Jon Kopaloff

So far this year, with the generous recovery rally in tech stocks, it’s easy to get complacent and think that tidings are good and macro headwinds are behind us. And while I think that the tech rally still has more steam left for the remainder of 2023, the benefits will only accrue to select names – those that are relatively more impervious to the tightening economy – and that other more-vulnerable names will see their phantom rallies this year fade.

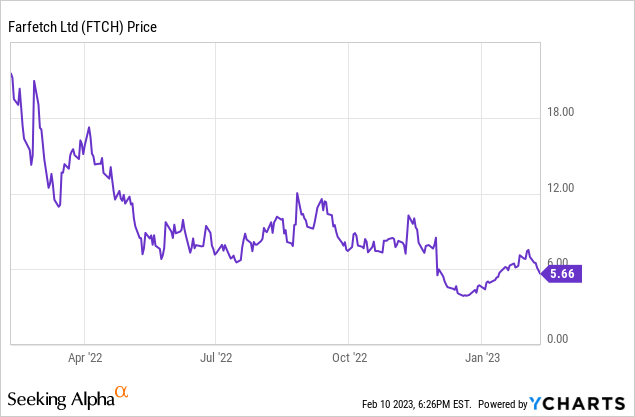

Farfetch (NYSE:FTCH) is a stock to turn more cautious on, in my view. The e-commerce company, which is known for specializing in high-end fashion brands, has seen a ~30% YTD recovery – even though gross merchandise sales have started to deteriorate amid a weakening profitability profile. It’s time to put the brake pedals on this one.

Though previously neutral on Farfetch (after having been bullish in the pandemic era), I am now bearish on Farfetch. Here are the major concerns I have on the name:

- Macro headwinds will take a heavy toll on Farfetch. In many recessions, blue-collar workers get hit first, and white-collar workers are relatively more immune. It’s the opposite in today’s economy, where lower-wage workers have seen a tremendous benefit from a lack of labor supply during the pandemic and boosted wages, and office workers are exposed to widespread layoffs as companies tighten their belts. This dynamic will have an incredibly adverse impact on the luxury category, and we’ve already seen Farfetch’s GMV decelerate into a y/y decline.

- Heavier promotions on the way? Farfetch management believes we are heading into a “very promotional environment” due to rising channel inventory in the fashion space. Farfetch, which has long prided itself on high gross margins, will be hurt in both its marketplace business as well as its company-operated brands like Off-White. It has a choice between trying to keep up with sales growth and discounting products to remain competitive, or prioritizing margin maintenance and falling behind other retailers.

- Major FX headwinds. A good chunk of Farfetch’s revenue is international, which leads to major FX translation losses on a dollar basis.

- Profitability concerns. Farfetch’s adjusted EBITDA and adjusted EPS have swung to wider losses owing to margin deterioration amid flat revenue. Especially in today’s volatile market environment which has paid more attention to tech companies’ bottom lines, this profitability concern will be a multi-quarter (if not multi-year) fix for Farfetch that will continue to weigh on sentiment for the name.

The bottom line here: in my view, Farfetch has more risk than reward this year, and the ~30% jump in the stock year to date is a good chance to cut losses and run. The company will next report Q4 earnings at the tail end of February.

I think we’ll have a chance down the line to re-invest in this name at lower prices, but at this juncture, the best move is to sell.

GMV decay is the first signal of a long uphill climb for Farfetch

Let’s start with the obvious: Farfetch’s sales are dramatically slowing down, and that outlook isn’t likely to get any better.

