JHVEPhoto/iStock Editorial via Getty Images

When faced with a potential impending recession, most investors would pivot from what Morningstar’s Sector Structure describes as Cyclical Super Sector (Basic Material, Financial Services, Real Estate and some parts of Information Technology), to the Defensive Super Sector including Consumer Defensive (manufacturing of food, beverages, household and personal products), Healthcare and Utilities.

Coupled with rising rates, investors look towards strong balance sheet, free cash flow cash cows. However, the quintessential trade-off of the Defensive Super Sector would be the more-than-common low growth characteristics of these companies.

I believe Experian (OTCQX:EXPGF) (OTCQX:EXPGY) is an exception that ticks both boxes of strong credit, high cash flow generation, whilst still maintaining significant growth in both revenue and bottom line metrics. The relatively low capital requirements, with 45% of cost base being adjustable to market conditions, will further allow for a downside buffer and the ability to scale rapidly if need be. Experian has sufficient downside protection attributable to its economic moat, which stems from the size of its dataset, which has almost 1.6 billion cumulative individual and business credit history data and its broad product offering and customer base.

More about Experian

Experian is a world leader in the information consumer credit sector and offers credit reports, risk management tools, and marketing services to clients all around the world, which includes both businesses and consumers. The company operates within the Industrial (Research and Consulting Services subsector) and Information Technology sector, and could be considered somewhere in-between Defensive and Cyclical, with moderate correlations with business cycles.

Experian IR Roadshow Presentation November

Since its inception in Ireland in the 1990s, operations have grown globally to regions including but not limited to North America, the United Kingdom, EMEA and APAC. The company has over 21,700 employees across 43 countries and is helmed by Brian Cassin, who has two and a half decades of experience cumulatively in merchant banking, investment banking and Experian.

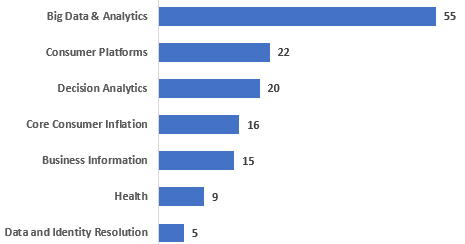

Experian is a leader in a High barrier of entry space, with a growing US$130 billion addressable market. The company continues to establish and grow market leadership, and is the custodian of over 1.6 billion people’s data.

Author’s Representation of Addressable Markets (in USD$b)

Profit and Cash Flow Resiliency in Times of Global Turmoil

Experian has demonstrated strong profit and cash flow resiliency in the past, with the company consistently generating strong profits and cash flow even in times of economic downturn or market disruption, and is likely to continue to be a key driver of the company’s success in the future.

The company has maintained revenue and net income resiliency growth through the pandemic and macro instability. What’s most impressive is Experian’s ability to weather the systematic downturn of 2019, enabling YoY growth in the 2016-2022 period. This unwavering, substantial cash-generative business translates into high returns for both equity and debt investors. Revenue consensus estimates from 2023 to 2025 is expected to grow at a 5.95% CAGR, compared to a 0.3% and 1.4% GDP growth in 2023 and 2024 respectively.

Seeking Alpha’s Profitability Grade

Experian has steady, consistent dividend payouts and share repurchases which have occurred in nine out of the last ten fiscal years, demonstrating cash-cow-like characteristics, while maintaining above-par growth prospects. To add on, dividend payouts have been consistently increasing modestly, from $0.35 in 2013 to $0.53 in 2022.

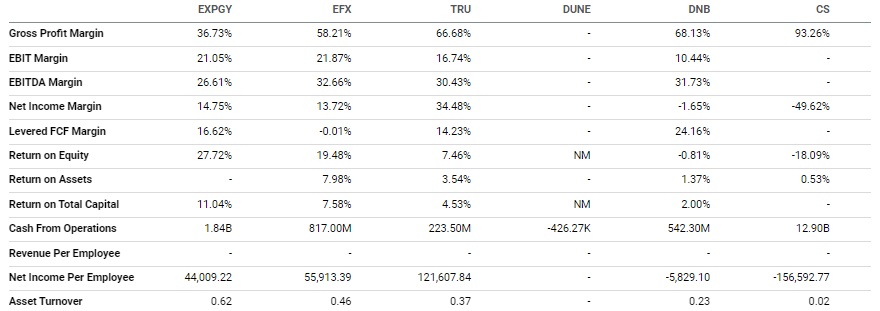

Return on capital have been solid and unwavering, beating out key competitors including Equifax (EFX) and Dun & Bradstreet (DNB) in the metrics game, with ROE at 27.7% and ROIC at 11.04% despite the pandemic and global equity headwinds. Equally importantly, levered FCF generation was at 16.62%, the highest among its comparable companies.

