Brandon Bell/Getty Images News

Exxon Mobil (NYSE:XOM) was besieged by questions about older fields that cost more and natural gas assets that “were not worth anything” and a lot more. The company was losing money so obviously management lost its touch. That of course was until the fiscal year 2021 happened. Then Mr. Market discovered that management knew what it was doing after all as the fourth quarter gushed cash at a rate not seen in years.

Exxon Mobil Key Operating And Income Summary For Fiscal Year 2021 (Exxon Mobil Fourth Quarter 2021, Earnings Press Release)

So many were worrying a year ago about the debt load. Even though basic management theory teaches us that (Michael Porter “Competitive Strategies”) that the safest time to expand a cyclical business is during a downturn, Mr. Market was quick to criticize the increasing debt load during the downturn from that expansion activity.

But as shown above, the latest quarterly cash flow annualized, would pay the remaining debt load off in less than a year with money left over. So, all the worry was really misplaced. The correct business move was to expand the business because costs were dirt cheap as suppliers were competing for whatever business they could find.

The result of those activities is some long-term assets are now operating that were built for costs that can no longer be matched by competitors now that the recovery is underway. Those assets will provide a competitive cost advantage that will show as additional profitability for years to come. The same Mr. Market that was worried about the debt a year ago will love the above average profits generated by the low-cost assets.

