vandervliet93

At the outset of the COVID pandemic, shipping stocks were all the rage. After all, if no one can leave their house, most goods will be shipped. Like so many pandemic darling stories, however, this one fizzled out as well.

Shipping stocks have been very weak this year, and FedEx (NYSE:FDX) certainly counts itself among the weak ones. The last time I covered FedEx, I was less than enthused about its prospects. That was two and half years ago, however, and much has changed. What hasn’t changed is that I don’t see a lot of reasons to buy this stock.

The company posted second quarter earnings, and the report isn’t all that inspiring given the massive reductions in revenue and earnings estimates in recent months. In addition, guidance looking forward was weak, and the company is cutting capex. In my experience, companies pretty much always cut capex from a position of weakness, so that’s a red flag for me. At any rate, let’s take a look at the technical setup, the report itself, and the outlook for FedEx going forward.

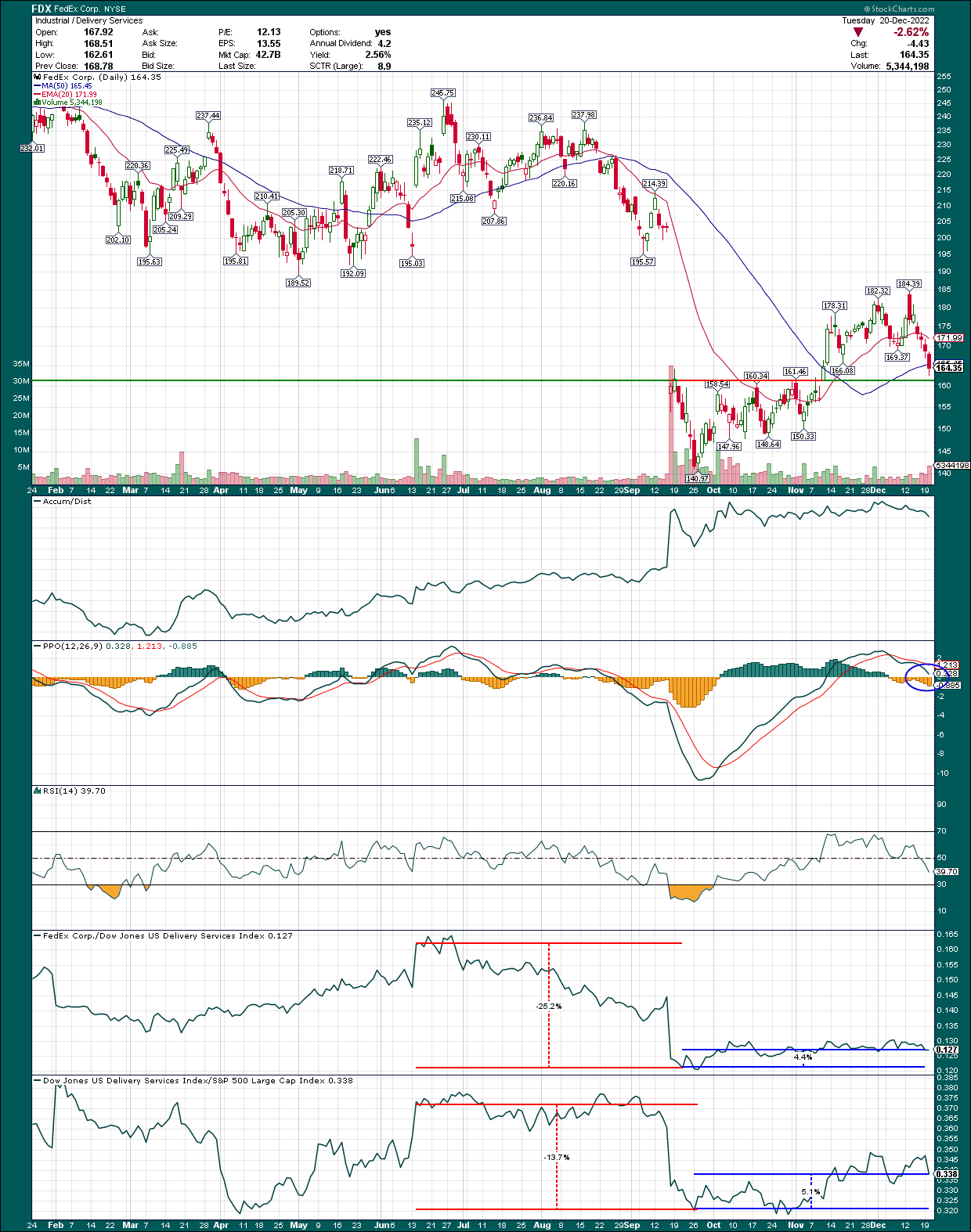

Showdown at $162

FedEx took a huge nosedive in September on a dud of an earnings report. The stock went from $204 to $140 in the space of a handful of trading days, creating an extremely oversold stock that did eventually bounce. There was a zigzagging consolidation until early November, when FedEx gapped above its consolidation range and ran to $184. The stock pulled back sharply in recent days and that has put it precariously close to the major, critical support level of $162.

When a stock breaks out, and then returns to the breakout level, it is critical the breakout level holds. Otherwise, the breakout is negated and what almost always follows is a big selloff. FedEx is indicated ~$5 higher as I write this, but we’ll see how regular trading goes on Wednesday. Point being that if you want to own this stock, the closer it is to $162, the better the risk/reward. If it falls below that level, look out below.

StockCharts

