minemero

Overview

Everybody makes mistakes, even Starbucks Corporation (NASDAQ:SBUX). Maybe it’s just “optics,” but optics help to differentiate the commodity that each of us is selling. Our written record regarding Starbucks is available on our website, where we follow every publicly held restaurant company, and where our caution regarding Starbucks has been documented over the last five years.

Prologue Regarding The Rewards Program

We don’t have access to the reams of numbers that Starbucks’ management is provided that detail the spending habits of 29M U.S. Starbucks Rewards members. We have to believe, however, that our personal pattern of accumulating Reward points sufficient to get a free drink (usually larger than normal, since there is no size limit) is typical of most members.

Just a few years ago, it required 125 “stars,” spending $62.50, to earn a free drink. The free $6.00 vente soy latte amounted to almost a 10% discount spread across the total of eleven drinks. A couple of years ago, the requirement was increased to 150 stars, requiring $75.00 spent. The effective discount was reduced to about 8.7%.

The Latest Change In Necessary Rewards

Starbucks just announced that it is updating its loyalty program, starting February 13th, increasing the number of stars (from 150 to 200) to redeem select items (including hot drinks) for free.

There are other changes, with some reductions, but those apply to iced coffee and tea (not including cold brew beverages), packaged coffee, and select merchandise.

SO…….

Inflation, the cruelest tax, is affecting us all, and the marketing department at Starbucks, who has (understandably) done their share of raising prices, decides to throw salt into the wound by reducing the effective discount for Rewards members by 1.7 points. Safe to say that hardly any of the 28.7M Rewards members are now thanking Starbucks.

The Numbers

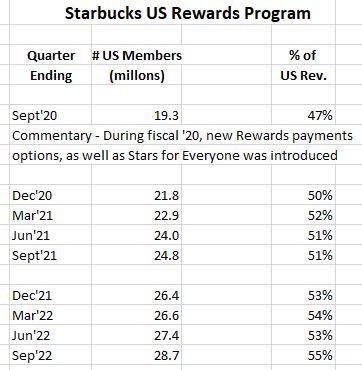

The table below shows how the number of U.S. active Rewards members has grown in the last two and half years, since new Rewards payments options, as well as Stars for Everyone was introduced.

To be sure, the number of members has increased by 48%, and the percentage of U.S. revenues that is generated by members is comfortably over 55%. In the near term, at least until this latest adjustment is digested, no pun intended, we suspect the growth in U.S. Rewards members will slow, and not just because of the law of large numbers.

Further Supporting Our Cautious Attitude – China, And Insider Trading Over The Last Twelve Months

We don’t claim to be an expert on China, regarding the politics, the economics, or the health care issues. However, it is safe to say that Starbucks’ largest growth market has more than its share of question marks. Whether it is the future of Taiwan, human rights issues, China’s role relative to the Russian/Ukraine situation, the role of the Yuan versus the U.S. Dollar in worldwide trade, or the ongoing possibilities of healthcare-related economic disruptions, Starbucks’ reliance on China for future growth does not suggest we should “pay up” for SBUX.

Furthermore, insider trading trends are watched closely by many investors, and the history over the last twelve months does not give us a warm feeling. As the table on our website shows, there have been a couple of recent notable sales, by a director and an international group president. The most notable material purchases within the last year were by the founder-billionaire Howard Schultz, the purchase worth millions but increasing his stake by only about 1%.

What To Do With SBUX?

Relative to the Rewards program, Starbucks’ management is too skilled to allow a misstep to become a major stumble. They have access to 28.7M U.S. customers, and they will somehow make amends. Still, loyal customers, including myself, did not need to wake up to this news. Some might even decide that they don’t need “their” Starbucks quite as often. Dunkin’, Horton’s, Dutch Bros, etc. also sell coffee, and the Keurig machine works pretty well.

More importantly, we have no problem calling Starbucks no better than a Market Perform or Hold due to: (1) Starbucks’ dependence on China for growth; (2) The premium price points in a sluggish word-wide economy that make it difficult to gain market share; and (3) The ongoing challenge, with tens of thousands of worldwide locations, to maintain and improve the operating culture that has been so crucial their success.

Roger Lipton

rewards program (private)

Be the first to comment