NicoElNino/iStock via Getty Images

Always keep your foes confused. If they are never certain who you are or what you want, they cannot know what you are likely to do next. ― George R.R. Martin

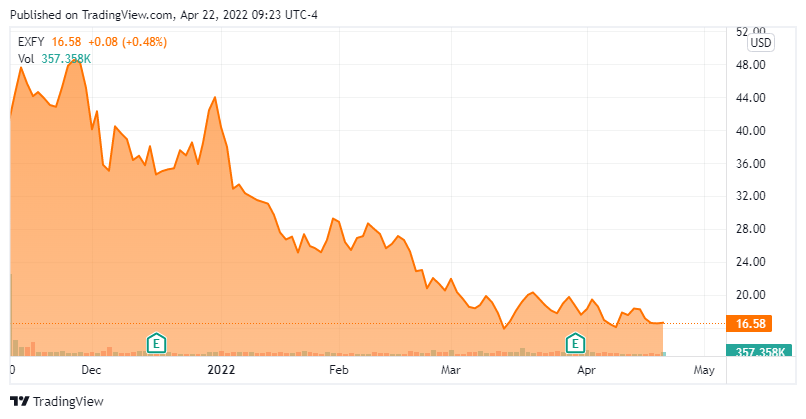

Today, we take our first in-depth look at Expensify (NASDAQ:EXFY). The company debuted in the fourth quarter of 2021, and the stock has rapidly found itself deep in ‘Busted IPO‘ territory. A ‘risk off’ market bears the brunt of the blame for this decline. Can the shares rebound? We attempt to answer that question via the analysis below.

Seeking Alpha

Company Overview:

Expensify is based in Portland, OR. The company has developed and provides a cloud-based expense management software platform to individuals, small businesses, and corporations. Capabilities provided by the said platform helps firms manage corporate cards, pay bills, scan receipts, generate invoices, collect payments, and book travel. The stock currently trades around $16.50 a share and sports an approximate market capitalization of $1.5 billion.

Fourth Quarter Results:

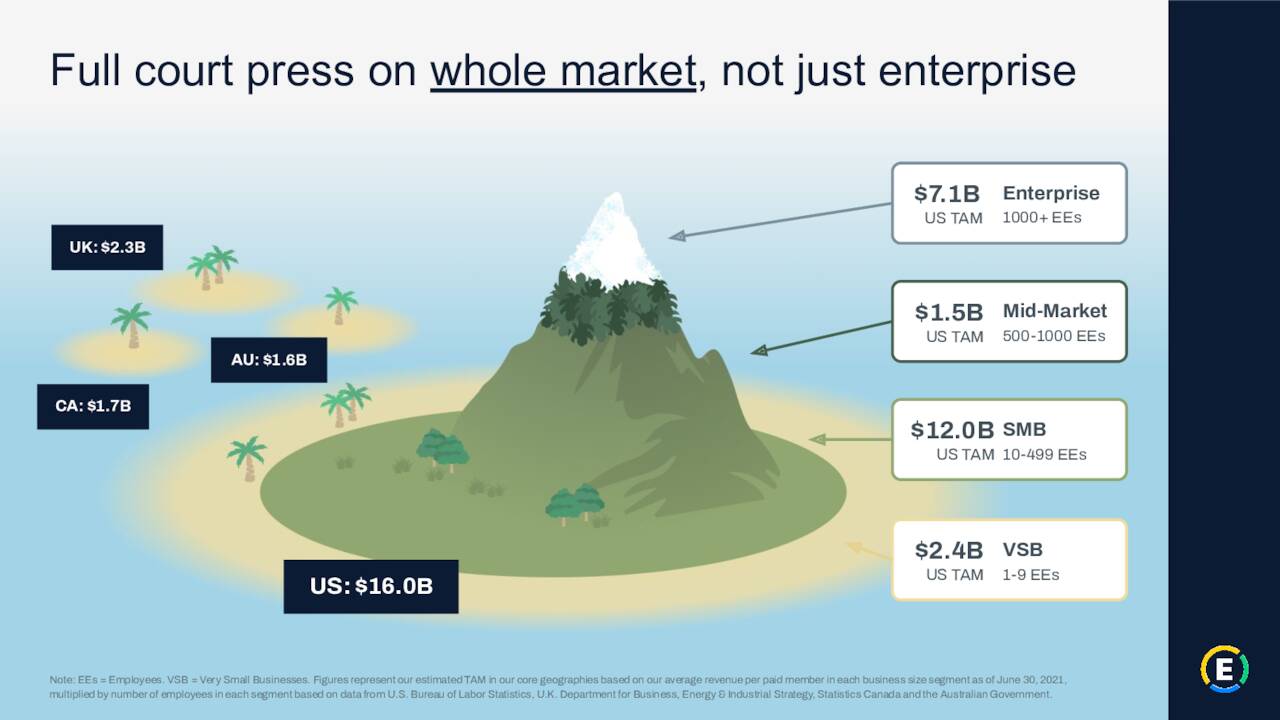

April Company Presentation

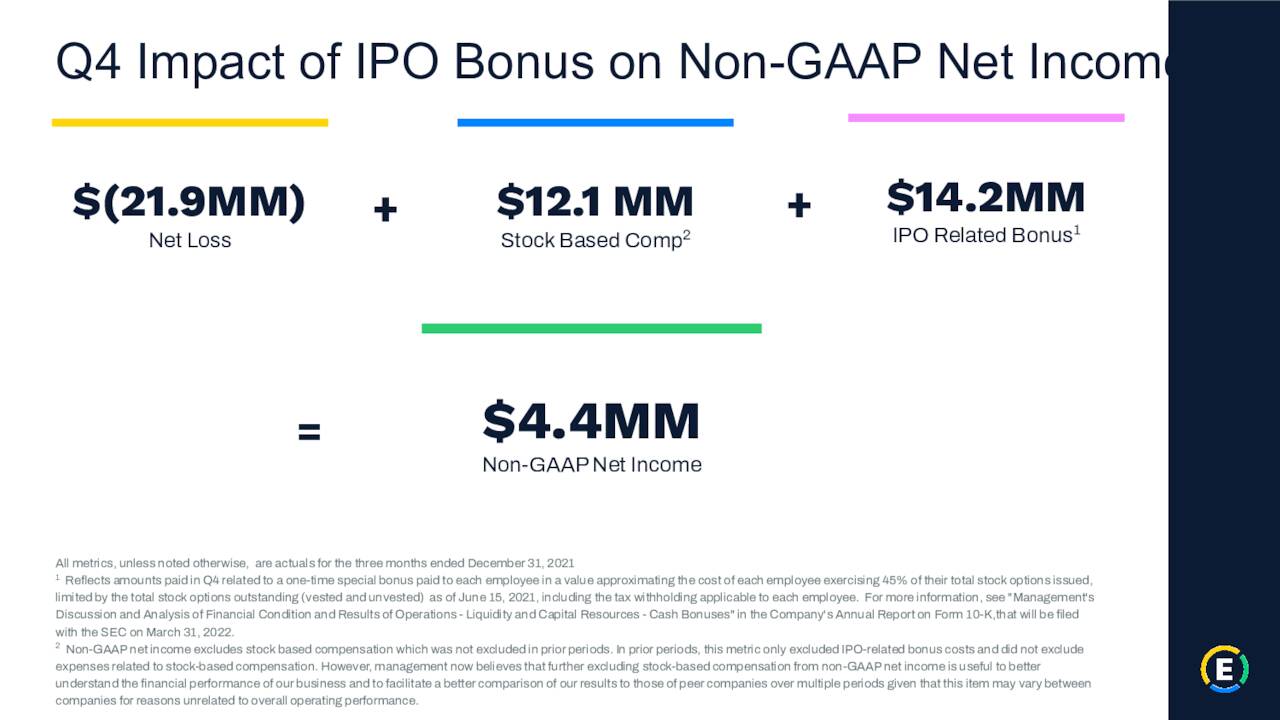

The company reported fourth quarter numbers at the end of March. They were quite disappointing. Expensify posted a GAAP loss of 82 cents a share, substantially above the 8 cents a share loss expected. The total net loss for the quarter was $21.9 million. It is important to note two things. First, this number included a one-time IPO-related bonus expense of $14.2 million. Another $12.1 million was for stock-based compensation. Second, even accounting for that, the GAAP loss was significantly over the consensus even as management was intent to focus on the positive EBITDA if you just took out those two items.