Now, we can see FedEx has already failed the 20-day exponential moving average, as well as the 50-day simple moving average, the former of which is downward sloping at this point. That’s not a good sign, and neither is the fact that the prior relative low of $169 was blown right through in the past few days.

On the plus side, the accumulation/distribution line looks great, indicating there are dip-buyers afoot. In addition, the PPO is in bullish territory and testing the centerline. Those are good things, and indicators that I follow very closely, but they are secondary to price action. In other words, if FedEx fails $162, those indicators aren’t going to help and the stock will almost certainly begin a larger selloff.

The bottom two panels show relative strength, and in the first one, we can see that FedEx underperformed its peers by 25% between June and September, while the group underperformed the S&P 500 by a further 14%. It’s gotten slightly better since then, with outperformance of 4% and 5%, respectively, but FedEx and other shipping stocks continue to have a hard time attracting investor capital.

The bottom line on the chart is that $162 is the line in the sand. If it holds, you can own this for a trade. If it doesn’t, it’s a good short candidate back down to $150 at least, which is the relative low before the breakout. The Wednesday trading session is critical given the stock’s proximity to this level.

Another so-so quarter from FedEx

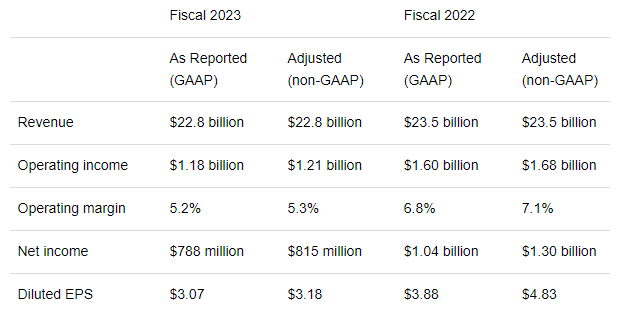

FedEx shares haven’t been sold off constantly this year for no reason; the company’s business continues to deteriorate. The report showed adjusted EPS of $3.18, which was 36 cents ahead of estimates. However, revenue was off 3% year-over-year to $22.8 billion, and missed expectations by $920 million. That’s a big revenue miss, and that’s after estimates were cut and cut and cut in the months heading into the report. In other words, FedEx had a lowered bar, and missed it anyway. The company said the Express segment was the cause of the weakness, primarily. However, all three segments saw lower shipping volumes. The demand simply isn’t there, and that’s a big worry.

