Marco Bello

A market research report on Exact Sciences (NASDAQ:EXAS) from Cathie Wood’s ARK-Invest (ARKK) (ARKG) has caught a lot of attention with another assertive call on the share price performance in the coming years. ARK believes that “our base case, shares of Exact Sciences could compound at an average annual rate of 25%, reaching $140 by 2027.” Cathie Wood and ARK are becoming well-known for making big calls on some of the hottest names on the market including:

- Zoom Video Communications (ZM) at $1,500 by 2026.

- Roku (ROKU) at $605 by 2026

- Tesla (TSLA) at $3,000 by 2025.

- Bitcoin (BTC-USD) at $1M by 2030.

Admittedly, it is hard to believe these tickers will be hitting those targets in those timeframes considering where they are trading at this time. However, I believe ARK’s call on EXAS is feasible considering the company’s fundamental outlook, and removal of a substantial overhang. Seeing that EXAS is trading around $49.50, I will take a nearly 300% upside in the next five years, which is why I still have EXAS in my Compounding Healthcare “Bio Boom” speculative portfolio.

I intend to provide a brief background on the Exact Sciences and will discuss why ARK is so bullish on its future prospects. Then, I will defend ARK’s $140 call on EXAS. Finally, I deliberate on Cathie’s other healthcare picks, and how I am managing EXAS as well as my other common positions in my Compounding Healthcare portfolios during this prolonged market-wide sell-off.

Background on Exact Sciences

Exact Sciences is a molecular diagnostics company that offers cancer screening and diagnostic test products. The company’s flagship product, Cologuard, is a non-invasive stool-based DNA screening test to detect DNA and hemoglobin biomarkers associated with pre-cancerous polyps and colorectal cancer. Colorectal cancer screening has grown into a sizeable market in recent years and Cologuard would be considered the leading brand. Cologuard has been over 10M times since its launch and has identified approximately 315K pre-cancerous polyps and 46K cases of early-stage cancers. On top of Cologuard, Exact also has Oncotype DX and Oncomap ExTra.

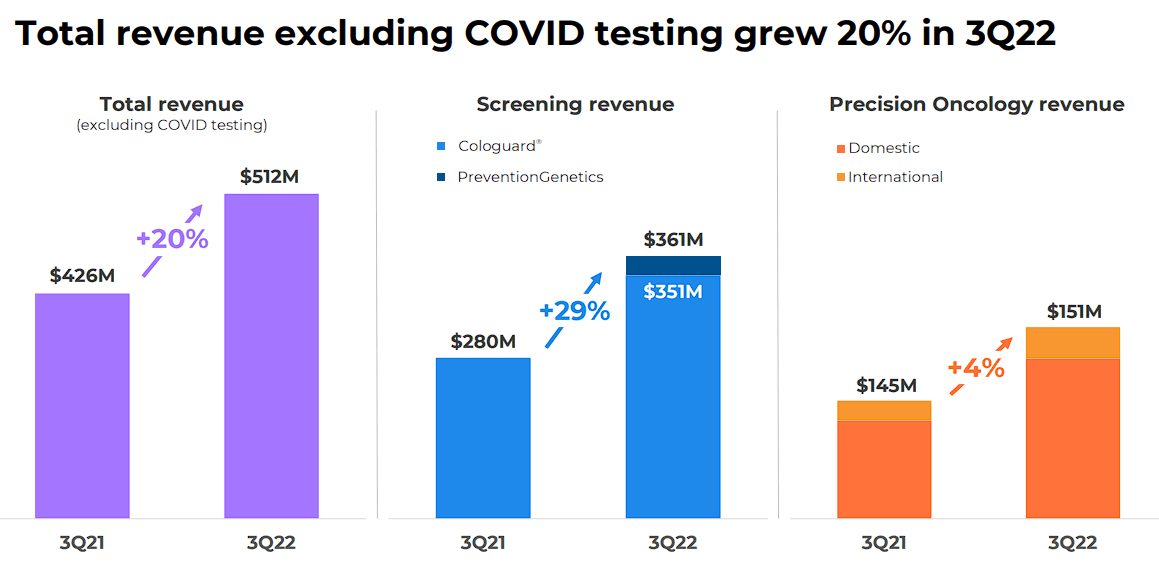

Exact has had a strong 2022 thus far and reported a strong beat on EPS and revenue for Q3. Exact was able to grow its Q3 revenue to $512M, which is up 20% year-over-year, excluding COVID testing.

