Editor’s note: Seeking Alpha is proud to welcome Principal Investor as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Marina_Skoropadskaya

Thesis

Fathom (NYSE:FATH) is a tech-agnostic digital manufacturing platform addressing the low volume/high mix TAM of $25B, with a broad range of solutions across 3D printing, injection molding, CNC, and sheet metal fabrication. The firm is EBITDA profitable and positioned to benefit from secular trends in manufacturing, including

- a shift from in-house manufacturing to outsourced solutions driving lower capex for customers;

- quick turnaround for high-quality products requiring customers to hold less inventory;

- interactive software solutions and quick pricing quote.

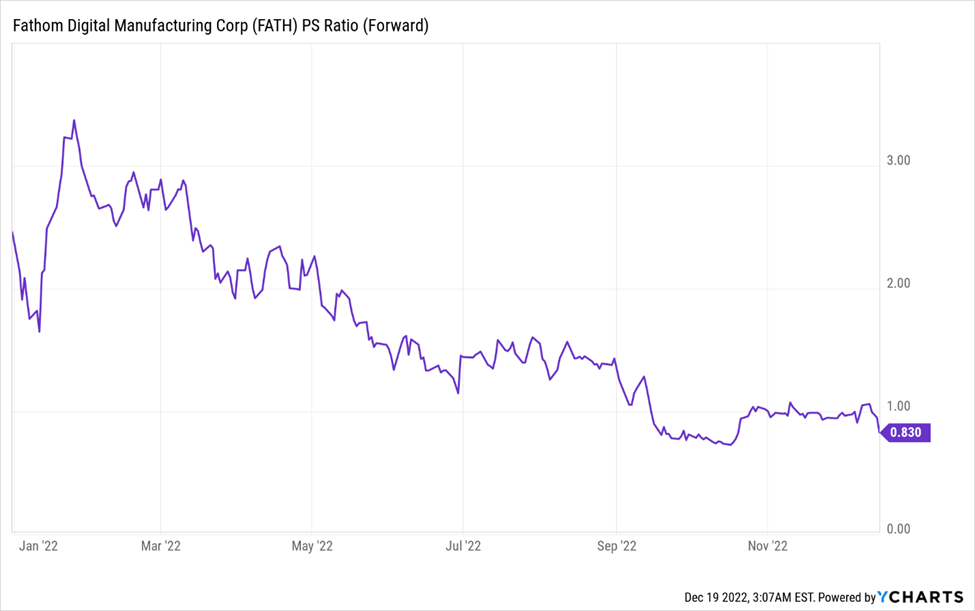

FATH is currently trading at a forward PS ratio of 0.83x sales compared to the 1.23x sector median and I believe the stock should trade higher owing to the company’s top-line potential growth and margin expansion.

Company Overview

Operating in North America, Fathom Digital Manufacturing Corporation provides digital manufacturing services to over 3K customers. The firm is tech agnostic and provides traditional manufacturing methods along with emerging technologies such as 3D printing. The firm focuses on low to mid-volume manufacturing and has 12 locations across the states with customers across industrial, medical, aerospace, auto, and consumer end markets.

Why do I like FATH?

