assalve/iStock Unreleased via Getty Images

Introduction

Ferrari (NYSE:RACE) is a cornerstone of my portfolio. Superior brand-recognition, coupled with superb supercars and a very predictable business model makes me very confident about this investment.

Ferrari is also a one of those stocks usually considered overvalued and too expensive. This is why value investors usually stay away from it. However, I started buying Ferrari exactly because I think the stock reflects a premium the company actually deserves, as I have tried to show a few times on SA.

On a personal note, I am a little fond of Ferrari because the first article (and one of my favorite ones) I ever published on SA was about it. Of course, I was bullish. Since then, the company has offered a total return close to 25% vs. -0.29% returned by the S&P500.

Ferrari recently reported its Q4 and FY2022 earnings report and provided its first 2023 guidance. In addition, it just unveiled the new SF-23, the car we will see during the 2023 Formula 1 World Championship.

I don’t like the expression “no-brainer”, since every investment requires a thought process. However, every time I look at Ferrari, I see many evident reasons supporting the bull-case. Here we will take a look at some of them.

The bull-case

I don’t want to spend a lot of words on a general introduction, since Ferrari is a very well-known company and, according to Brand Finance, it is currently the 7th strongest brand in the world.

Here are the main aspects I like about the company:

- It manufacturers cars, but its products are actually luxury vehicles. Therefore, it has rather high margins compared to all other car manufacturers.

- Its business model is very restrictive on volumes, staying true to what Enzo Ferrari said: “Ferrari will always deliver one car less than the market demand”. This creates product exclusivity and strong pricing power.

- Ferrari’s business model makes it easy for investors to predict future earnings and cash flows.

- Ferrari’s TAM is increasing as more people around the world enter into the category of HNWI (high-net-worth individual) who have liquid assets of at least $1 million.

- Ferrari is a best-in-class technological innovator: it is already manufacturing hybrid cars and by 2025 it will unveil its first all-electric car, where, we know, there will be a unique way to perceive the new sound of the engine.

- The new Purosangue (Italian for “thoroughbred” is a game-changer as it developed a new kind of vehicle a four-door four-seater luxury sports car.

- Purosangue order books are full. This means a high-margin vehicle with many personalization optionals will impact significantly Ferrari’s financials.

- Ferrari is a perfect fit for a dividend growth portfolio, with growing free cash flows that support growing dividends (with a low payout ratio) and share repurchases. An important fact is that Ferrari doesn’t have stock-based compensation, thus there is no dilution of buybacks nor any accounting problem when looking at free cash flow.

Full Year 2022 Results: highlights and thoughts

Usually, we start considering an earnings report from the top-line. This time I want to start from something outside of the financial statements. It is something I consider extremely relevant to assess Ferrari.

The Prancing Horse, in fact, disclosed that its order book extends well into 2024. Yes, you have read the date right: 2024.

The implied consequence is clear: Ferrari already knows fairly well what to expect from 2023.

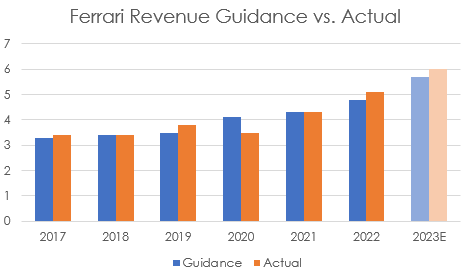

This is one of the key aspects I like about the company: it is highly predictable. In addition, the company is used to provide a guidance at the beginning of the year that it can reasonable meet and, oftentimes, beat. We can see this from the graph below, where the only exception is 2020, for obvious reasons.

Author, with data from Ferrari’s reports

For this past year, Ferrari had initially provided a net revenue guidance of €4.8 billion. Since, my first article back in May, I was inclined to think Ferrari would reach €5 billion. It actually reached €5.1 billion, as we can see from the highlight slide taken from the results presentation.