Seeking Alpha’s Key Stats Comparison

Growth Opportunities

Robust New Client Segment in the BNPL Space

Experian has developed a strong lead in the Buy Now Pay Later (BNPL) segment where affordability checks are crucial in order to prevent potentially vulnerable consumers from overextending their credit. Experian’s decisioning software aims to solve one of the most pertinent problem in the BNPL space, fraud, where fraudsters try to take advantage of user-friendly identity checks in BNPL applications to commit financial crimes.

Overall, the BNPL segment is, and will continue be one of the highest growth areas within consumer finance and is projected to surpass $1 trillion by 2030, and Experian provides key solutions to enabling safer and more reliable usage for this space.

Growing Demand for Credit Reports and Risk Management Solutions

As businesses and consumers globally feel the weight of worsening credit conditions, it becomes increasingly pivotal for them to manage credit ratings, risk and score. Experian also provides a platform for the unbanked, or those without access to credit (E.g. SMEs) to find funding through alternative credit scoring data for business continuity. On the flip side, with tightening conditions and the risk of a full-blown recession, creditors are becoming more stringent with capital lending, with greater reliance on credit reports and rating by companies such as Experian.

Defensive Characteristics

Partnership and Geographical Diversification

Experian has diverse, rooted expansions into wide geographical segments and industries enables for the continuous expansion of market share, which will minimise idiosyncratic risk in terms of revenue downside variability amidst global uncertainty.