Fathom’s Growth Strategy addresses a large TAM

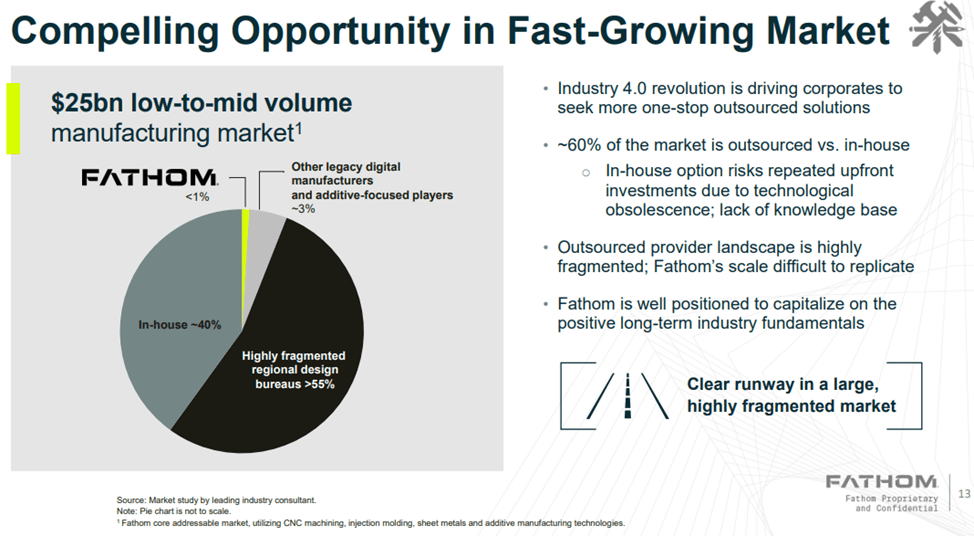

As part of the $25 billion low-to-mid volume manufacturing market involving these technologies, Fathom approximates that 40% of production is handled in-house, 55% is delegated to regional design services bureaus, and 5% is serviced by legacy digital manufacturers. The shortcoming of utilizing regional design services, which currently hold the largest market share, is that they are specialized in their offerings and not well positioned to scale production due to labor and capacity constraints. Similarly, legacy manufacturers experience constraints on the flexibility side and inhouse manufacturers have capacity constraints. A part of Fathom’s key growth strategy is taking market share from these areas, which they believe is an easy value add for companies looking to outsource production due to their increased flexibility and capacity offerings.

Thus far, FATH has pointed its attention toward enterprise level corporate customers, leveraging their ability to tackle a wide range of manufacturing complexities and scale production quickly. In the near term, the existing customers will continue to be the focus as the company increases penetration across departments and lines of production (called the “land and expand” model). Over time, the company has a vision to expand the customer base to include other enterprise level corporate companies while retaining legacy customers by maintaining strong relationships. It also plans to grow additive manufacturing capabilities along with software and digital capabilities via organic growth or acquisition.

Currently sitting at 12 sites, I believe Fathom is poised to gain market share given speed with its growth strategy and optimization plans in place and as FCF rebounds in FY23 (FY22 cashflow was affected by restructuring and one-off charges), I think the firm will continue to execute on new site acquisitions.

FATH is exposed to a large TAM (company presentation)

M&A in a highly fragmented space

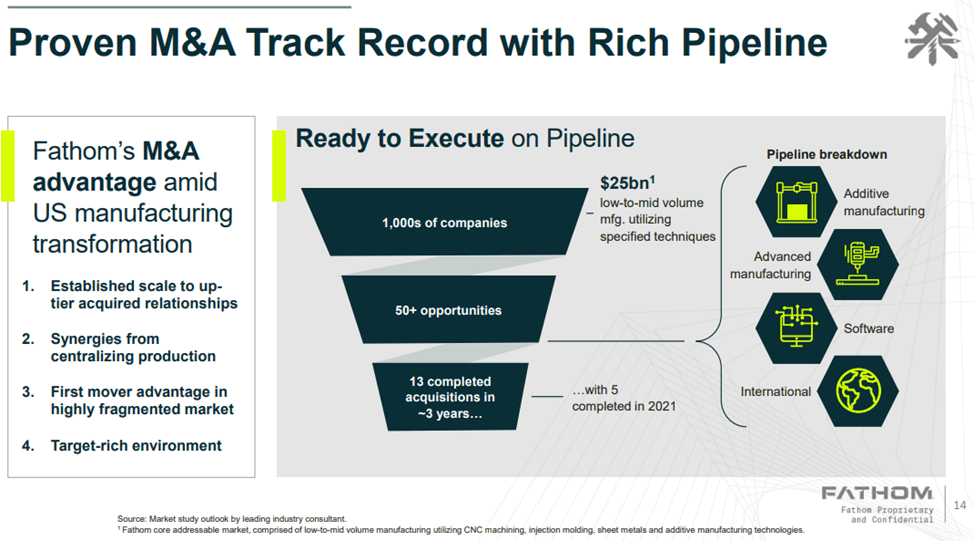

Fathom has continued to make acquisitions in recent years as the management looks to expand the company’s capabilities and services across sheet metal fabrication, injection molding, and CNC machining. The firm also regularly expands its portfolio of 3D printing capabilities. M&A pipeline has 50+ targeted opportunities with the potential to expand across thousands of companies. I believe it’s likely that the firm will continue to actively pursue M&A, adding new tech but also driving scale and incremental leverage, recognizing synergies post-close of acquisitions, rationalizing locations, and consolidating locations to drive scale benefits. Firm plans also include adding new services and cross-selling existing services to newly acquired client bases.

FATH’s pipeline breakdown (company presentation)