The company noted it repurchased 7.9 million shares under its accelerated share repurchase program, or nearly 3% of the float. That’s a strong showing from the buyback, and it is not a moment too early given the company’s weakness.

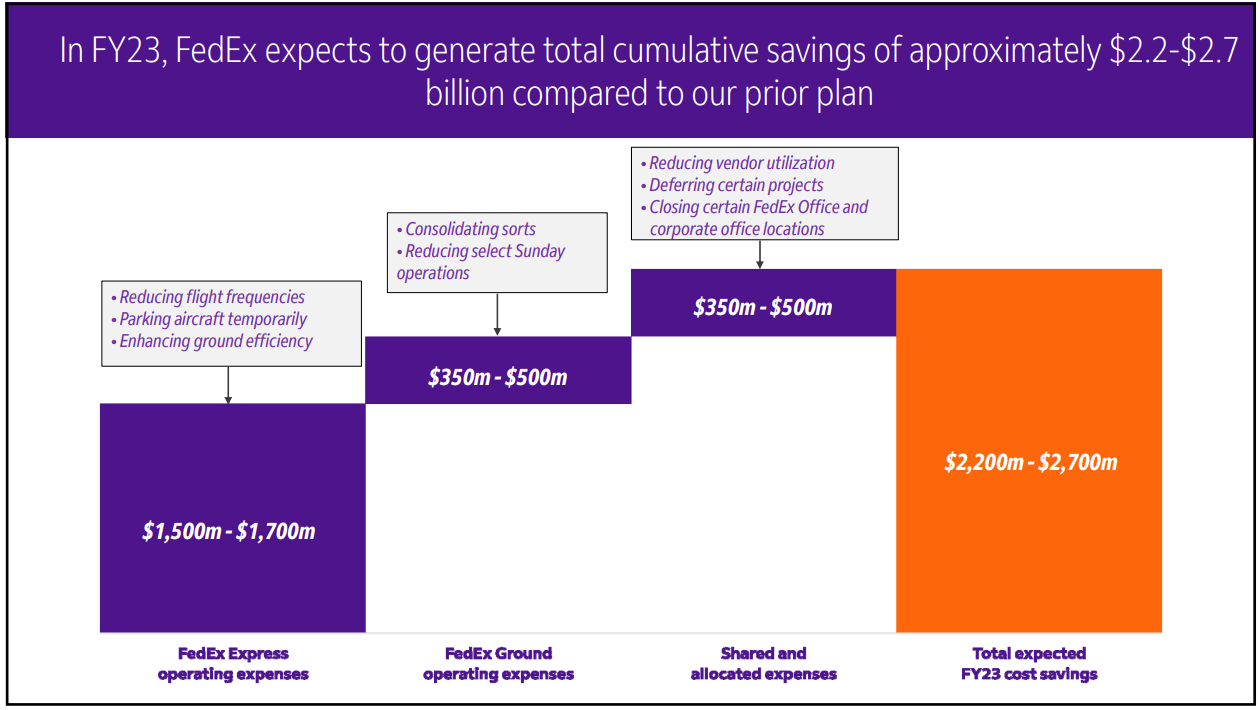

I mentioned that companies that cut capex do so from a position of weakness, and the same is true for cost savings. Generally, companies that are laser focused on cost cutting are doing so because margins and/or revenue are declining. On the other side of the coin, think of a hot tech startup; they generally don’t care how much they spend on capex because it’s supporting growth. Companies that cut costs and capex are very worried about growth, and are downsizing to meet lower demand. It is my belief that is where we find FedEx today.

Investor presentation

This slide from a recent presentation shows the company is serious about this effort, and they see meaningful cost reductions on the horizon. If these come to fruition, it should help boost flagging margins. But keep in mind, there is no way to cut one’s way to growth; these are stop-gap measures to preserve profitability. Again, done from a position of weakness.

FedEx guided for $13.00 to $14.00 in EPS for this year, short of the $14.12 mark of analysts heading into the report. That’s a shortfall of up to 8% (at the bottom of $13.00), so this is not an insignificant reduction to earnings. In addition, capex is now expected to be $5.9 billion, down from $6.3 billion.