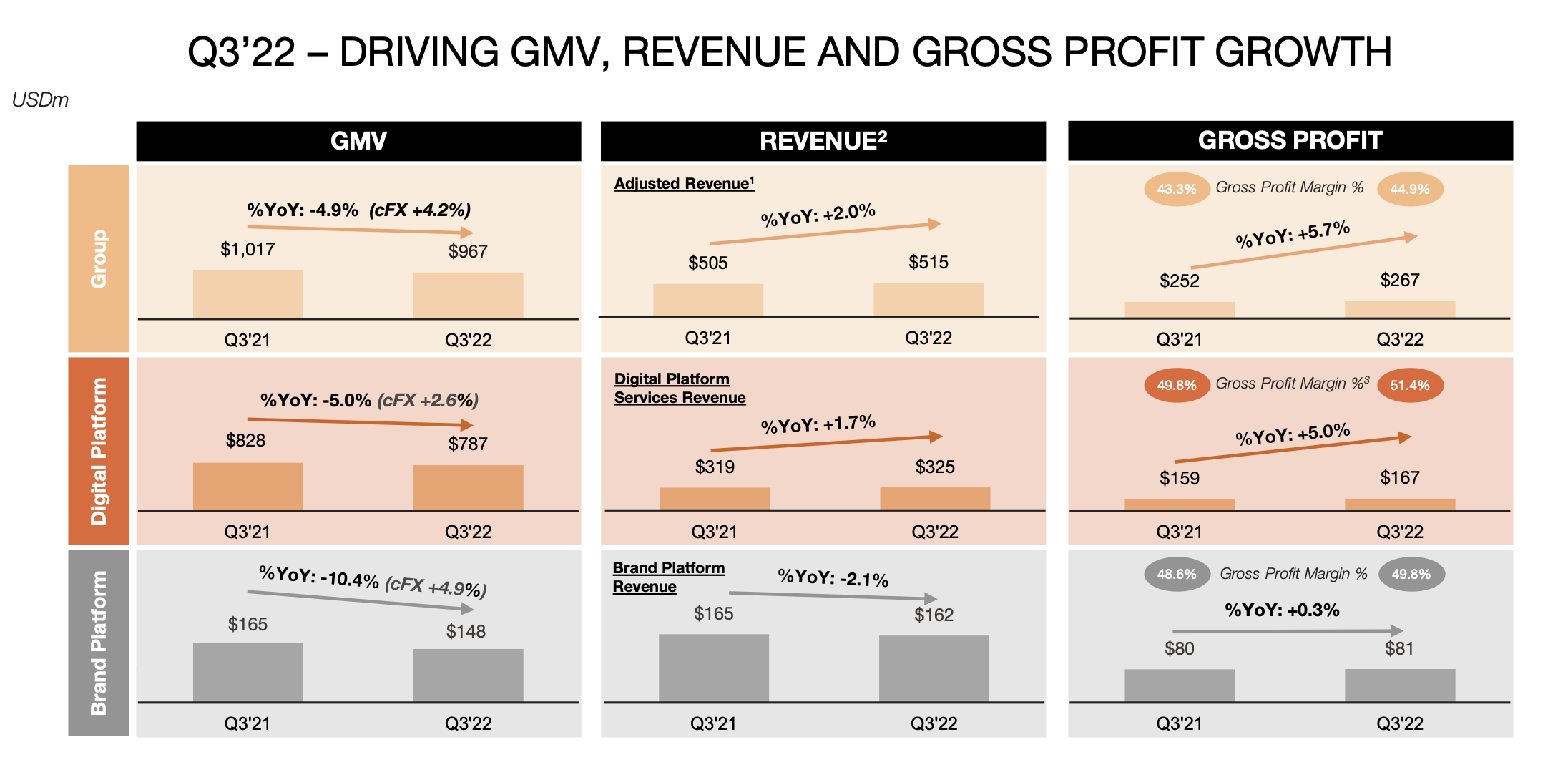

Farfetch Q3 highlights (Farfetch Q3 earnings deck)

In Farfetch’s most recent reported quarter (Q3, the September quarter), gross merchandise sales (GMV, or the sum value of all the goods sold on both a first and third-party basis on Farfetch’s platform) declined -5% y/y to $967 million. Of course, there is an FX impact here; on a constant-currency basis, GMV would have grown at 4% y/y. But this does represent a deceleration from 7% constant-currency growth in Q2. (We will note here that due to the weakening of the dollar since the third quarter, we expect FX headwinds to shrink and thus GMV to potentially re-accelerate on an as-reported basis in Q4).

To Farfetch’s credit, there are good-news tidbits under the hood here. One is the fact that revenue growth, at 2% y/y, is outpacing the dismal GMV results. The company has managed to boost its take rates by 250bps y/y, the result of Farfetch’s success in negotiating higher commissions from brand partners.

And so far, Farfetch has not dipped too far into promotions to salvage its growth. Demand generation expense as a percentage of revenue declined 400bps y/y (which is a lever that Farfetch can pull to achieve more growth if it desired). The company noted as well that in-store GMV grew 35% y/y, though against an easier pandemic-impacted comp last year.

Overall, however, I’m not so keen on the fate of the luxury sector heading into 2023. Though historically high-end consumer spending has been relatively safer from economic turmoil, the nature of this year’s potential recession (with layoffs occurring in the higher-paid sectors, including tech) may see different dynamics play out.

Profitability pressures

So far, though Farfetch has noted that high retail inventories are likely to drive a much more promotional environment in the sector, the company has stated that its strategy is to protect margins. Per CEO Jose Neves’ remarks on the Q3 earnings call:

Another area of focus in the current environment has been on further expanding margins through greater emphasis on disciplined growth. As a result of this initiative, Q3 gross profit margin increased 160 basis points year-on-year to 45% and digital platform order contribution margin expanded 580 basis points year-on-year to 32.4%, and we plan to extend this trading strategy through Q4.

In the current global macro environment, we’re seeing continued digital media cost inflation for luxury, especially in the US as well as reports of higher inventories indicating we’re going to be heading to a very promotional environment. We’ve made the strategic decision of prioritizing margin profitability over growth in this promotional markets, which is reflected in our revised full-year 2022 guidance.”