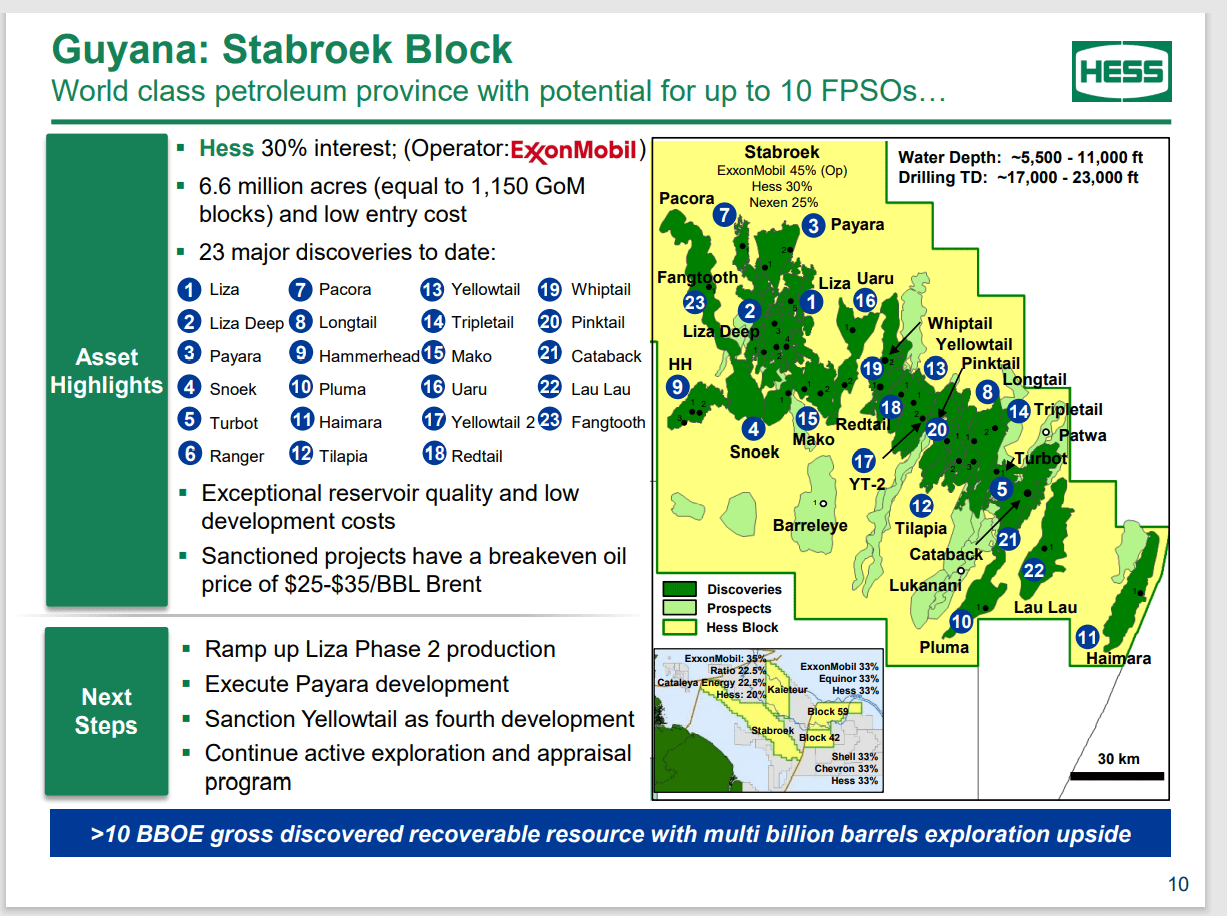

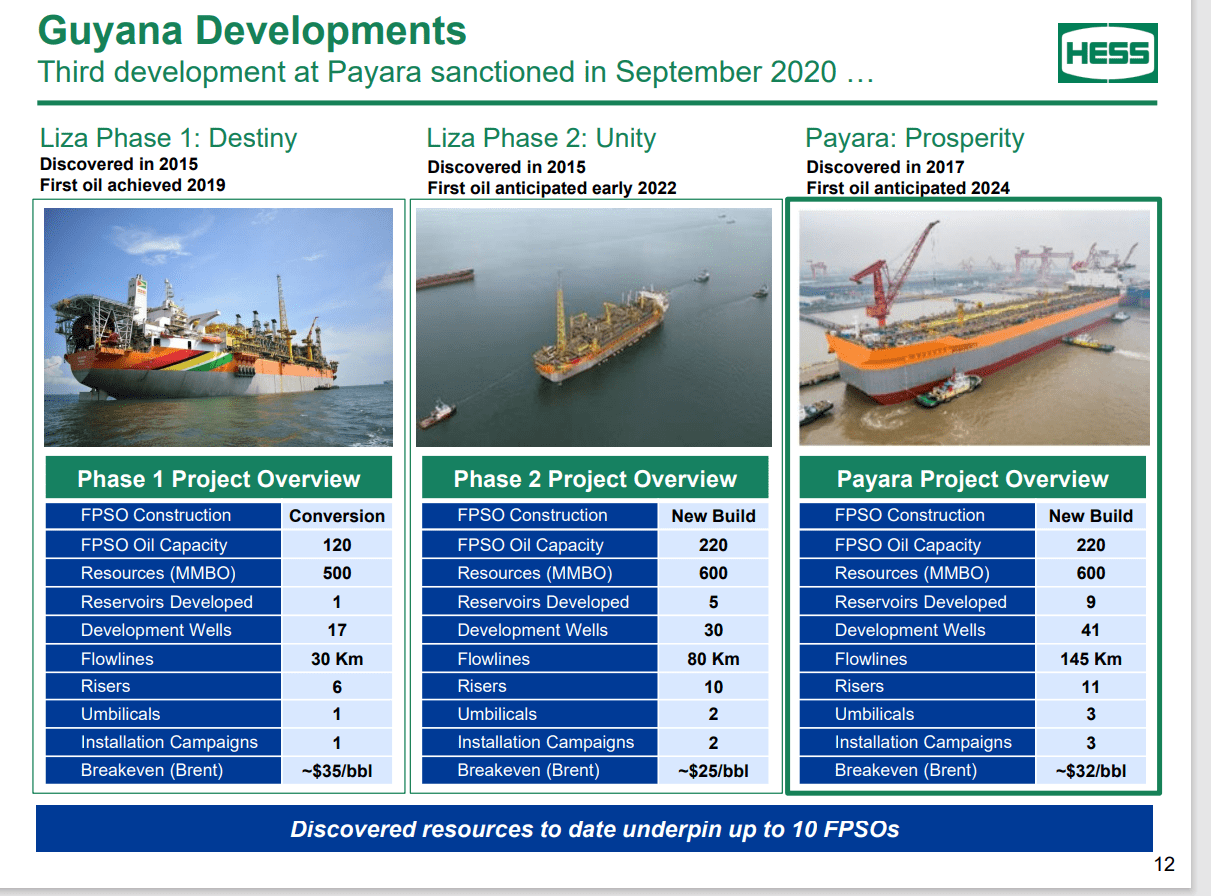

Guyana Stabroek Block Discoveries And Production Ramp-up (Hess Investor Presentation March 2022.) Exxon Mobil Guyana FPSO Deliveries and Key Performance Data (Goldman Sachs Energy And Clean Technology Conference Presentation By Hess)