April Company Presentation

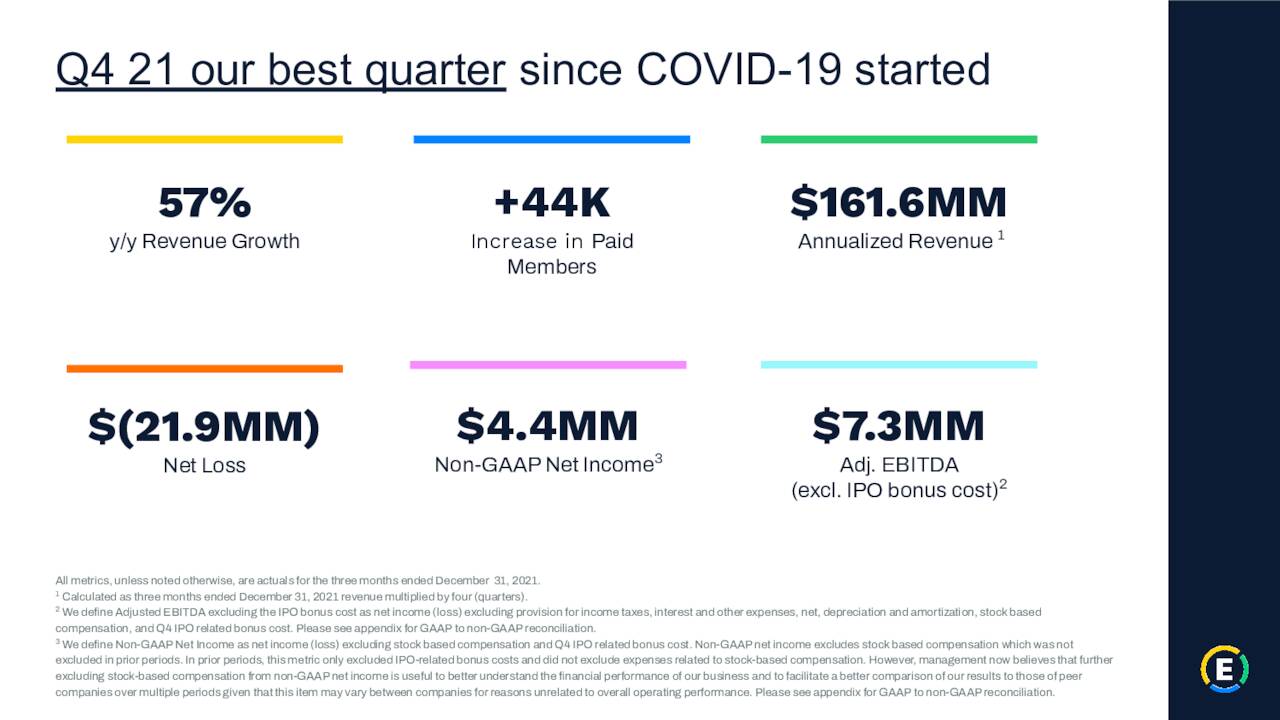

The company did see revenues increase 56% on a year-over-year basis to $40.4 million, which was a bit over the consensus estimate. For FY2021, revenues rose 62% over FY2020’s levels to $142.8 million. The company provided the following guidance for this first quarter of the new fiscal year.

April Company Presentation

Analyst Commentary & Balance Sheet:

Since fourth quarter results posted, four analyst firms including Piper Sandler and JP Morgan have reiterated Buy ratings on the stock. Albeit, two of them had downward price target revisions. Price targets proffered range from $25 to $47 a share now. Both Bank of America ($22 price target) and Loop Capital Management ($17, down from $22 previously) maintained Hold ratings on the shares.

The company ended FY2021 with just under $100 million in cash and marketable securities on its balance sheet against just over $50 million in long-term debt. Just over 12% of outstanding shares are currently held short. There has been no insider activity in the stock (neither buying nor selling) so far in 2022.

