Douglas Rissing

The best course I took in graduate school was an accounting class called “Problems in Financial Reporting” with Professor Peter Knutson. My take-away from the class was to not follow what they say, but to look for what they don’t say.

I was reminded of this when I read last week’s press release from the Fed on their results for 2022:

“The Federal Reserve Act requires Reserve Banks to remit excess earnings to the U.S. Treasury after providing for operating costs, payments of dividends, and any amount necessary to maintain surplus. During a period when earnings are not sufficient to provide for those costs, a deferred asset is recorded. The deferred asset is the amount of net earnings the Reserve Banks will need to realize before their remittances to the U.S. Treasury resume.”

What wasn’t said in the press release, is that the deferred asset is an accounting gimmick which allows the Fed to hide their operating losses on their balance sheet as a negative liability. Nowhere in the statement do they mention operating losses, but operating losses they do have!

For the first time in 107 years, the Fed recorded an operating loss in the fourth quarter of 2022.

The operating loss amounts to just over $15 billion for the quarter.

The loss came about because the Fed made a fundamental error during their 14-year period of Quantitative Easing (QE) of buying fixed rate long term assets (US Treasury bonds and mortgage-backed securities) and funding them with variable rate short term liabilities. Any basic risk management course would teach that such an asset-liability mismatch would expose the entity to significant interest rate risk when rates rose.

Lo and behold, this past year when inflation spiked to a 40-year-high, the Fed did what their mandate requires them to do, which is to raise interest rates to combat the inflation.

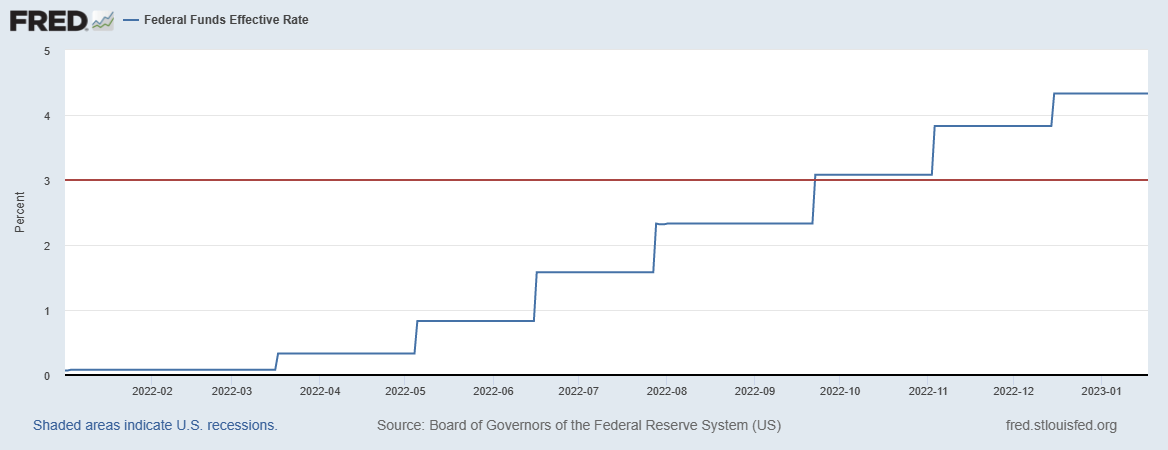

The Fed raised rates seven times in 2022 increasing the Fed Funds Rate by a total of 425 basis points from a range of 0.0-0.25% to a range of 4.25-4.5 %.

Federal Reserve

As was totally predictable, the rise in short rates due to the Fed tightening created a negative net interest margin.

With $8.5 trillion in fixed rate bonds earning 2.0%, the cost of the Fed’s variable rate liabilities, namely $5.7 trillion in bank reserves and reverse repurchase agreements, began rising. The break-even rate is roughly 3.0%, which was exceeded when the Fed raised the Fed Funds rate to 3.0-3.25% on September 21, 2022, as can be seen in the above chart.

There have been two subsequent rate hikes bringing the current Fed Funds rate to 4.25-4.5%.

There is much talk in the market about the Fed’s next move at their February 1st meeting, as to whether another 50 basis hike will occur or if it will be trimmed to 25 basis points. Market expectations are now favoring a slimmer 25 basis point hike.

Nonetheless, the net interest margin will remain negative, and the Fed will continue to book operating losses until the Fed Funds rate drops below the 3.0% mark. No one is expecting that to happen any time soon.

Summary of 2022 Results

Net Income for the year fell to $58.4 billion from $107.9 billion in 2021, a 45.9% decline.