We’ll see how this plays out in 2023, however – if competitors slash prices, Farfetch may quickly lose market share and decide to turn demand generation activities back on in order to maintain its customers.

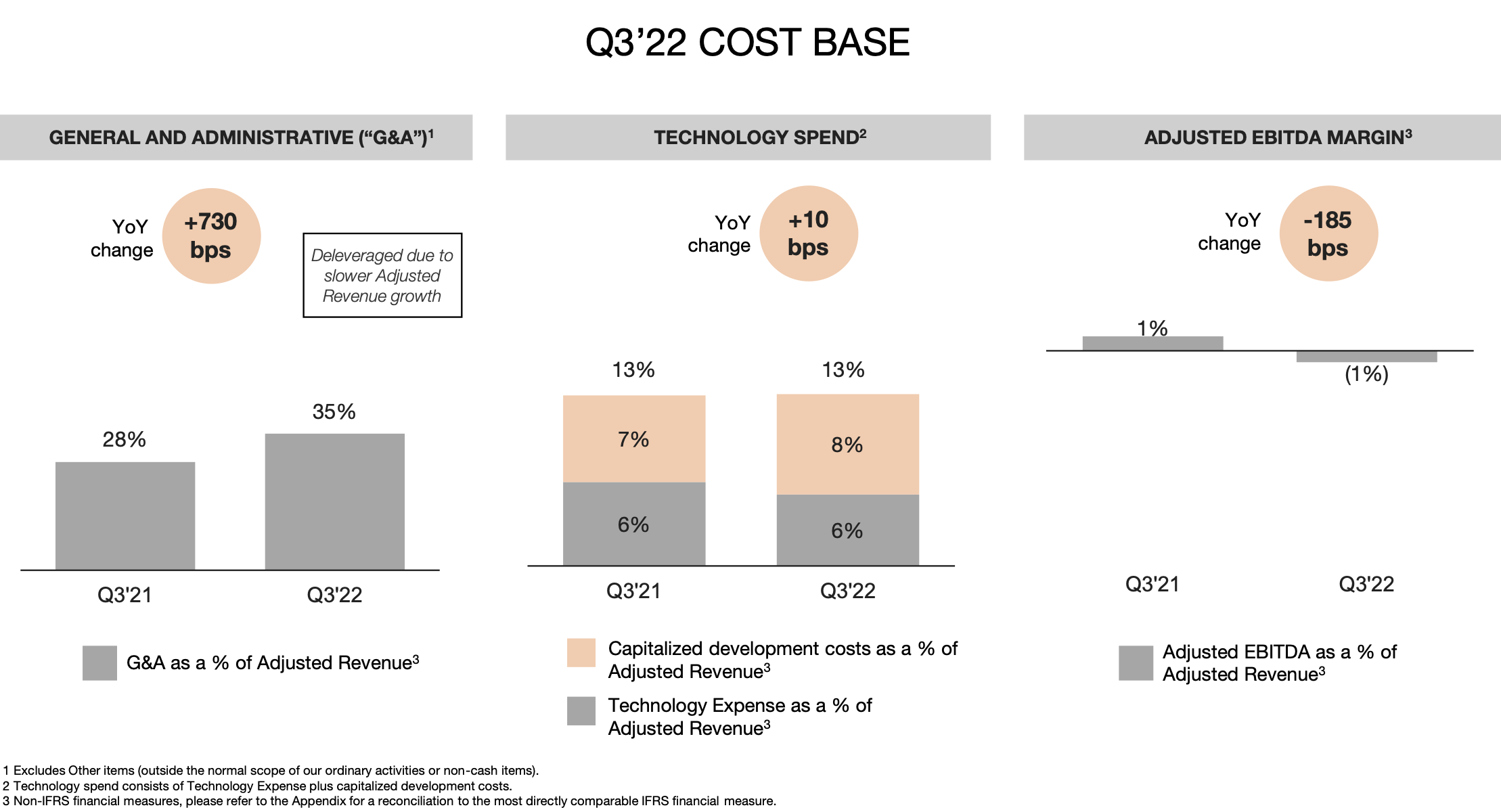

Meanwhile, profitability is already under pressure – in spite of higher gross margins and order contribution margins. In particular, Farfetch’s corporate overhead/G&A expense has risen 730bps as a percentage of revenue.

Farfetch costs (Farfetch Q3 earnings deck)

As seen in the chart above, this has swung the company’s adjusted EBITDA to a loss of $-4.1 million, representing a 185bps y/y decline in profitability. So far, Farfetch has committed to delivering adjusted EBITDA profits in 2023, but we’ll see if the combination of opex inflation plus potential competitor pressure into discounting may cause the company to waver from this stance.

Key takeaways

In my view, things will get worse for Farfetch before they get better. I think the company’s luxury sales will be under pressure throughout the year, both due to macro impacts as well as Farfetch’s own expectation that its competitors will resort to deep discounting (now may be the right year to be shopping!) Steer clear here.

Be the first to comment