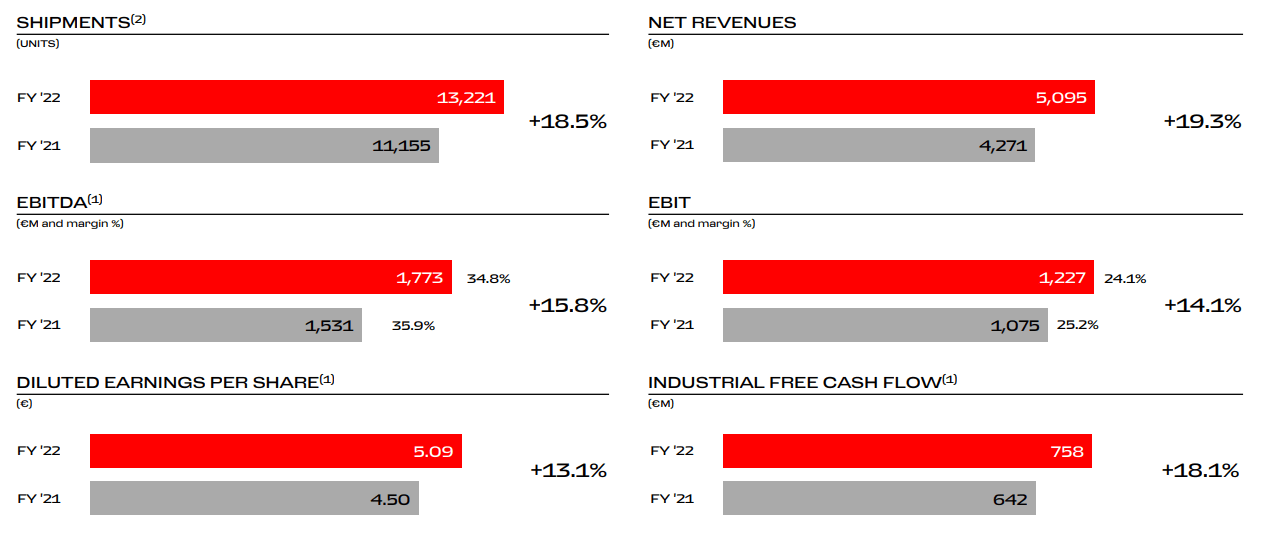

Ferrari Q4 Results Presentation

Using the slide, we can also figure out a few things. First of all, revenues increased 19.3%, more than the +18.5% seen in shipments, meaning that the price/volume mix was favorable. I expect this difference to increase next year, as Purosangue sales pick up.

On the other hand, Ferrari too experience a bit of margin compression both on EBITDA and EBIT. However, these have been years where Ferrari has pounded on capex to develop hybrid and all-electric cars, creating new cutting-edge technology up to its iconic and exclusive reputation. Considering these investments, the result on margins is quite good. This leads to EPS and industrial free cash flow growth.

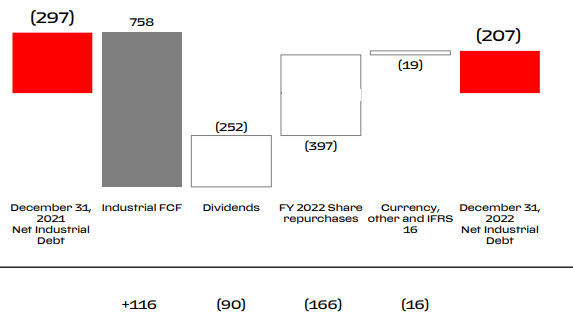

It is important to focus on the industrial side of the business because Ferrari has a financial branch which has its operations and, most importantly, its debts, linked to the financing activities.

Therefore, to get a grasp of the core business, we have to look at industrial free cash flow and industrial debt. Here below, we can see how Ferrari generated strong industrial FCF during 2022 that more than covered its dividends and its share repurchases, while being also used to reduce the net industrial debt (already quite low) by another 30%. It is the industrial debt that represents a company’s operational risk. I don’t want to sound too enthusiastic, but, to me, it seems like we are before an fortress, operationally speaking.

Ferrari Q4 Results Presentation

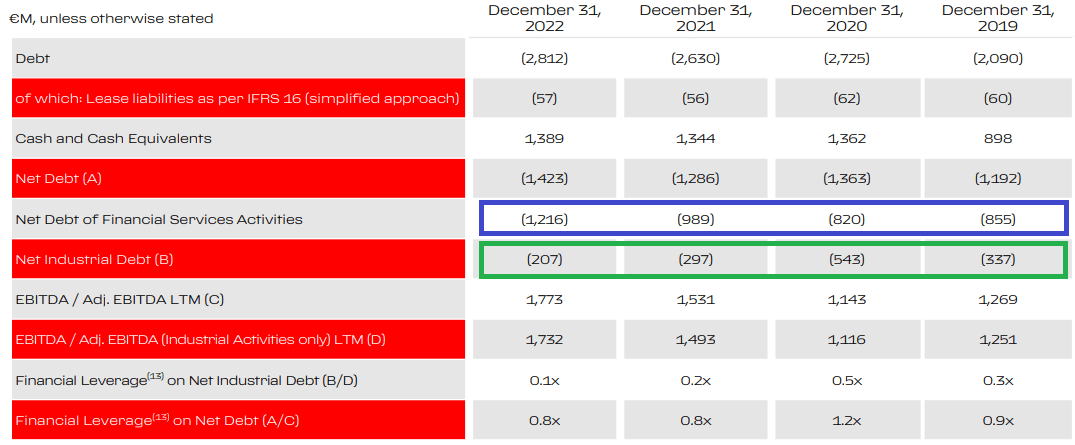

Having seen this, we can look at the reconciliation of non-GAAP measures to show the net industrial debt. As we can see, it spiked up during the pandemic, but Ferrari was able to bring it down aggressively already in 2021, to the extent it was already below its 2019 levels.