The main reason for this drop in income was the significant increase in the cost of their variable rate liabilities. While total interest income rose to $170 billion from $122.4 billion (a 38.9% gain), interest expense spiked dramatically to $102.4 billion from $5.7 billion, a whopping eighteenfold increase.

In the chart below, we can see how the Fed’s earnings fell each quarter as the Fed Funds rate was rising.

Federal Reserve

Weekly Fed Losses

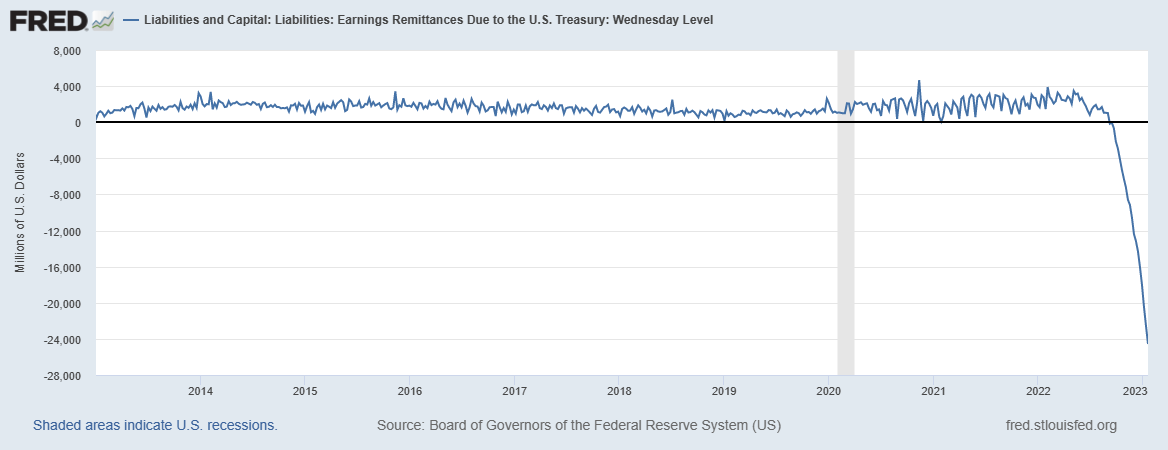

The Fed is good at providing data, and one of their very useful statistical releases is the H.1.4 weekly report titled “Factors Affecting Reserve Balances.” Buried deep in this document is an item called “Earnings Remittances Due to the U.S. Treasury.” This is the deferred asset account referenced in the Fed’s Press Release.

In the below chart we can see that the account turned negative for the first time ever during the week of September 21, 2022 when the Fed Funds rate rose above the break-even point for Fed earnings. It has been growing more negative each week since then.

Federal Reserve

As of 1/18/23 the deferred asset account has a cumulative balance of -$24 billion.

Currently, the Fed is losing $2.2 billion per week. If rates do not change, this translates to an annual loss of $114 billion. If the Fed keeps tightening, as expected, the weekly losses will only grow.

Federal Reserve

To put this in perspective, the Fed has total capital of $42 billion. The projected losses for 2023 are almost three times the Fed’s total capital.

While placing their operating losses in a deferred asset account on their balance sheet does not affect their capital, this is strictly an accounting maneuver. The deferred asset account will continue to increase for some time.

The Fed acknowledged as much in a policy note dated July 15, 2022. They anticipated that net earnings would turn negative, but the speed and magnitude of the losses has exceeded even their most pessimistic assumptions.

We project that the deferred asset account will grow to at least $240 billion over the next two years.

Federal Reserve and Author

As stated in their press release, the Fed is required to remit all excess earnings to the Treasury. Over the past 20 years, they have averaged sending $64 billion per year back to the Treasury. These earnings have been used to offset the government’s fiscal deficit. As the Fed is now generating losses, it is the taxpayers who will bear the brunt of the Fed’s monetary policy decisions. Under the Fed’s worst-case scenario, they expect the deferred asset account to remain until 2030.

Unrealized SOMA Portfolio Losses

In addition to the net operating losses, the Fed is also carrying a huge unrealized loss in their SOMA portfolio.

The Fed records their asset purchases in their SOMA portfolio at amortized cost. In a footnote on their financial statements, they list the fair value, or market value, of their holdings. The entire SOMA portfolio was purchased when interest rates were significantly lower than they are today, meaning that every single security in the SOMA portfolio was purchased at a higher price than its market value today.

The total unrealized loss of the SOMA portfolio at year end is $1.1 trillion.

