Spencer Platt

By The Valuentum Team

Consumer-tied businesses, whether consumer staples or discretionary, are facing tremendous cost pressures, but some of those cost pressures are freight and logistics expenses. This might play into the hands of FedEx Corporation (NYSE:FDX) and rival United Parcel Service, Inc. (UPS).

For FedEx’s fiscal 2023 (ends May 2023), the company issued guidance for diluted earnings per share to the range of $22.45-$24.45, which when issued June 24, was above the consensus estimate of $22.40 at the time. FedEx was able to drive its fiscal fourth-quarter 2022 operating income higher due to a “favorable net impact of fuel,” but it did note that it experienced “lower shipment demand due to slower economic growth and supply chain disruptions.”

We think FedEx is better positioned to pass along costs than many, and for that reason, we think it will hold up better should the U.S. enter a recession. The same rings true for rival UPS, which reported first-quarter 2022 results on April 26. In UPS’ first quarter, consolidated revenues jumped 6.4% from the same period last year, while it grew consolidated operating profit 17.6% (12.1% on an adjusted basis). We think transportation stocks such as FedEx and UPS, which are able to pass along price increases in the form of surcharges for higher fuel costs, are much better positioned than the broader retailer landscape, which may face continued earnings pressure as they deal with higher input costs and larger inventory balances.

Here’s more about FedEx’s ability to price effectively to grow earnings from its 10-K:

FedEx Express has an indexed fuel surcharge for U.S. domestic and U.S. outbound shipments and for shipments originating internationally, where legally and contractually possible. FedEx Express fuel surcharges are adjusted on a weekly basis. The fuel surcharge is based on a weekly fuel price from two weeks prior to the week in which it is assessed. Some FedEx Express international fuel surcharges incorporate a timing lag of approximately six to eight weeks.

On the basis of our discounted cash-flow (“DCF”) process, we value FedEx at $293 per share, well above where shares are trading at the moment (~$230). While the company is not immune to recessionary characteristics, its flexible pricing surcharges mean it can handle cost adversity better than most S&P 500 entities, in our view. Shares of FedEx yield ~1.5% at the moment, and while the company’s dividend health could be stronger, we give it high marks for both dividend strength and dividend growth potential.

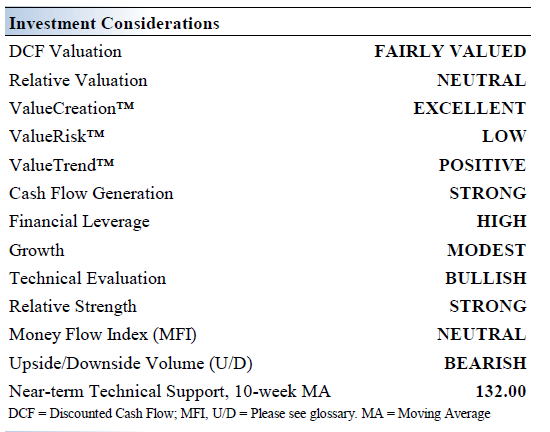

FedEx’s Key Investment Considerations

Image Source: Valuentum

FedEx provides customers and businesses worldwide with a broad portfolio of transportation, e-commerce and business services. The proliferation of e-commerce supports its growth outlook. FedEx operates under various segments including: FedEx Express, FedEx Ground, FedEx Freight, and FedEx Services. It was founded in 1971 and is based in Memphis.

FedEx’s acquisition of TNT Express gives it access to TNT’s European distribution network. Integration costs have come in higher than projected, but it is on track to achieve material pre-tax synergies, which will help drive incremental operating profit.

FedEx’s operations are capital intensive, characterized by significant investments in aircraft, vehicles, technology, facilities, and equipment. Capital expenditures have come in at ~7% of its sales in recent fiscal years. While FedEx is a tremendous generator of operating cash flow, its free cash flow performance is rather volatile, and the firm has a large net debt load.

FedEx’s outlook is supported by its impressive pricing strength, and future price increases should be expected. However, FedEx is also contending with major inflationary pressures, with an eye towards rising labor and fuel expenses. It will take time for recent pricing increases to be fully reflected in its financials, but we like how the company is positioned.

FedEx has significantly grown its dividend in recent years. Management remains committed to rewarding shareholders. FedEx’s business model has proven to be quite resilient even in the face of serious operational hurdles and various exogenous shocks.