Seeking Alpha

I want to go back to margins, because FedEx has a big problem there. It’s why the company is focusing so heavily on saving costs, because it knows its margins have plummeted in recent quarters. If we look above, we can see the year-ago period saw adjusted operating margins of 7.1%, whereas this quarter was 5.3%. That’s a 25% reduction in profitability, and it’s why net income and EPS plummeted. Cost savings will help, but so long as revenue is weak, FedEx is going to have a hard time raising that number.

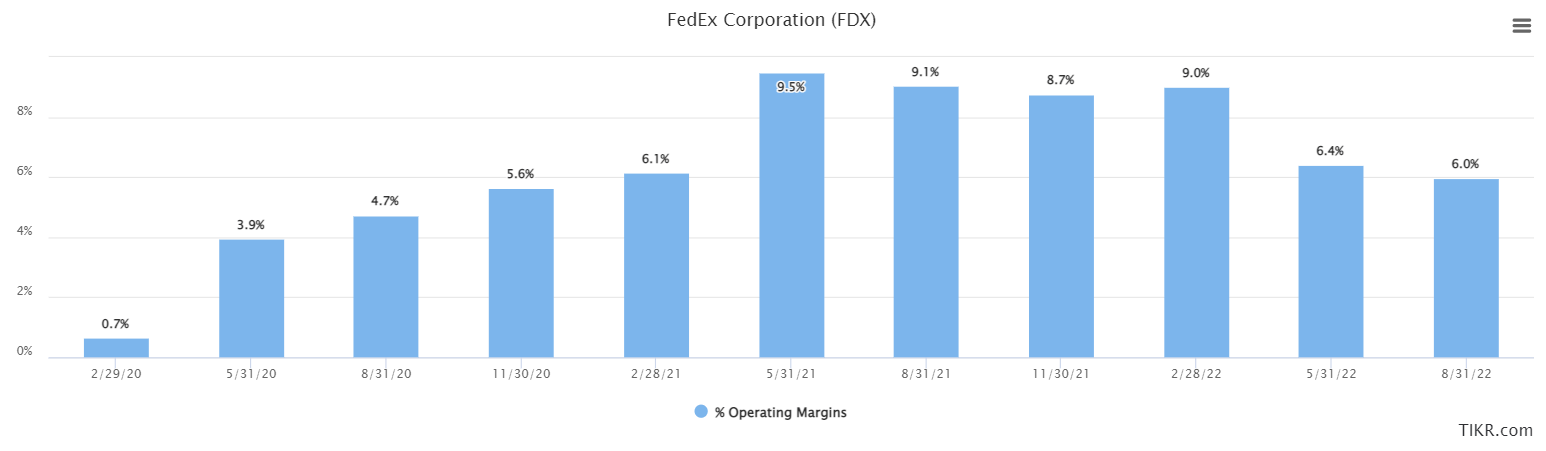

TIKR

We can see the pandemic boom very clearly on this chart of operating margin, and the fact that those days are long gone. The company is back to below-average operating margins today, and when combined with weak revenue, I’m really not sure why I’d want to own this stock.