These market losses will only be recognized if the securities are sold. Presently, the Fed is reducing their portfolio as securities mature, so they won’t have to recognize any losses.

Federal Reserve

Policy Normalization is Going Slowly

The Fed has two main tools for tightening monetary policy to control inflation. The first is to increase the interest rate they pay on bank reserves, and we’ve already discussed their actions on that front. Their second tool is to reduce the stock of bank reserves, and this is done through what is known as Quantitative Tightening (QT).

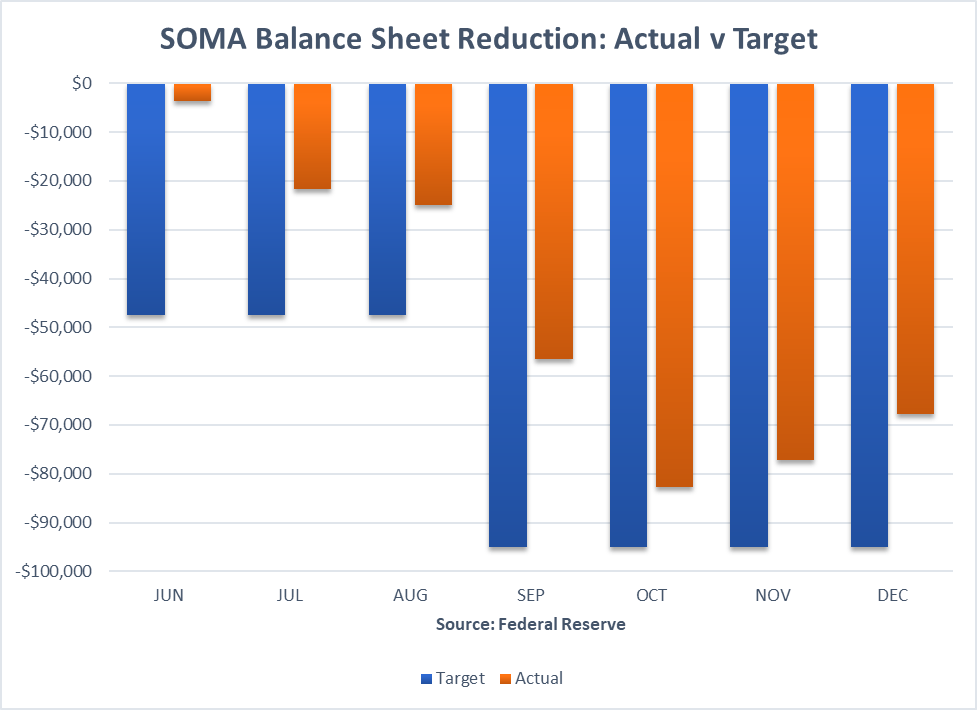

The goal of Policy Normalization through QT is to shrink the Fed’s balance sheet. The normalization program was gradually phased in over 3 months. Beginning in June 2022 the Fed allowed maturity roll-offs of $47.5 billion per month, then full implementation of $95 billion per month of roll-offs was started in September 2022.

We’ve had seven full months of QT to date, with the results falling short of expectations.

Federal Reserve

The Fed has not hit their target yet in any month, and the total reduction to date is only $334 billion of a projected $522 billion, or 64% of target.

What This All Means

The Fed insists that “while the rising interest rates have ancillary effects for the Federal Reserve’s income and the unrealized position of the SOMA portfolio, none of these effects impair the Fed’s ability to conduct monetary policy or to fulfill any of its other responsibilities.”

They have to say this.

The operating losses and unrealized losses, however, are not insignificant and could have major implications.

First, when it becomes more widely known that the Fed is losing money, it could have political implications. When congress begins to focus on the Fed losing money for the first time in 107 years, thereby costing taxpayers billions of dollars, they may pressure the administration to institute controls to limit the Fed’s independence. This may become particularly contentious as discussions heat up in the ensuing months over raising the debt ceiling tied to reducing the deficit.

The second area of concern is market confidence. In many ways, the stability of our financial system is due to its confidence that the central bank is strong and in control. Continued weakness may erode that confidence. Again, this may become more significant over the brinkmanship of raising the debt ceiling.

Finally, as losses continue to mount, the Fed may be forced to create new reserves to meet their obligations. This would be inflationary and would exacerbate the problem they are trying to solve.

As Professor Knutson taught, to understand an institution, look for what they’re not telling you.

The Federal Reserve is awash with losses for the foreseeable future.

Be the first to comment