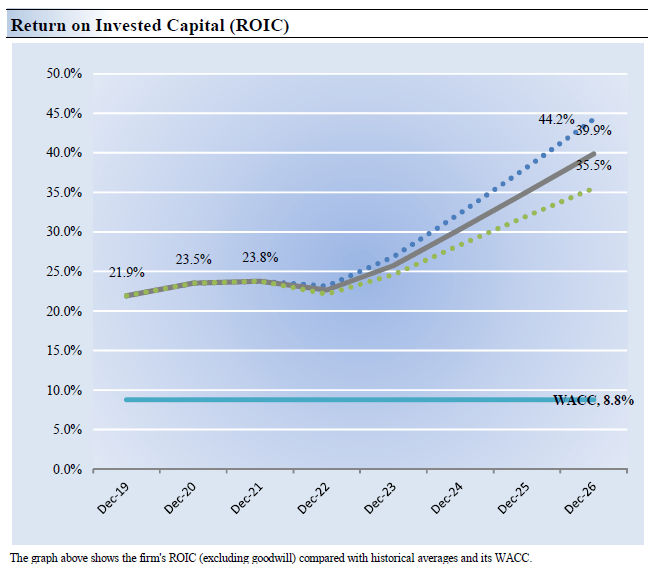

FedEx’s Economic Profit Analysis

The best measure of a company’s ability to create value for shareholders is expressed by comparing its return on invested capital with its weighted average cost of capital. The gap or difference between ROIC and WACC is called the firm’s economic profit spread. FedEx’s 3-year historical return on invested capital (without goodwill) is 14.2%, which is above the estimate of its cost of capital of 8.9%.

As such, we assign FedEx a ValueCreation rating of EXCELLENT. In the chart below, we show the probable path of ROIC in the years ahead based on the estimated volatility of key drivers behind the measure. The solid grey line reflects the most likely outcome, in our opinion, and represents the scenario that results in our fair value estimate. FedEx is a fantastic economic-value generator.

