DNY59

Fed Rate Hikes: Is Too Little Enough?

Markets are almost crazed with the desire to put a stop to central bank tightening. In Europe a survey of inflation expectations shifted down by less than half a percentage point and markets are rife with predictions that the ECB is going to have to slow its pace of tightening…because of this. The ECB interest rate lags inflation badly already, what difference does one-half of one percentage point on expectations make when inflation is already so far over its targeted pace? What are people thinking?

In the U.S., the CPI has decelerated 2.6 percentage points from its peak year-on-year pace, with the core rate decelerating by just 0.7 percentage points from its peak pace. Yet markets think the Fed – that just reduced its rate hike increment to 50bp from 75bp – needs to downshift again. Does it?

These questions spring eternal… The answers are mired in ideology, dogma, politics, and guesswork, with a sprinkling of “science.” There is no truth in the answer, only some references to history, some forecasts, and some wishful thinking. In truth, it’s not much to go on. But all economists have their opinions on these matters, and they take their musing from the various buckets of science, ideology, and guess-work. So, who do you trust?

That question is also hard to answer and is not just pertinent to monetary policy. In many fields these days – at least in America – we have a hard time getting to truth and objectivity on many issues. Politics have poisoned all the wells, there is no truth. There is opinion.

However, on the issue of monetary policy, I believe there are some standards, some pillars, some benchmarks, that can give support to opinion.

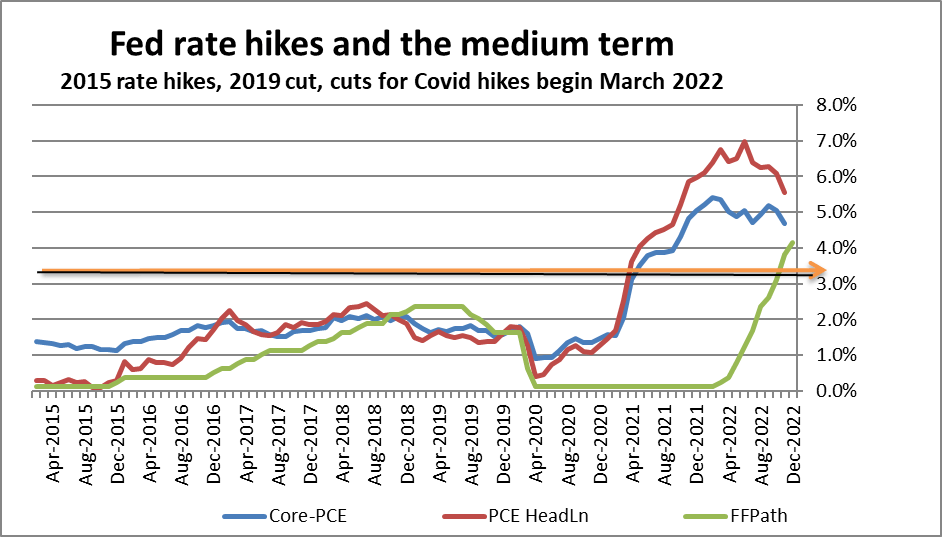

Inflation Vs fed funds rate levels (Haver Analytics and FAO Economics)

My take on it all is that the Fed messed up for various reasons that we can argue about (but won’t here). Having made bad policy that let inflation rise and – that let that rise go on for about 12-months – without taking any action at all – the Fed was “forced” to engage in accelerated tightening. However, markets have forgotten about the Fed’s long delay in tightening and only want to look at the rapid rate increases and use them as a rationale to slow the Fed down. But with year-over-year inflation at 6.4% and the core pace at 5.7% and the Fed funds rate lower than that, the rationale for slowing down escapes me.

This cycle has contained the 13 lowest negative real fed funds rates since mid-1960, at least. Those rates imparted a great deal of stimulus, on top of the spurt in money supply, the Fed balance sheet expansion, and the fiscal thrust. So, the recent rate hikes, which still do not put the Fed funds rate above the inflation rate, only serve to make monetary policy less stimulative – not contractionary. As a counterpoint, I’ll admit that we also now have the slowest growth in M2 since the mid-1960s, but that, of course, follows a ballooning in money growth. The ratio of money to GDP is still high. I didn’t say this was going to be easy, it is complicated. There are cross currents.

CPI acceleration by major category (Haver Analytics and FAO Economics )

Trends are not as tame as market reactions would seem to imply

Not only are assessments of monetary policy mired in ideology, politics, and guesswork, but the pertinent facts are of an uneven nature. If monetary policy works with a lag, should it be concerned with the stimulus from the past deeply negative real fed funds rates and the money supply ballooning, or the more recent return of real rates to a more modest negative posture and the sharp slowing in money growth? If statistical work were reliable enough, it could tell us but so many of these events are piled one on a-top-of-the-other or on the heels of the other. Disentangling the effects is still guess work.

In the end, the policy choice is an act of judgement and of risk management. After creating the inflation bubble or failing to act to deflate it quickly, I would expect the Fed to be more aggressive and to make sure it stops inflation since it has emerged. Markets are less concerned with this and simply want lower rates. But the Fed already has put markets on notice about how predictive market rallies, looking for future easing, may be self-defeating. They may cause Fed policy to be tighter if markets significantly ease financial conditions ahead of the Fed’s own policy steps.

Things have gotten very complicated. We have policy, forward guidance, markets watching and reacting to their perceptions of the central bank’s expressed reaction function, and we have feedback effects to Fed policy from all that.

Headline inflation is falling 3 ½ to 4 times faster than core inflation. China is no longer touting Zero Covid. The potential for oil price pressure to return is there and falling oil prices have been the major factor behind inflation falling – so far. Service-sector inflation remains stubborn. I don’t know what markets are looking at to handicap their reactions beyond weighing their own wishes. Markets want the endless financial market carnage to stop. As far as I can see, the data, the trends, the analysis, the history, all are against what the markets are poised to do in 2023. We can’t yet be sure where the Fed stands because its members’ express a lot of differing views. Is the Fed worried about its reputation after it let inflation loose? Even Pandora closed the box in time to keep hope from escaping. Is hope all the Fed has or does it still have any toughness?

This is what we are about to find out. I continue to fear a 1970s-type result, a modest recession because monetary policy does not stay the course to push inflation all the way back down. For now, no FOMC member looks for any Fed rate cuts this year, but that is exactly what markets look for, a 2023 rate cut. And they are priced for it. Somebody is going to be disappointed.

All this will come to a head soon. I urge investors to look clearly at the data and trends. Apart from the part linked to oil, inflation is not falling fast. Inflation is high- too high. The Fed has more work to do. At this rate, a mild recession is not going to get the job done. It will leave us in a 1970s situation with a mild recession, some reduction in inflation….but not enough reduction. The recession will end with more work to do. But central banks do not hike rates early in a recovery…

We have seen the market and Fed go head-to-head before. It is never pretty. For now, it is not so much a battle for rate levels as it is a battle for the heart and soul of the Fed. Will the Fed give in to complacency and cast its fate to the wind? Will it be willing to bet inflation will continue to slide without its continued strong action? Or will the Fed do its job, and become more concerned with risk management and continue to guard against insufficient inflation declines by staying the course with rate hikes? That’s what we are waiting to find out. It should be clear by now that too-little is not enough regardless of what markets want. But in the end the Fed has a dual mandate and lately it has been emphasizing the employment objective. What will it do? How will it act when the unemployment rate begins to rise? That is still an unknown, but it is the reason for my unease.

Be the first to comment