Looking forward

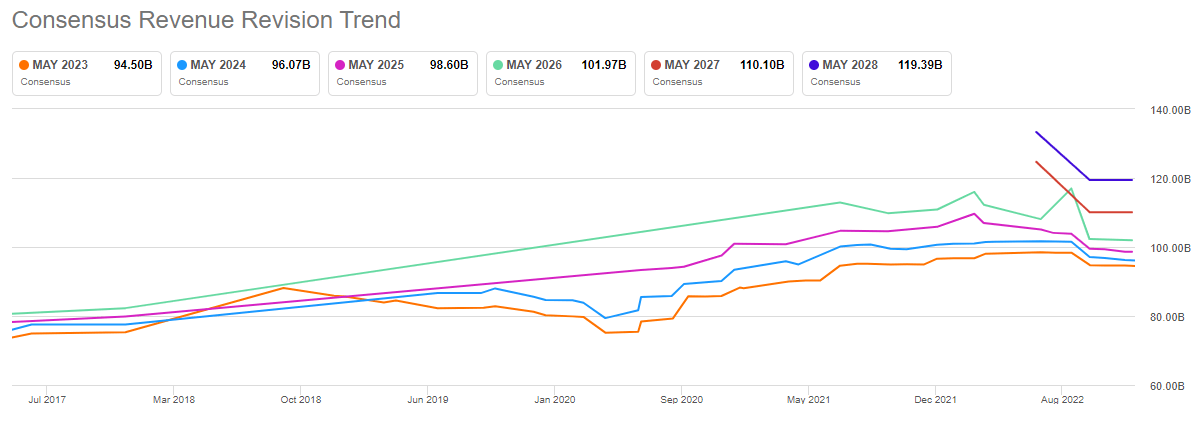

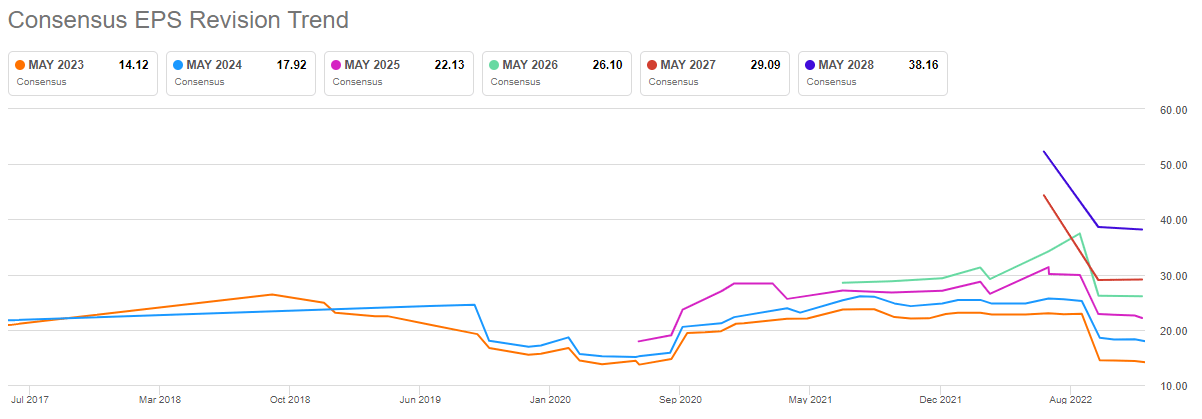

I mentioned above that estimates had been slashed heading into the report, and below, we can see the extent of the damage. Keep in mind also that with the guidance cut, we’re almost certain to see further cuts from analysts as FedEx continues to underperform.

Seeking Alpha

Out of 27 EPS revisions in the past three months, 23 were down. On revenue, it was 18 out of 24. The analyst community is/was quite pessimistic on FedEx’s ability to execute, and with the report now out in the open, we know why.

Revenue revisions have been pretty tame, as we can see the lines turned down over the summer of this year.

Seeking Alpha

However, like I said above, the cuts are almost certainly not done when literally every segment is posting lower package volumes.

The story with EPS is much worse, and it’s because margins have plummeted along with slightly weaker revenue.

Seeking Alpha

With the guidance cut, these lines are coming down, too. Interestingly, FedEx’s EPS estimate for this year is likely to make a full roundtrip back to the pandemic lows from 2020. If you’re buying this stock based upon estimated earnings in 2023/2024/2025, and those lines continue plummeting, you have to ask yourself what exactly you’re valuing the stock with. Stocks with ever-declining estimates are difficult to value because you have to guess where the bottom is. I don’t know where the bottom is with FedEx, but Q2 results suggest wherever it is, it’s lower than where we are today.