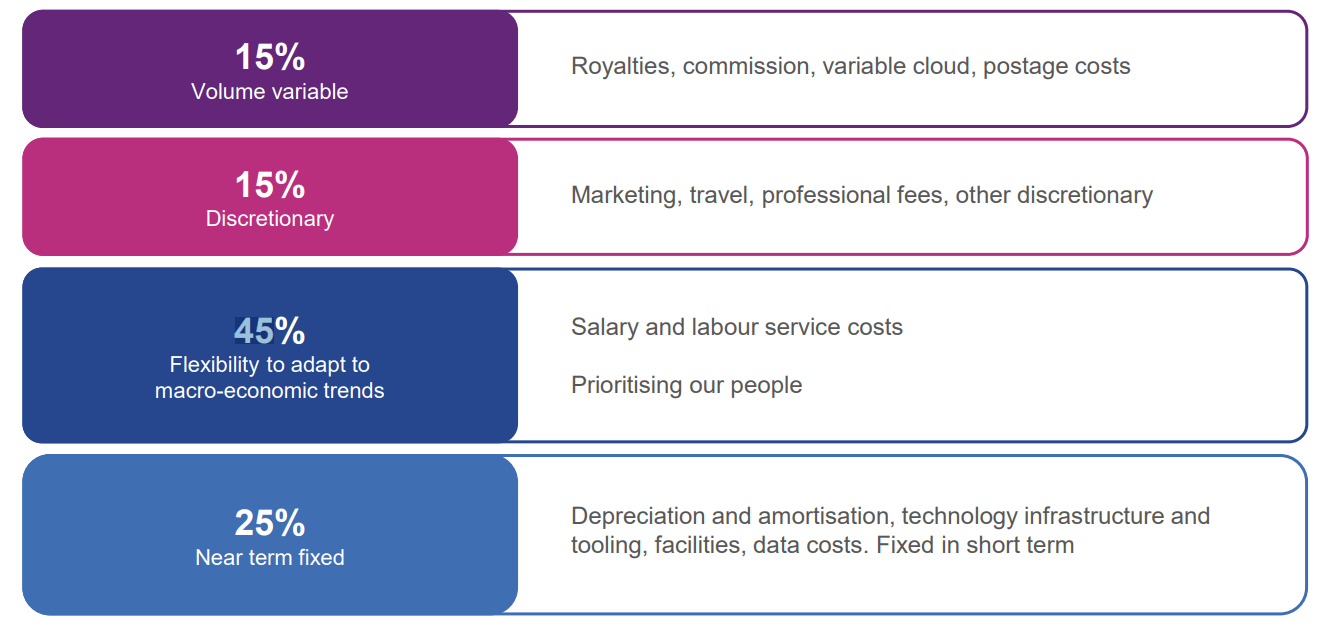

To add, the company has implemented various cost cutting measures in the past, such as reducing headcount and streamlining operations in the 2008 Subprime Mortgage Crisis, through near-shoring activities and data center consolidation which have helped the company to weather through turbulent times. The company further protects its downside risk through its 45% adaptable cost base and a further 15% in discretionary spending which can be cut swiftly based on macroeconomic trends.

Experian Investor Presentation

Ironclad Balance Sheet

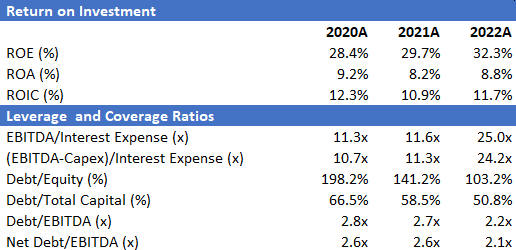

Experian has also been deleveraging, which is reflected by its D/E ratio improving from 198.2% to 103.2% and debt/EBITDA decreasing from 2.8x to 2.2x over the last two years. The company’s coverage ratio has more than doubled from 2021 to 2022, signalling strong earnings and a healthy balance sheet.