Exact Sciences Q3 Performance (Exact Sciences)

Growth was fueled by screening revenue, including Cologuard and PreventionGenetics by 29% year-over-year. Exact reported that “10,000 new health care providers ordered Cologuard” in Q3. Precision Oncology revenue was up 4% to $151M, led by Oncotype DX Breast. As for the company’s COVID testing revenue, the company saw a 64% decrease to $11M.

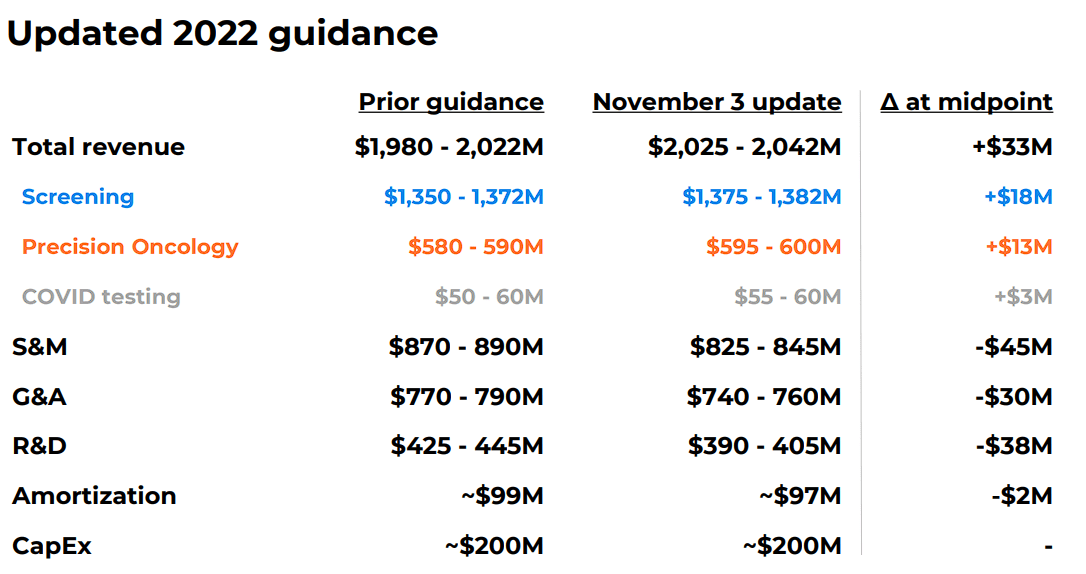

The company’s Q3 performance encouraged them to raise their full-year revenue guidance by $33M while decreasing OpEx guidance by $113M. In addition, Exact is amending their adjusted EBITDA profitability goal date to Q3 of this year, compared to their previous target of 2024.

Exact Science Updated 2022 Guidance (Exact Science)

ARK’s Take on Exact

ARK believes Exact Sciences is a “pioneering force in the growing field of oncology testing and will likely remain so during the next five years” thanks to their Cologuard and Oncotype DX testing franchises, and their efforts to expand their “services across the entire cancer care continuum-from prevention to late-stage disease.” ARK sees Exact to continue to lead CRC testing through 2027 thanks to their brand recognition in addition to other competitive advantages. As a result, ARK expects “shares of Exact Sciences could compound at an average annual rate of 25%, reaching $140 by 2027.”