Financial Outlook

Revenue Outlook

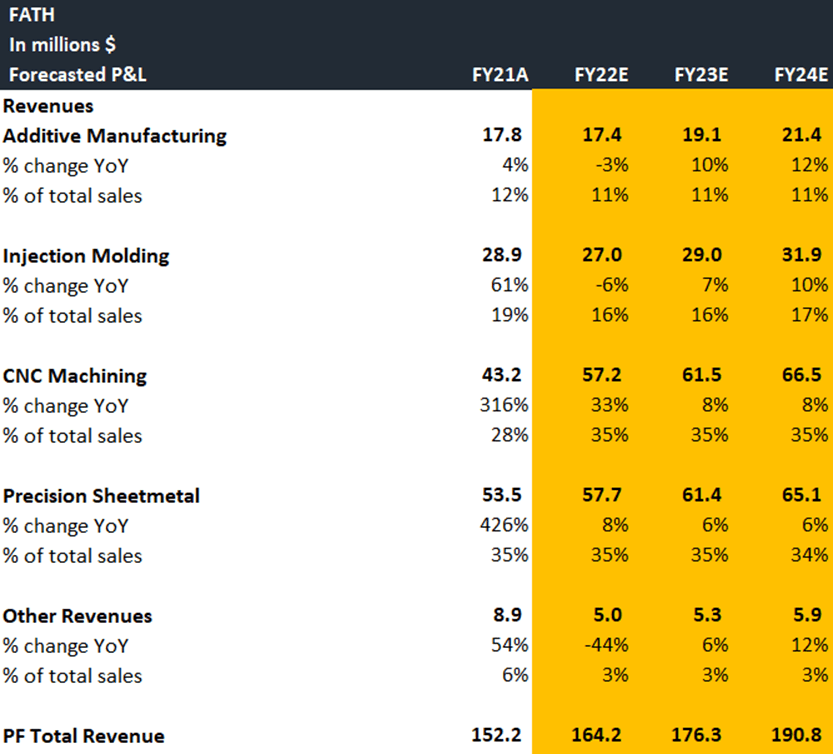

Fathom’s revenue segments are split by technology: Additive, Injection molding, CNC Machining, Precision Sheetmetal, and Other, which includes finishing work and other services. Revenues are typically recognized when performance obligation has been satisfied. I am looking for ~8% growth in FY22, and ~7.4% in FY23 (in line with the historical growth rate), with relative strength in Additive followed by CNC, Injection molding, Sheetmetal, and other. I believe longer term that the firm can grow high single digits top-line on scale as it expands market share in a fragmented market and expands services across segments and verticals.

FATH’s forecasted revenue estimates (my estimates)

Margins and Earnings Outlook

COGs consist of depreciation, raw materials costs, employee costs, and overhead. Near term rising costs of materials weighing on margins coupled with product mix. I think it’s likely that FATHOM will continue to actively pursue M&A, adding new tech but also driving scale and incremental leverage, recognizing synergies post close of acquisitions, rationalizing locations and consolidating locations to drive scale benefits. Firm plans also include adding new services and cross selling existing services to new acquired client bases.

I expect gross margins to grind higher with benefits of scale to 40%+ (from current ∼37% range). SG&A has seen some volatility near term on acquisition integration costs, public company costs, stock comp, and IT Infrastructure consolidation, though I believe the firm is optimizing costs to focus on profitability. I expect SG&A to become less % of sales over time as top-line ramps and see more fixed cost leverage benefits.

Valuation

FATH is currently trading at a forward PS ratio of 0.83x sales compared to the 1.23x sector median. I think the stock should trade at a higher multiple ahead of OEM 3D printing peers owing to top-line potential and margin expansion. The 3D printing space has seen material pressures on valuation multiples this year as profits come into focus, and the top line has seen some softer demand trends emerging. I expect some near-term headwinds, particularly in injection molding; however, longer-term, I believe the diversified product mix, sticky consumer base, and strong margin profile with a credible path toward mid-20% EBITDA and resulting high FCF generation. For my target price calculation, I have assumed a PS multiple of 1.5x for FY23 and $176.3 in revenue for the year which results in a target price of $4.03.

FATH is trading at a PS ratio of 0.83 (ycharts)

Risks

A highly fragmented, quickly emerging sector sees competitive pressures

With the backdrop of strong industry fundamentals and a solid 20%+ historic CAGR, 3D printing has especially been in the spotlight as a solution in response to pandemic-induced supply chain headwinds. There has been a burst in players entering this highly fragmented industry with few established legacy firms, and as a result, there is some level of volatility in market share and competitive pressures. Market share is dependent upon innovation and keeping pace with technological change, and my price target includes an embedded expectation that Fathom will be able to remain competitive in the space, which may not be the case.

Exposed to supply constraints

Fathom procures all of its manufacturing equipment and some of its materials from third-party vendors on a purchase-order basis. While some materials are available from a variety of suppliers and face lower supply constraint risks, many other products of the company have limited suppliers and might see greater risks in the case of a supply shortage.

Final Thoughts

Fathom addresses several different verticals, with Medical, Industrial, and Technology as the largest end markets. The firm has over 3K customers with a focus on large commercial customers and sticky relationships with 90% retention rate. The 3D printing space has seen material pressures on valuation multiples this year, but I believe the longer-term outlook remains healthy, driven by secular trends. I am bullish on the company given my optimistic view on the 3D printing space, a large TAM, and FATH’s growth strategy to expand its market share. I keep a price target of $4.03 on FATH.

Be the first to comment