The key to good management is most of the assets of this very major project were acquired when offshore prices were rock bottom. Now the partners are talking about cost inflation. That cost inflation will come after a lot of initial hiccups were overcome using those rock bottom prices.

The result is the latest FPSO has begun production, could pay back in less than two years if current prices hold. That is nearly unheard of for a long-lived offshore project. Most partners would not even consider the possibility. In fact, it was probably planned with a far longer payback period. But now, the partnership is looking at a very long period of time after the asset is paid back to garner a lot of free cash flow. It was extremely important to start this project at a time of low costs.

There are many partnerships in the area that will not even think about cash flow for years to come. By the time they go through the initial debugging process, this partnership will have found all kinds of efficiencies. This is one of the definitions of a competitive moat. In fact, leadership in this basin of this sort is likely to lead to low costs for years to come. A head start at the right time can be worth a lot of money in this industry. Here, that “lot of money” appears to be millions in cost savings and potentially billions in revenue at sky high commodity prices.

The even bigger deal is by the end of the decade there could be enough production from this project to equal about half of the current company production. So, the Exxon Mobil share of this project will be significant to the future of the company for years to come. There are a lot more assets needed to fully develop the project. But a great competitive advantage has to be a low-cost start, and this project appears to have taken advantage of an offshore industry downturn that lasted years.

Exxon Mobil is exploring off the coast of Brazil in hopes of eventually repeating the success in Guyana. Should one of these other projects like this one be successful, then Exxon Mobil could be in for decades of significant production growth not only in Guyana, but also in other basins.

