund account for more than 5% of the fund’s assets. This is because this is approximately the point at which a position begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification but if the asset accounts for too much of the portfolio, then it will not be completely diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not, and if it accounts for too much of the portfolio then it may end up dragging the entire fund down with it. As we can see above though, that is not a problem here as there is no individual issuer that accounts for an outsized position in the portfolio. Even the largest issuer, Citigroup (C), is only 4.1% of the fund. It, therefore, appears that this fund has reasonable diversification and we should not be especially concerned about the risks presented by any individual company whose securities are represented in the portfolio.

Leverage

As stated earlier in this article, a closed-end fund like the Flaherty & Crumrine Preferred and Income Securities Fund has the ability to employ certain strategies that have the effect of boosting its overall yield. One of these strategies is the use of leverage. Basically, the fund borrows money and then uses that borrowed money to purchase fixed-income assets. As long as the interest rate on the borrowed funds is lower than the yield of the purchased assets, this strategy works pretty well to boost the overall portfolio yield. As the fund is able to borrow at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword because leverage boosts both gains and losses. This is one reason why the fund has significantly underperformed the preferred stock index so far this year. As such, we want to ensure that a fund is not employing too much leverage because that would expose us to too much risk. I do not typically like to see a fund’s leverage above a third as a percentage of its assets for this reason. The Flaherty & Crumrine Preferred and Income Securities Fund is unfortunately quite a bit above this as its levered assets currently comprise 39.53% of the portfolio. In the past, I have been willing to allow fixed-income funds to carry more leverage than equity funds due to the fact that their assets are somewhat more stable price-wise but this fund still has more leverage than I really want to see. Caution is urged here as the fund will probably decline more than might be expected as interest rates continue to rise over the next several months.

Distribution Analysis

As stated earlier in the article, the primary objective of the Flaherty & Crumrine Preferred and Income Securities Fund is to provide its investors with a high level of current income. In order to do this, the fund invests in a levered portfolio that primarily consists of preferred stocks, which tend to have fairly high yields themselves. As such, we might assume that the fund boasts a fairly high distribution yield. This is certainly the case as it currently pays a monthly distribution of $0.10 per share ($1.20 per share annually, which gives the fund a 7.92% yield at the current price). Unfortunately, it has not been particularly consistent about this distribution over its history and the fund even cut its distribution four times this year:

CEF Connect

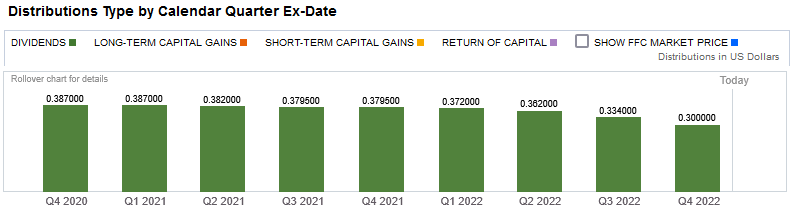

The fact that the fund’s distribution has varied so much over time will likely reduce its appeal for those investors that are looking for a steady and consistent source of income with which to pay their bills or cover other expenses. However, these same conservative investors may be somewhat comforted by the fact that the distributions consist entirely of dividend income:

Fidelity Investments

The reason that this may be comforting is that dividend income is by far the most sustainable source of money to cover distributions. After all, a return on capital can be a sign that the fund is returning the investors’ own money back to them. A capital gains distribution depends on the fund actually generating sufficient capital gains, which is something that has been quite difficult during the market that we have seen this year. In contrast, companies very rarely cut their distributions, which is particularly true with preferred stock and bond payments. However, as I have pointed out in the past, it is possible for these distributions to be misclassified. As such, we want to investigate exactly how the fund is financing the distributions that it pays out so that we can determine how sustainable they are likely to be.

Unfortunately, we do not have an especially recent document to consult for this purpose. The fund’s most recent financial report corresponds to the six-month period ending May 31, 2022. As such, it will not include any information about the fund’s performance over the past seven months. However, the Federal Reserve started its monetary tightening regime in March so we will still get a good idea of how well the fund managed to negotiate that. It should also give us some insight into whether or not the fund is actually generating enough income to cover its distributions. During the six-month period, the Flaherty & Crumrine Preferred and Income Securities Fund received a total of $16,332,647 in dividends and another $24,750,314 in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources, the fund brought in a total of $41,180,702 in income during the period. The fund paid its expenses out of this amount, leaving it with $34,412,201 available to its investors. This was unfortunately not enough to cover the $35,170,325 that the fund actually paid out in distributions, although it did get pretty close. At first glance though, this may be somewhat concerning.

The fund does have other methods that it can utilize in order to obtain the money that it needs to cover its distributions. One possibility is through capital gains. As we might expect given the Federal Reserve’s actions during the reporting period though, the fund was quite unsuccessful at this. During the six-month period, the fund reported net realized losses of $895,581 along with net unrealized losses of $141,252,785. Overall, the fund’s asset base decreased by $134,754,470 during the period. This is likely the reason for the distribution cuts as the fund needed to reduce in order to ensure that it could completely cover the distribution out of net investment income. We will need to wait until the fund releases a new full-year report in order to verify whether or not it is successful, but it probably has been considering how close it got during the most recent reported period. We should receive this updated financial information in a few weeks.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on those assets. In the case of a closed-end fund like the Flaherty & Crumrine Preferred and Income Securities Fund, the most common way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of December 23, 2022 (the most recent date for which data is available as of the time of writing), the fund had a net asset value of $15.97 per share but the shares currently trade for $15.16 per share. Thus, the shares currently trade at a 5.07% discount to the net asset value. This is a much better price than the 2.80% discount that the shares have had on average over the past month so today’s price certainly looks reasonable for anyone looking to buy.

Conclusion

In conclusion, the Flaherty & Crumrine Preferred and Income Securities Fund certainly has an appealing proposition for anyone today. After all, we could all use income, particularly today as the high inflation rate has been robbing us of buying power. Unfortunately, the Federal Reserve’s continual monetary tightening and the fund’s high leverage will likely result in share declines over the next several months. Thus, it may make sense to buy in once interest rates have gotten closer to their peak and avoid those unrealized losses. The fund does have an attractive price today, but it still may be best to wait.

Be the first to comment