Author’s Representation of Experian’s Metrics

Valuation

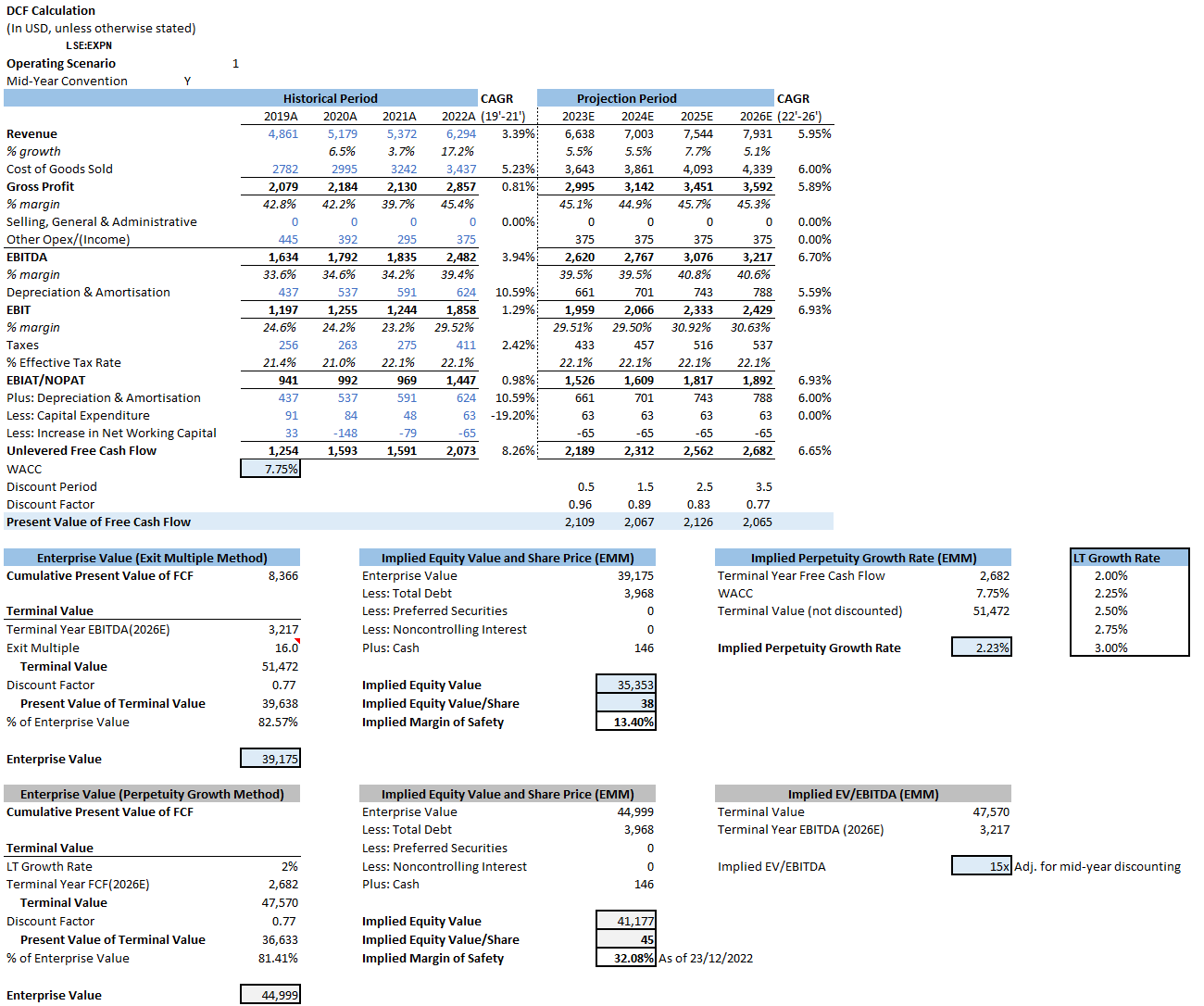

Our Gordon’s Growth Method valuation with a 2% long-term growth rate gives Experian a potential 32% upside potential, whereas our Exit Multiple Method provides a 13.4% upside from current levels. We do not believe there will be too much revenue wide-swing variations, as per Experian’s historical revenue and investors should be basis assumptions more heavily towards the Exit Multiple Method instead of the Gordon’s Growth Method. We believe with a strong balance sheet, unwavering free cash flow generation and its proven ability to tide through recessions are undervalued premiums, and will only be fully priced into Experian’s stock in 2023 when potential worries are materialised.

The WACC used was 7.75 and we believe revenue growth at a 5.95% CAGR, as per street consensus would be manageable for Experian- Revenue growth in H1 2023 came in at 9% based on constant FX rates (with 8% being organic revenue growth), and 7% on an actual FX rates basis, compared to our relatively modest model of 5.5% in FY2023. On a FY basis, Experian’s management expects 7-9% revenue growth.

We model a more conservative-to-grey-sky expectation as a whole, partially as the EMEA/APAC revenue segment has yet to turn EBIT positive, and a market downturn will further prolong positive expansion efforts into these regions. However, we believe there is light at the end of the tunnel, with benchmark EBIT improving 4.8% YoY within these region composition. Furthermore, impact is minimised due to the small revenue percentage of the EMEA/APAC revenue segment, which was 8.1% of total revenue in FY2022.

Author’s Experian Discounted Cash Flow Model

Key Risk Factors

Changes in the Regulatory Environment

The information consumer credit industry is governed by a number of laws, including the Fair Credit Reporting Act (FCRA) in the United States and the General Data Protection Regulation (GDPR) in the European Union. The business and compliance costs of Experian may be impacted by changes to these regulations. Furthermore, in high growth target segments in the BNPL space currently has limited regulatory oversight, and growth in the BNPL space, and subsequently Experian might be hindered if further regulations are imposed, such as after the Woolard Review, which came about after the Financial Conduct Authority’s Board Commissioned a review of the unsecured credit market.

Market Disruption

Economic downturns and market disruptions can affect Experian’s business, as businesses and consumers may reduce their use of credit and demand for credit reports and risk management solutions. If this scenario occurs, instead of an increasing need for credit reports and the maintenance of credit ratings due to worsening credit conditions, Experian could experience material revenue downside.

In a Nutshell

A Rare Scoop of “Warm Porridge”

I believe Experian will outperform the broader market due to its inherent ability to diversify its end customer, product base and geographical segments. Additionally, its economic moat in terms of its 1.6 billion user dataset and expanding product base including a rapidly inflating BNPL market will enable Experian to tide through a potential recession in 2023.

Moving into 2023, with a threat of recession looming and rates expected to remain high, managing potential downturns and downside could even outweigh the importance of a stock’s upside. As such, Experian’s robust balance sheet, leverage and coverage metrics, paired with its FCF generation resiliency could be one of the rare scoops of “warm porridge” in this not-so-Goldilocks economy.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment