Leon Neal

Shares of Fastly (NYSE:FSLY) surged on Monday just 2 days before reporting Q4 earnings and after Bank of America (BAC) raised its price target nearly 60% to $16.

Before we get into the broader outlook for Fastly, let’s take a look at what the Q4 earnings results are supposed to bring.

Q4 Revenue Estimates

- High: $115.8M

- Low: $113.88M

- Midpoint: $114.55M (+17.23%)

Looking forward several more quarters and Wall Street is expecting mid-teens growth into Q1 2024.

- Q1 2023: $116.81M (+14.1%)

- Q2 2023: $118.61M (+15.69%)

- Q3 2023: $125.1M (+15.27%)

- Q4 2023: $134.4M (+17.33%)

Solid enough growth on the revenue side to maintain interest in the stock, however this is coupled by no positive EPS expected for the foreseeable future.

The Q4 earnings will be just the second for newly appointed CEO Todd Nightingale who was just 60-days into the job during Q3. During a recent investor conference Mr. Nightingale outlined some of the opportunities he and the Fastly team have been working on.

I think the biggest one for me was the innovation roadmap, the velocity of innovation at Fastly and the way the roadmap is playing out, I think was in a lot better shape than I thought perhaps from the outside, especially in that there is sort of a core business in network services and content delivery and there is a growth engine – a growth business in security.

Investors are certainly going to be looking for an update on not only how Fastly maintains the mid-teens growth over the next year – but potentially how it can reaccelerate revenues. Clearly, the content delivery network (CDN) is the core, but if Fastly can build out a larger suite of products will be key in driving growth in the future.

One possible way is shifting its business model to a traditional SaaS pricing model versus consumption. During the pandemic, Fastly benefited from higher amounts of web traffic since it charged customers based on consumption versus a flat monthly fee.

This led for some explosive revenue growth, but clearly wasn’t sustainable after web traffic came back down to normalized levels. Additionally, most of Fastly’s competition is flat-rate pricing, so it made some customers opt for more predictable pricing structures.

CFO Ron Kisling outlined this during the investor conference in November stating:

It’s going to drive a bigger percentage of our revenue is going to be on that sort of SaaS model and recurring revenue. And then also, from our perspective, going to reduce some of the revenue volatility that we see from consumption as we see more and more business coming as recurring revenue-based contracts.

Ultimately this should smooth out Fastly’s revenue projections and also align it more closely with how competition is pricing similar products.

Investors will also be looking for updates on the company’s acquisition of Glitch, which the CEO even admitted at the same investor conference that it “was hard to understand externally”.

That’s because Glitch is essentially a community of developers which Fastly hopes becomes familiar enough with Fastly’s product offering that the enterprise clients that hire them end up using Fastly.

At the time the acquisition seemed like a long-tail way to develop more sales growth and investors are still going to need a clearer picture on how Glitch drives a pipeline of future sales growth for Fastly.

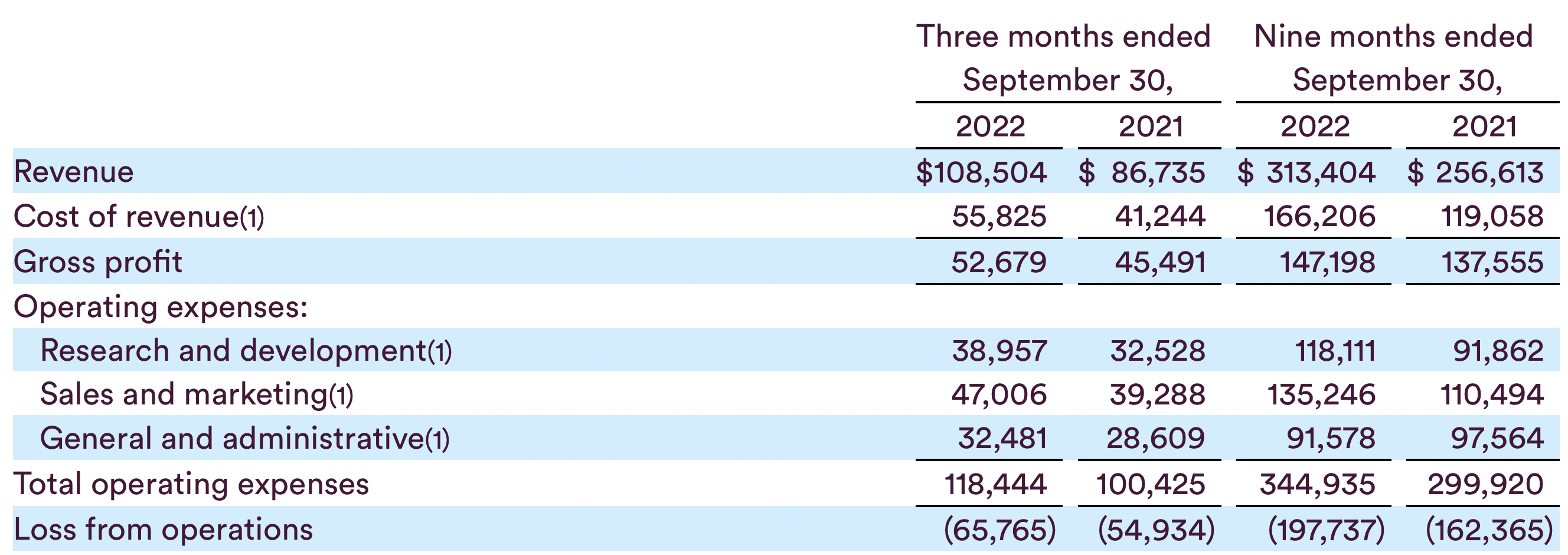

Flashback to Q3 and Fastly clearly has a ways to go in order to generate operating profits. The mid-teens revenue growth will be offset by increases in operating expenses. Although investors aren’t anticipating operating profits anytime soon.

Fastly Q3 Earnings Press Release

Companies in this position tend to point to adjusted numbers, which may turn off some investors, however it can shed light on Fastly’s business in a more reasonable way.

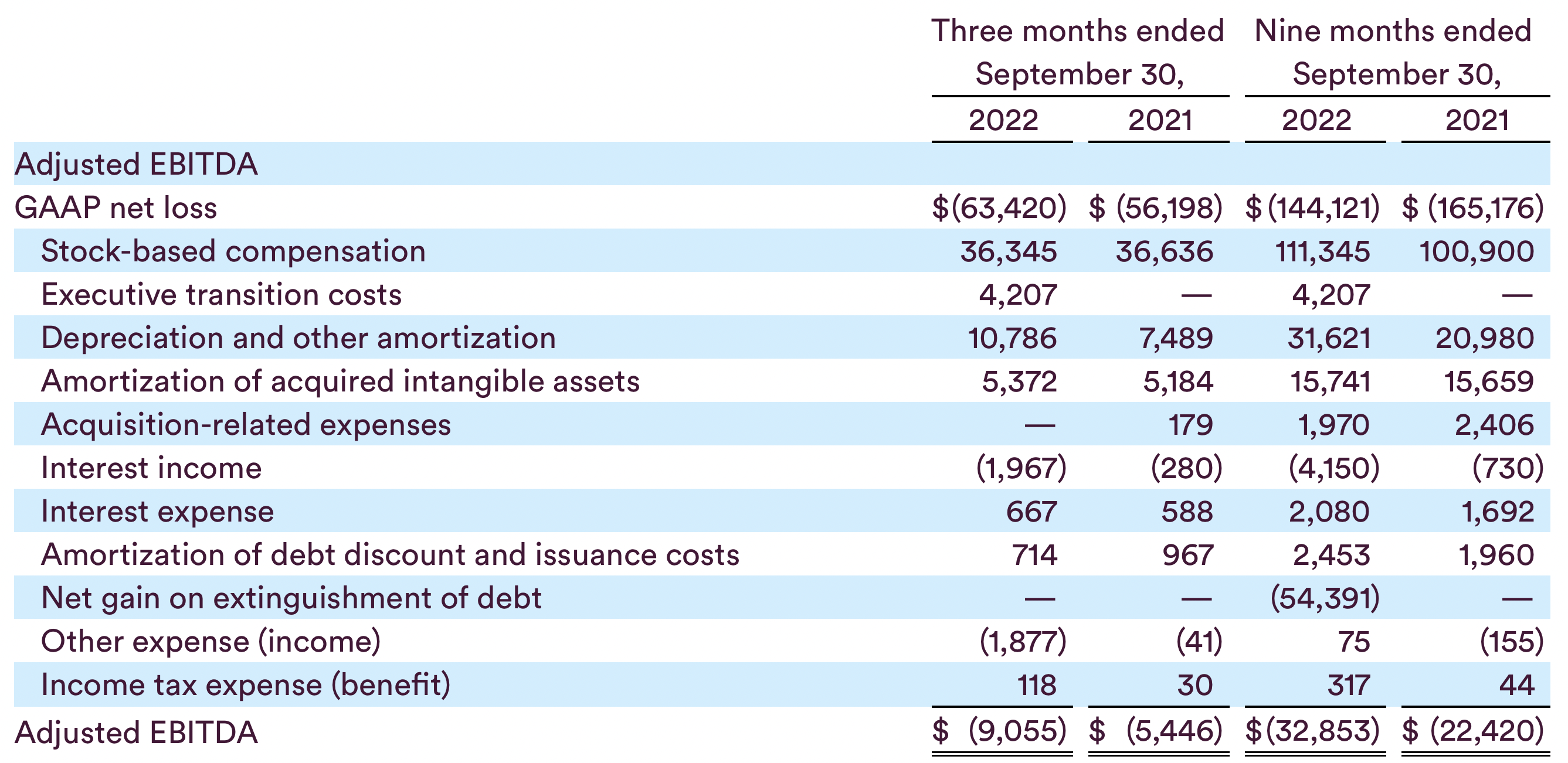

Fastly Q3 Press Release

From an adjusted EBITDA perspective, Fastly’s results still aren’t overly impressive. On the 3-month and 9-month basis loses simply continued to accelerate despite significant stock-based compensation and depreciation add-backs.

Luckily the company can pull some levers to reduce costs as server efficiency continues to get better. Management noted recently the company is targeting 60% gross margins in 2023 as it sees cutting server/bandwidth costs. That would be a significant improvement over the 48.6% gross margins the company achieved in Q3.

Back in August 2022 I wrote Hold On For The Fastly Bayout, as the company’s valuation had slipped below peers making it potentially an acquisition target. One of the problems is the regulatory environment is not favorable, particularly in the technology space, so it remains to be seen if that’s a viable outcome.

However, there are positive signs coming from Fastly management. After the Q4 results and conference call, investors should pay close attention to the gross margin expansion, product line extensions and commentary on how the new pricing model is parlaying into more sustainable revenue projections. Management seems to have a clear understanding of how to accomplish each and communication will be key considering Fastly stock has lost over 55% of its value just in the past year.

Conclusion

Overall, my rating is still a hold with Fastly. I’m encouraged by management commentary as the strategy shift to flat-rate pricing and expanding gross margins through server improvements is the right move. There’s also always the potential for a buyout as internet “plumbing” type companies like this are often potential acquisition targets for larger companies that already own vast server resources and have a long list of clients.

Be the first to comment