It should be mentioned that ARK is in deep on EXAS. You can find EXAS in ARK Innovation ETF (ARKK), where EXAS is listed as the fund’s second-largest holding at 8.32%. What is more, you can find EXAS in her ARK Genomic Revolution ETF (ARKG) which is the fund’s top holding at 11.42% weighting. Overall, ARK Investments LLC is the largest shareholder at around 10% stake. So, it is no surprise that ARK is bullish on EXAS.

Defending Cathie’s Call For EXAS At $140

Although I can’t get behind Cathie on some of the other calls that I mentioned above, however, I can get behind her on EXAS for a number of reasons. First, Cologuard is becoming synonymous with colorectal cancer screening and is essentially the standard of care due to its accuracy and the fact it’s a convenient at-home test. Moreover, Cologuard is in all major guidelines, broad insurance coverage with no cost to the patient. Remember, roughly 10M people have completed the Cologuard test. What is more, the company is still seeing growth, with more than 150K healthcare providers ordering Cologuard during Q3, which was a new record for the test. Exact continues to develop Cologuard and their next-gen Cologuard collection kit will prolong sample stability by 33%, which the company believes will help increase the number of completed tests by more than 1 percentage point next year. Not only is Exact considered the market leader, but the company is working on Cologuard 2.0 and a colorectal blood test, which will further defend their position as the market leader.

Second, colorectal cancer is the second leading cause of death from cancer in the United States, however, screening has helped drop mortality rates by 40%. Considering this, Cologuard should be seen as a preventative tool because it can help detect pre-cancer before it turns into CRC. As cancer screening becomes more of common practice, Cologuard should benefit from its position and from a growing market.

Indeed, it is possible that competition could challenge Cologuard in the coming years, but the company’s biggest threat, Guardant Health (GH), announced lackluster topline data for their Shield blood-based cancer screening test. Guardant reported an 83% sensitivity and 90% specificity. Meanwhile, Cologuard has superior sensitivity to detect 92% of colorectal cancers and 42% of pre-cancerous polyps. Guardant Health was considered to be one of Exact’s biggest threats, so the removal of that overhang has improved Exact’s long-term outlook.

Third, Exact is more than just colorectal cancer screening and has been working hard to broaden their offerings. Oncotype DX allows providers some of the tools needed to help them determine a cancer patient’s treatment. Riskguard is designed to help people recognize their inherited risks for getting cancer, as well as the genetic makeup of their tumor. Exact is planning on offering supplementary genomic tests to be used by patients, providers, biopharma companies, and academic partners. The company is also working on a multi-cancer early detection test which detected 61% of cancers at a 98.2% specificity in fifteen distinct organs, including 11 with no screening option currently available.

Fourth, Exact has impressive growth and profitability metrics. Exact has demonstrated its ability to summon growth with five-year average revenue growth of around 72%. In addition, the company’s gross margin of 73%, which is superior to the sector’s median of 55%.