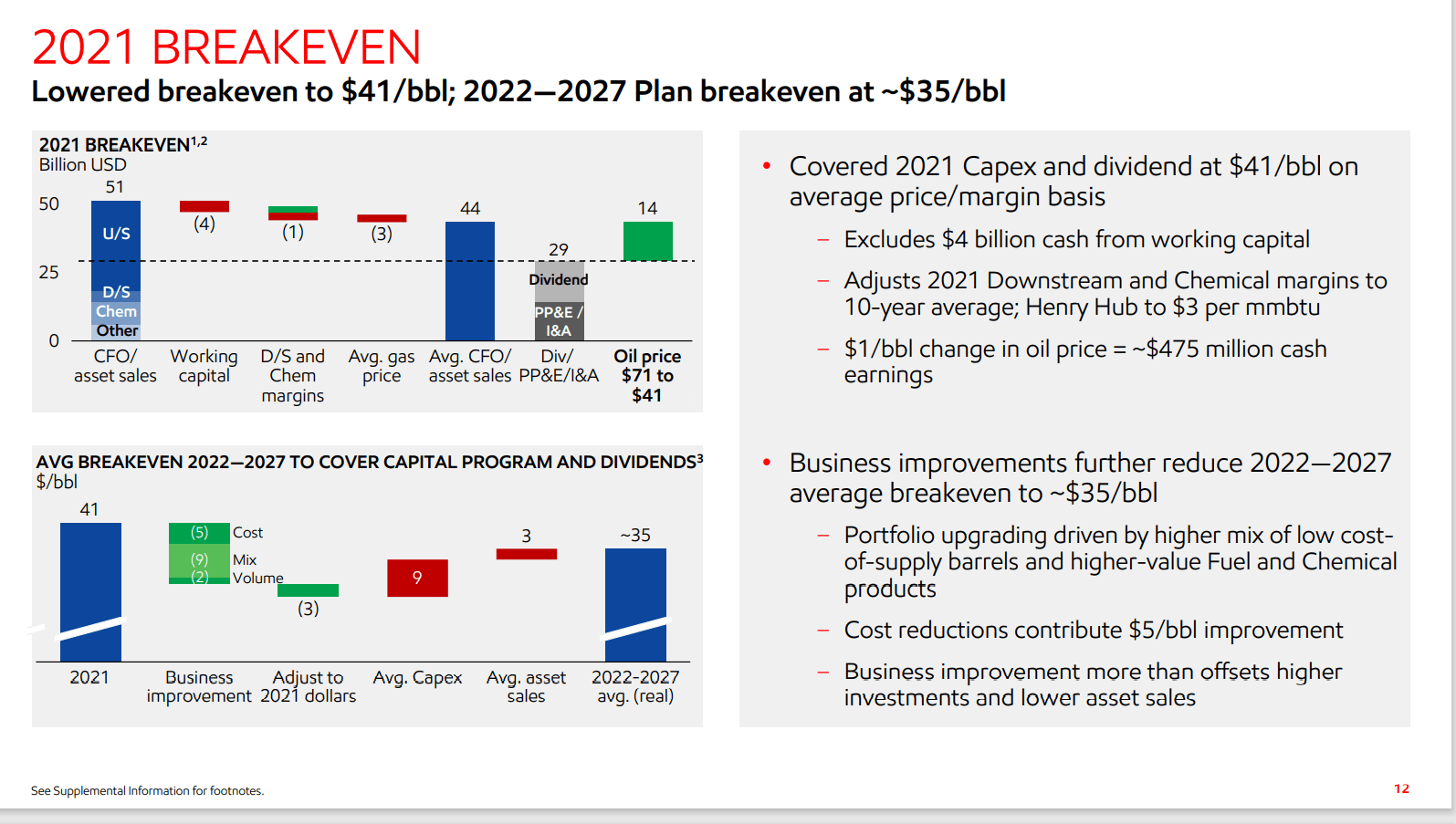

Exxon Mobil Declining Corporate Breakeven Price Model (Exxon Mobil Fourth Quarter 2021, Corporate Presentation)

A countercyclical investment strategy goes a long way towards decreasing the company breakeven point. Those lower cost services aid any technology improvements to help the company achieve lower breakeven points.

A large company like Exxon Mobil does not “turn on a dime”. This actually took several years of work before investors would notice the difference. By the time the loss of the previous fiscal year (2020) was apparent to the investment community, the work to make sure it would not happen again had already begun before that. Now that the company is moving in the direction of lower breakeven points, it would behoove management to make sure the company keeps moving in that direction.

Management has several exploration projects that may well provide surprisingly large future returns. So, the future price action of the stock is likely to be very different from the past. The largest difference is that management intends to grow already large upstream production significantly. That goal is definitely getting off to a slow start because the company is so large. But as the Guyana slides above demonstrate, that project has definitely become significant for a company the size of Exxon Mobil and it is likely to become more significant to the company in the future. Rarely does a company the size of Exxon Mobil have a discovery that turns out to be significant to the future prospects of the company. Normally it would be a lot of smaller projects combined.

Exxon Mobil Common Stock Price History And Key Valuation Metrics (Seeking Alpha Website March 27, 2022.)

The stock has clearly responded to the unexpectedly good fourth quarter news. But the future implies that this stock is still cheap. The fourth quarter cash flow annualized is about one-sixth of the enterprise value of the company. For a company of the stature of Exxon Mobil, that is extremely cheap.

This stock offers some recovery potential plus some high single digit future growth rates. That is a darn good deal for an integrated major. Some of the projects underway like Guyana may develop the scale to the point that they help to cushion future industry downturns with their growth.

Exxon Mobil also has a chemical division that will likely be a formidable presence in the continuing green revolution. Two major sources of green products are plastics and some coating chemicals. Both of these are likely near and for the foreseeable future sources of income.

Natural gas has a future as a source of hydrogen fuel. Natural gas also replaces far dirtier alternatives at the current time. There may be a better solution in the future. So far that future appears to be distant enough so that it will not stop natural gas use from growing.

The company future appears to be quite bright for a long time to come. Exxon Mobil will undoubtedly increase its presence in the renewable fuels market in the future. But for the time being, the oil and gas business will be tremendously profitable with good future prospects.

Be the first to comment