Image Source: Valuentum

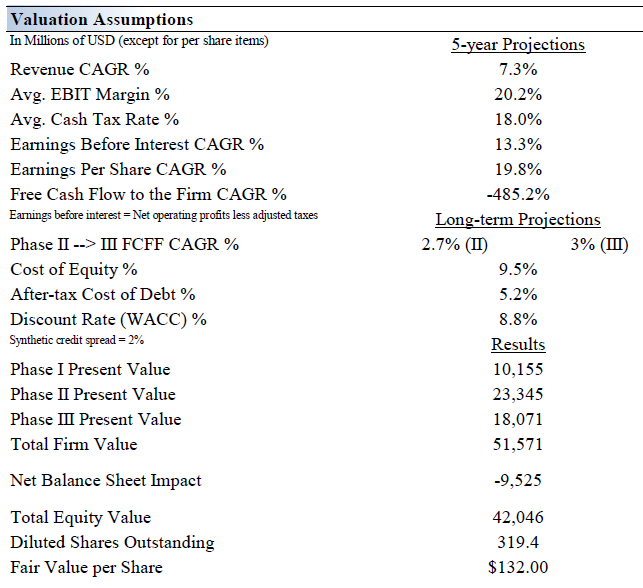

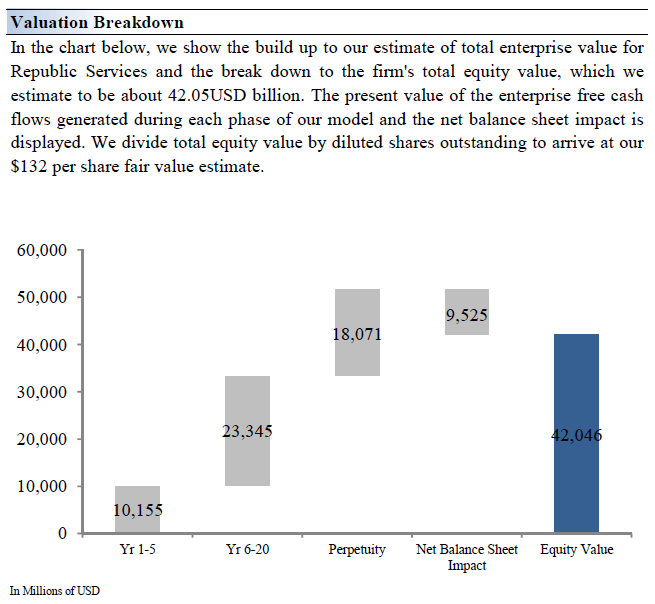

FedEx’s Cash Flow Valuation Analysis

Image Source: Valuentum

We think FedEx is worth $293 per share with a fair value range of $234.00 – $352.00. The margin of safety around our fair value estimate is driven by the firm’s LOW ValueRisk rating, which is derived from an evaluation of the historical volatility of key valuation drivers and a future assessment of them.

Our near-term operating forecasts, including revenue and earnings, do not differ much from consensus estimates or management guidance. Our model reflects a compound annual revenue growth rate of 4.1% during the next five years, a pace that is lower than the firm’s 3- year historical compound annual growth rate of 10.3%.

Our valuation model reflects a 5-year projected average operating margin of 8.6%, which is above FedEx’s trailing 3-year average. Beyond year 5, we assume free cash flow will grow at an annual rate of 5.3% for the next 15 years and 3% in perpetuity. For FedEx, we use a 8.9% weighted average cost of capital to discount future free cash flows.

Image Source: Valuentum Image Source: Valuentum

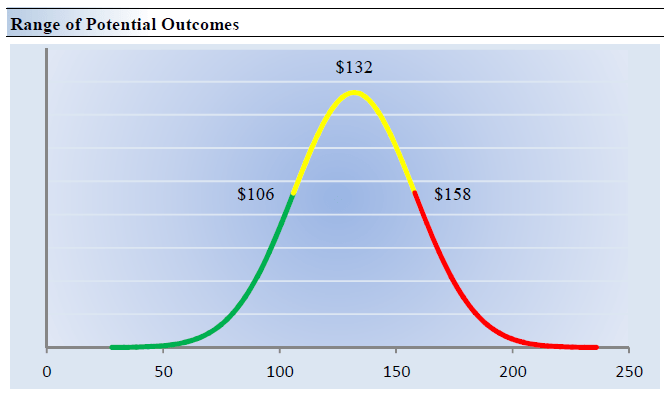

FedEx’s Margin of Safety Analysis

Image Source: Valuentum

Our discounted cash flow process values each company on the basis of the present value of all future free cash flows. Although we estimate FedEx’s fair value at about $293 per share, every company has a range of probable fair values that’s created by the uncertainty of key valuation drivers (like future revenue or earnings, for example). After all, if the future were known with certainty, we wouldn’t see much volatility in the markets as stocks would trade precisely at their known fair values.

Our ValueRisk rating sets the margin of safety or the fair value range we assign to each stock. In the graph above, we show this probable range of fair values for FedEx. We think the firm is attractive below $234 per share (the green line), but quite expensive above $352 per share (the red line). The prices that fall along the yellow line, which includes our fair value estimate, represent a reasonable valuation for the firm, in our opinion.

Concluding Thoughts

FedEx provides customers and businesses worldwide with a broad portfolio of transportation, e-commerce and business services. The firm’s pricing strength supports its outlook, as does the proliferation of e-commerce and the growing global middle class. FedEx is investing heavily in automation and route optimization technology to support its FedEx Ground division while continuing to integrate its air freight business in Europe, activities that should support its financial performance over the long haul by generating meaningful operating efficiencies. We expect management will push through decent dividend increases over the coming fiscal years.

FedEx’s business requires substantial capital investments (the firm’s capital expenditures as a percentage of its revenues have come in around 7% in recent fiscal years), but it typically generates significant amounts of operating cash flow. The company aims to offset inflationary pressures, such as rising labor and fuel expenses, with its pricing power though it will take time for pricing increases to be fully reflected in its financial performance. FedEx has a sizable net debt load which weighs negatively on its dividend health, in our view, though the company generally maintains a nice total cash position on hand to manage its various near term financing needs. We like shares.

This article or report and any links within are for information purposes only and should not be considered a solicitation to buy or sell any security. Valuentum is not responsible for any errors or omissions or for results obtained from the use of this article and accepts no liability for how readers may choose to utilize the content. Assumptions, opinions, and estimates are based on our judgment as of the date of the article and are subject to change without notice.

Be the first to comment