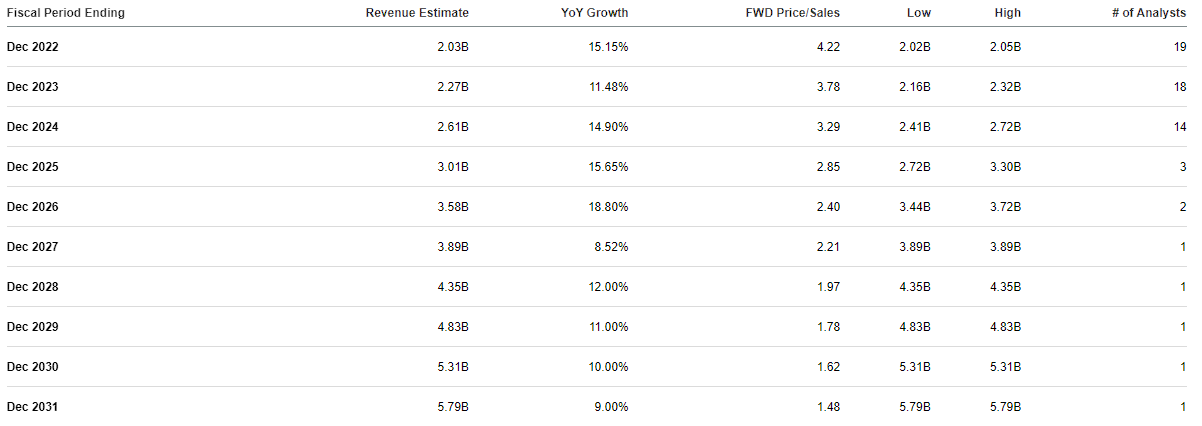

My fifth and final point is the ticker’s current valuation. EXAS is currently trading around a 4x price-to-sales for its estimated 2022 revenue of roughly $2B.

Exact Sciences Annual Revenue Estimates (Exact Sciences)

The sector’s average price-to-sales is around 4x-5x, so EXAS is trading at an acceptable valuation at this time. However, the company is projected to report strong double-digit growth for most of the remainder of the decade and finish 2029 with $4.83B in revenue… which would be a 1.78x forward price-to-sales. This would justify EXAS trading between $108 and $136 per share in 2029. Now, Cathie had EXAS hitting $140 in 2027, which the Street has the company pulling in around $3.89B, so it wouldn’t be outrageous to see EXAS trading around $140.

Considering the points above, I think it safe to defend ARK’s position here. All I see is Exact Sciences broadening and strengthening their foundation to become a leading presence in cancer diagnostics and hit their goal of profitability this year.

Managing My Shared Positions

It turns out Cathie and I have some similar interests in healthcare companies, such as Regeneron (REGN), Vertex Pharmaceuticals (VRTX), CRISPR Therapeutics (CRSP), Veeva Systems (VEEV) Pfizer (PFE), Schrödinger (SDGR), Twist Biosciences (TWST), Cerus Corp (CERS), Veracyte (VCYT), Fate Therapeutics (FATE), Pacific Biosciences of California (PACB), as well as Exact Sciences. Unfortunately, some of these tickers have been absolutely crushed during this prolonged market sell-off. Some of these tickers have been labeled a “Cathie Wood Stock”, which was once a hot momentum playback in 2020 and 2021… now, some of these have turned into Kryptonite and have dropped more than 50% over the course of 2022. EXAS was pummeled in the first have of 2022, but the selling pressure has subsided and is down roughly 37% over the past twelve months.

I have to admit that I have employed the same strategy as the market, and I have steered clear of adding to most of Cathie Wood’s speculative healthcare picks. Regardless of whether the company has made significant progress and reported growth, I have stayed away and have waited for the market to stop punishing ARKG and Cathie Wood’s small-cap and mid-cap healthcare tickers. Indeed, I don’t think the market is finished applying pressure to some of Cathie’s tickers, but I believe Exact’s improved fundamental outlook might have removed EXAS from the market’s “hit list.”