Verdict:

The current analyst consensus has Expensify earning roughly 30 cents a share in FY2022 as revenues jump a projected 25% to just under $180 million. That leaves the company selling for just over seven times FY2022’s projected equating for the next cash on the balance sheet. Expensive, but certainly less than the 14-15 times revenues Expensify was valued at when it first came public less than a year ago.

April Company Presentation

Expensify is moving to profitability and one could possibly justify paying that premium if one was confident sales would grow at a 25% to 35% CAGR for years to come like the company’s management is at the moment.

April Company Presentation

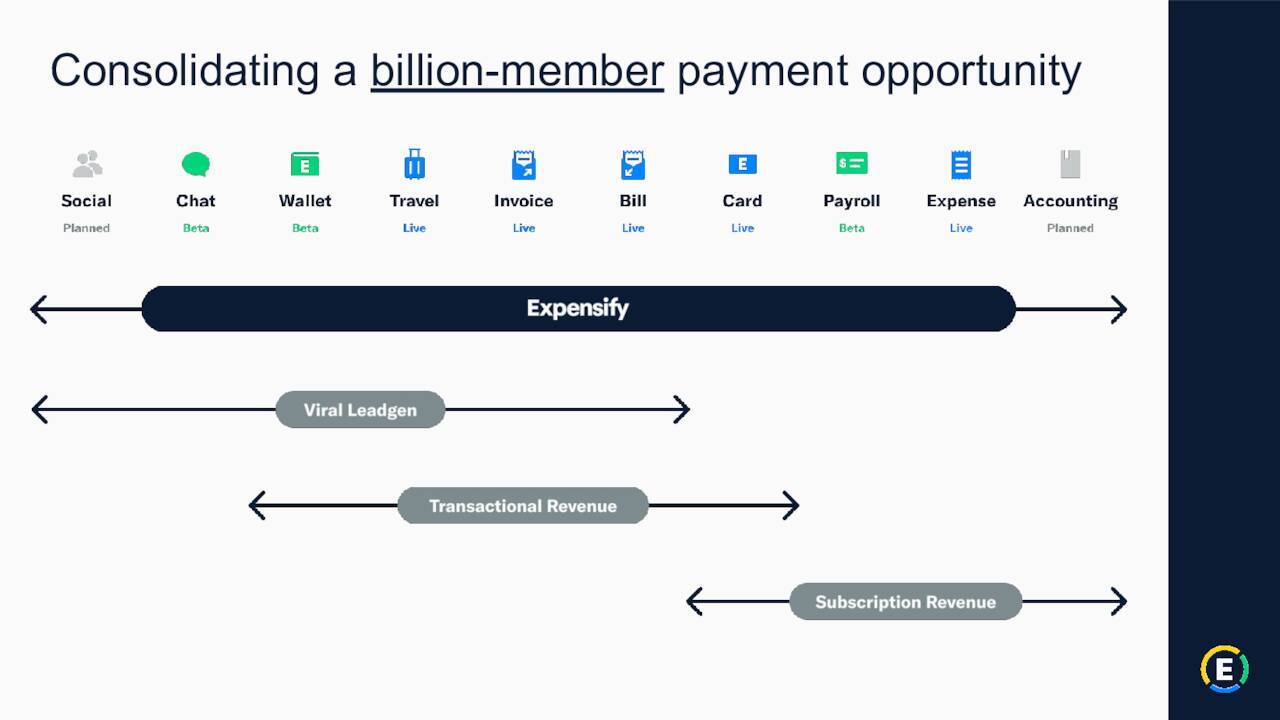

I am not quite there yet even though Expensify is targeting a huge potential market. If the market environment wasn’t so dismal so far in 2022, I would probably initiate a small ‘watch item’ holding in this name. Therefore, Expensify is worth keeping an eye on but we have no investment recommendation on the stock at the moment. Maybe when the company starts to post quarterly profits (without adjustments) and/or insiders start to buy the dip, we will revisit Expensify at that time and do a status check.

April Company Presentation

Every man should lose a battle in his youth, so he does not lose a war when he is old.”― George R.R. Martin

Bret Jensen is the Founder of and authors articles for the Biotech Forum, Busted IPO Forum, and Insiders Forum

Be the first to comment