Ferrari Q4 Results Presentation

On the other hand, we see the net debt of financial activities increase. This should not be seen as a big issue, but actually as something positive because it shows how the financial activities are actually growing. Most automakers have such a branch and it is accounted for as debt.

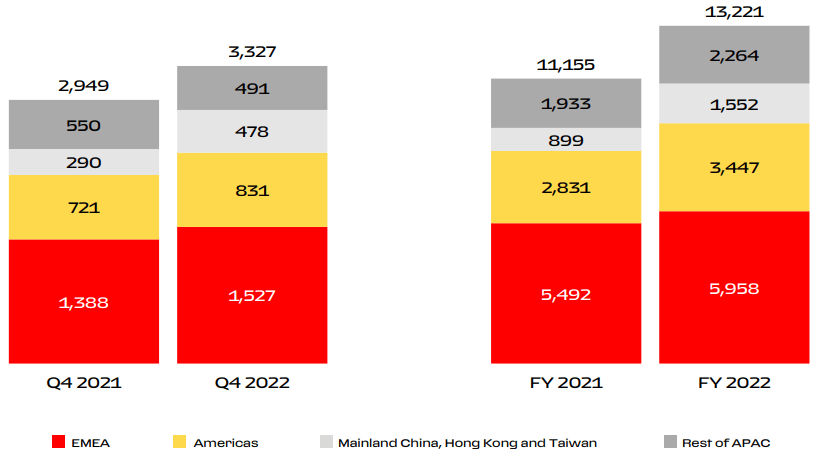

Geography

Let’s take a look at Ferrari’s sales by geography. We see the impressive YoY growth in China, Hong Kong and Taiwan. If we compare the two full year results we have a 72% increase, which can also be explained with the reopening of China. Some SA readers may know I am not really fond of being exposed to China. However, Ferrari addresses a particular niche of customers and enjoys such a strong brand-recognizition that I see it somewhat more immune to geo-political tensions and conflicts.

Overall, we see strong performance in the Americas, too, where shipments increased by 21.7%. It is clear demand is still there for Ferraris and I think it would not be surprising to see the Maranello-based manufacturer end up selling around 18,000-20,000 vehicles per year by 2028.

Ferrari Q4 Results Presentation

The Purosangue effect

During the earnings call, Ferrari’s management reported some interesting news regarding the Purosangue:

The Purosangue order intake has been extraordinarily high, well beyond our expectations. But the enthusiasm of our clients is expressed also by their attendance level at all our events. In fact, in 2022, we had an unprecedented number of unrivaled client engagement experiences.

In particular, it was highlighted how the Purosangue is a car where personalizations are quite high in proportion to total revenues, making Ferrari reach an 18% of total personalization revenue compared to revenues from cars and spare parts.

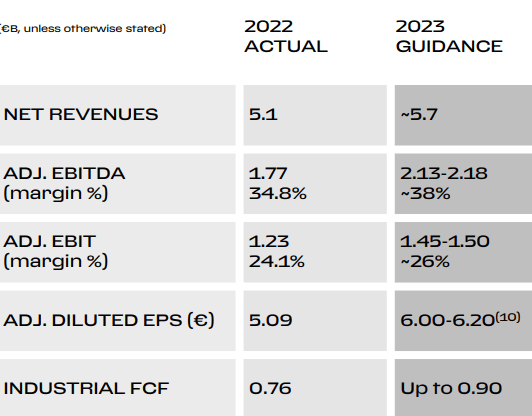

Guidance

Let’s get to a point the market seemed to appreciate: Forward guidance. Where is Ferrari headed towards?

In my past research I wrote I expected Ferrari to reach a revenue of €5.5 billion in 2023 and to break the €6 billion barrier in 2024. My thought was that Purosangue sales should generate 20.7% of total revenues in 2023 and 21.8% in 2024. This made me consider Ferrari able to reach an adj. EBITDA margin of 37% in 2023 and a 38% in 2024, which would have led to a 2023 adj. EBITDA above €2 billion and around €2.28 billion in 2024. I also wrote I was forecasting that EBIT margin will increase, projecting it at 26.5% in 2023 and 28% in 2024, which translates into a 2023 EBIT of € 1.33 billion and of €1.68 billion in 2024.

I thought I was already being a bit bold, however Ferrari surprised me too, providing higher than expected guidance.

In fact, the Prancing Horse forecasts net revenues of €5.7 billion with an adj. EBITDA margin of 38% well above €2 billion. Regarding EBIT margin Ferrari is in line with my forecast of 26% in 2023.

Ferrari Q4 Results Presentation

Given this guidance, I think it is reasonable to expect Ferrari to come close to €6 billion in net revenues at the end of this year, which, with an adj EBITDA margin of 38% would mean € 2.28 billion of EBITDA. I wouldn’t be surprised either if the company reached €1 billion in industrial FCF. But, once again, I would like to stress one point: Ferrari is not an investment focused on huge estimation beats, but rather on steady and highly reliable growth generated by the moat provided by brand exclusivity and product quality.

An eye on Formula 1

Last year, Ferrari started the World Championship with a Grand Prix win and for the first half of the year it seemed to be able to compete for the title. However, the second half of the championship saw Ferrari hit by reliability issues and the racing team came in second position. However, returning to compete for the title increased revenues from sponsorships. This year, Ferrari just unveiled its new SF-23, which has serious ambitions of winning the championship.

Ferrari Racing website

Though the revenues from sponsorships is not a major concern for Ferrari, results in Formula 1 are, as they have a direct impact on how the company is perceived around the globe. Ferrari has stated many times that winning the championship is a key focus of the whole company, not only the racing team. Let’s see what happens this year to this regard.

Valuation and conclusion

I think few people can object to the quality Ferrari has as a company. But many people believe the stock to be too expensive. I have shared many times in my previous articles that I think Ferrari should trade in a range between $260-290 a share.

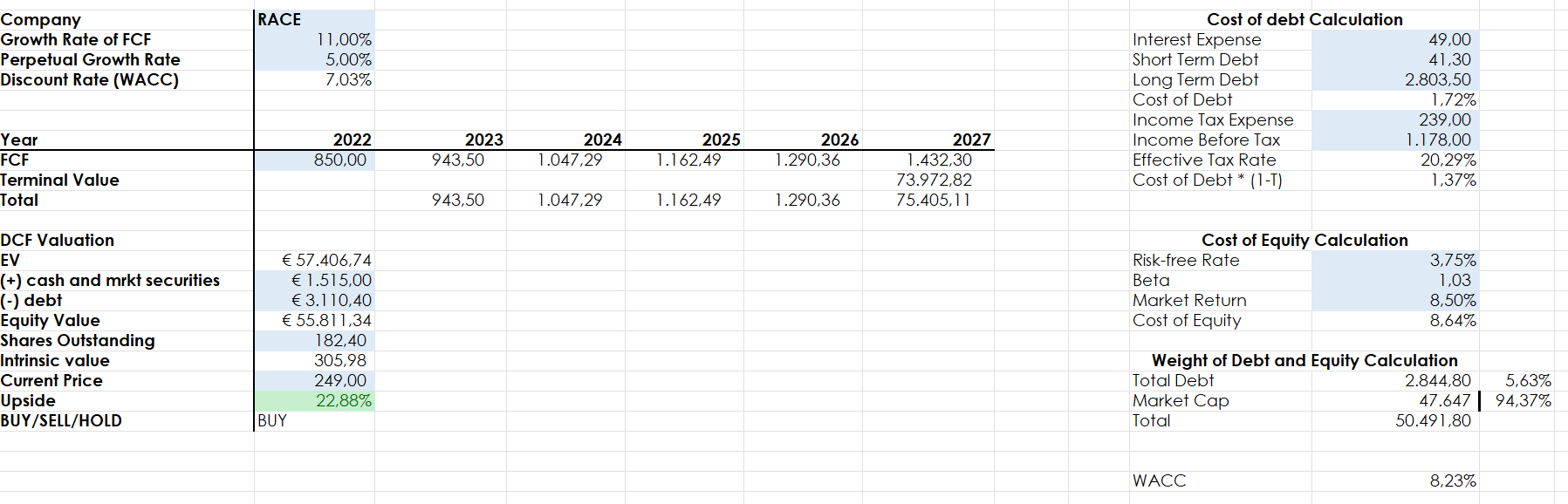

Given the new guidance and the fact that I think Ferrari will overdeliver, I plugged in a FCF growth rate of 11% for the next 5 years. I also discount the cash flows considering Ferrari worth of a premium. Instead of using its WACC of 8.23%, I take away 1.2 percentage points to use a discount rate close to 7%. I think a business like Ferrari’s well deserves such a premium. Please notice all numbers are in Euro, since this is the currency Ferrari uses to report its financial data.

Author, with data from SA and own estimates

With these numbers, I find Ferrari to be once again a stock with some interesting upside. First of all, my target price has broken the €300 barrier, which in USD is currently equal to $318 per share. This is why Ferrari is still a buy for me and it is a stock I always try to buy more shares of.

Be the first to comment