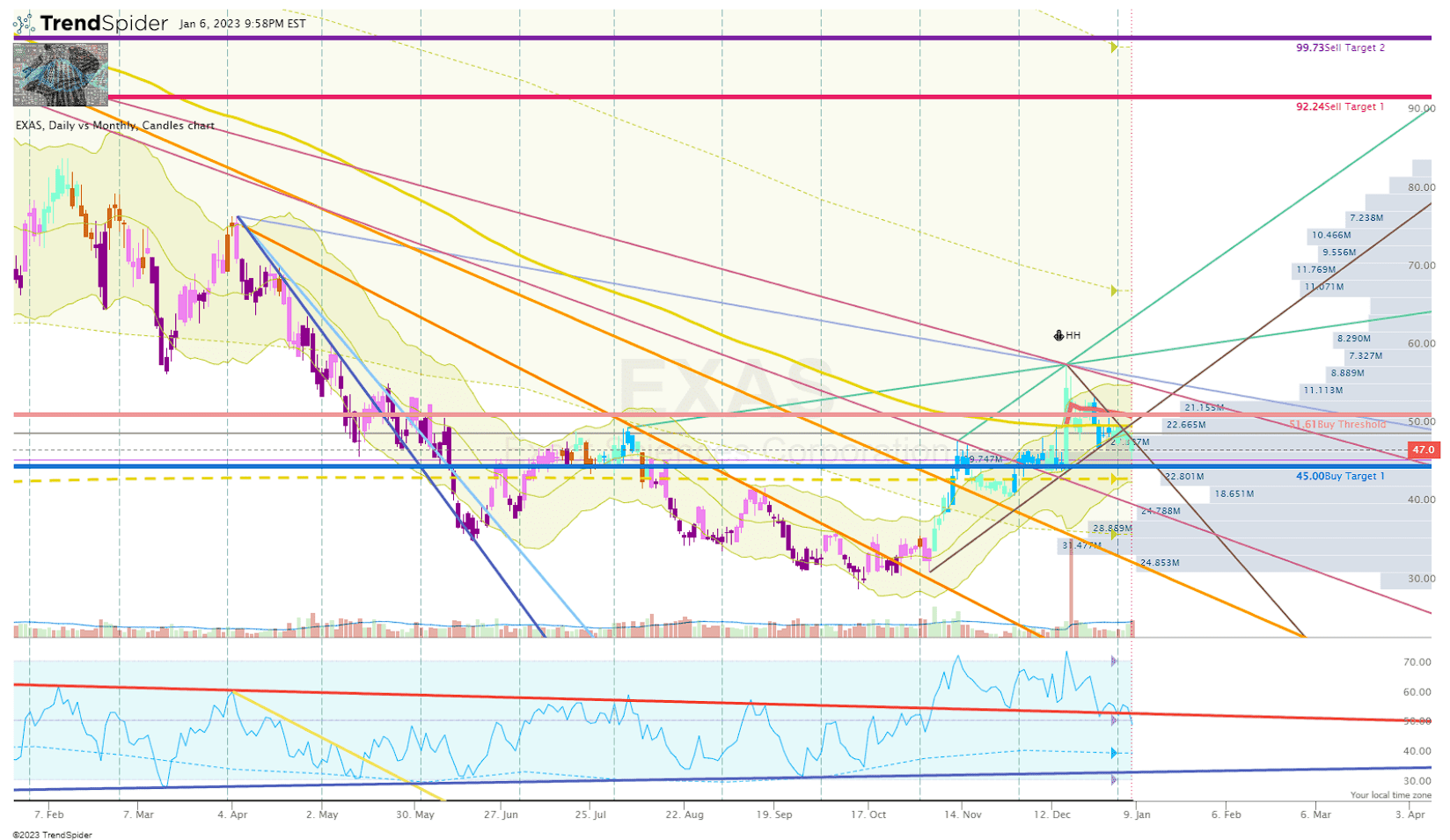

EXAS Daily Chart (Trendspider)

EXAS has found a new uptrend following their Q3 beat and saw a nice spike following Guardant Health’s update on their CRC blood test. EXAS climbed above my Buy Threshold, but has since dropped below and is approaching my Buy Target 1. The ticker has acquired a new downtrend ray from the mid-December high and has broken its uptrend from the Q3 earnings report. So, I am going to wait and see if we can hit my Buy Target 1 and reveal a new uptrend. If so, I will look to buy on a high conviction setup under my Buy Threshold.

Admittedly, I am not looking to “all-in” at this time… in fact, I am thinking I am going to take a cost-average approach over the course of 2023 with EXAS, and most of my “Cathie Wood stocks.” I might see things the same way as ARK is on EXAS, but I need the rest of the market to see it our way as well. As a result, I am giving EXAS a conviction rating of 3 out of 5.

Long-term, I am willing to see if ARK was right about $140 by 2027, and will plan on maintaining an EXAS position through 2027.

Be the first to comment