Let’s value FDX stock

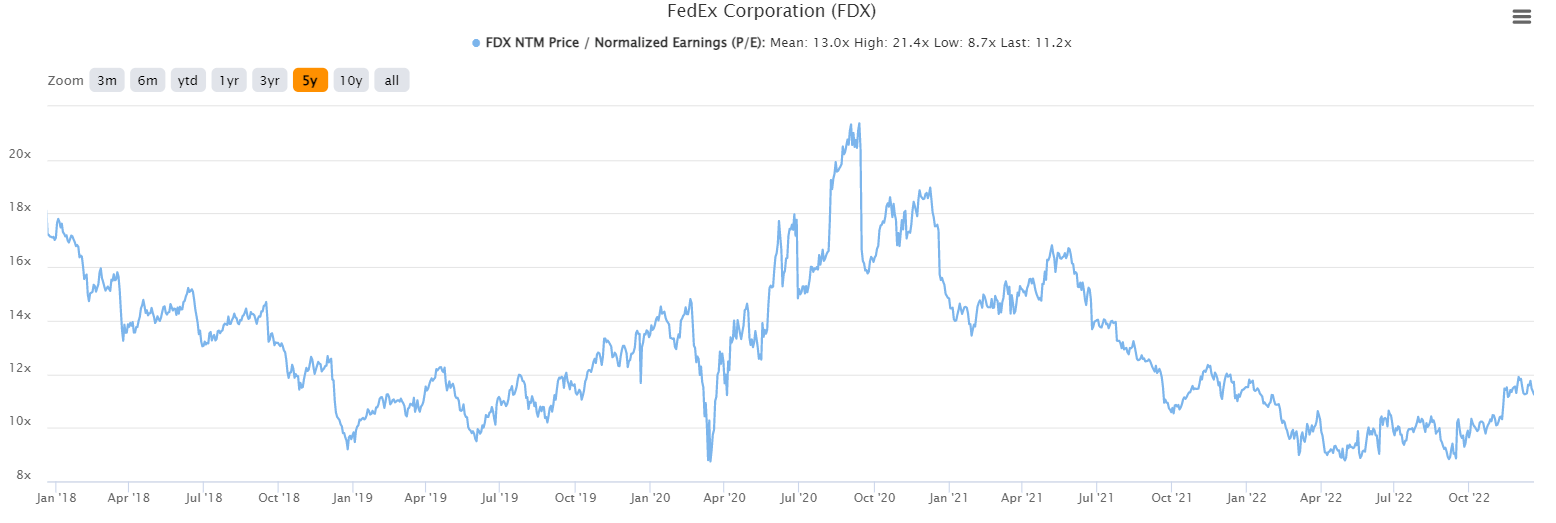

I just provided a cautionary tale on valuing a stock with falling EPS estimates, so we’ll need to take the below with a proverbial grain of salt. At any rate, what we have is historical data on forward P/E ratios the stock has traded with, and it’s quite instructive.

TIKR

Shares were at 11.2X forward earnings before the report, but as we know, the forward earnings portion of that equation is going to come down. Thus, if we assume a 5% reduction in earnings (the midpoint of guidance), we’re looking at more like 12 times earnings.

The stock’s average forward P/E ratio during the last five years is 13X, so it’s slightly below that. Does that make it cheap? Given that volumes are falling and margins are in free fall, the stock should have a below-average valuation. With it near the historical average, I would say not only is it not cheap, it might be slightly expensive. In fact, I could see FedEx easily testing its valuation lows of 10X earnings if things don’t pick up quickly.

The bottom line here is that there is a setup in place on the chart for a bounce from the $162 level. Will it happen? I suspect we’ll find out very shortly.

Longer-term, I still think FedEx is struggling, and the fact is that I don’t want to own any company that has constant downward EPS and revenue revisions, and one that is much more focused on cutting capex and operating costs than figuring out its growth issues. That doesn’t fit my style, but I also recognize that is exactly what value investors look for. For me, an investor’s capital could be better used in a very long list of places besides FedEx, so I’m staying away for now.

I will look to potentially short the stock if it fails the $162 level on a closing basis, but for now I’m neutral on it.

Be the first to comment