Alexey_Lesik/iStock via Getty Images

The share price of EuroDry Ltd. (NASDAQ:EDRY) has held up better than expected after a very weak earnings report that saw revenue plunge to $15.81 million, missing by over $5 million in the quarter.

Unfolding developments like rising interest rates, the economic slowdown, and a decline in port-related delays which has increased the availability of vessels points to ongoing challenges the company faces in 2023, and they aren’t going to go away in the near future.

Interestingly, even after the poor third quarter performance the share price of EDRY rebounded nicely from a double-bottom of approximately $13.45 per share at the end of October and early November, to trade at about $17.00 per share at the end of trading on January 6, 2023.

I think the reason for the share price holding up well is its huge plunge from its 52-week high of $44.99 on April 21, 2022, to its 52-week low of $12.71 on September 7, 2022, which resulted in a huge discount to NAV.

In this article we’ll look at some of it latest numbers, the effect of ongoing macro-economic weakness, and why I think the company is going to struggle in 2023 and may not get the rebound some are thinking it will because of the belief it’s undervalued at this time.

TradingView

Some of the numbers

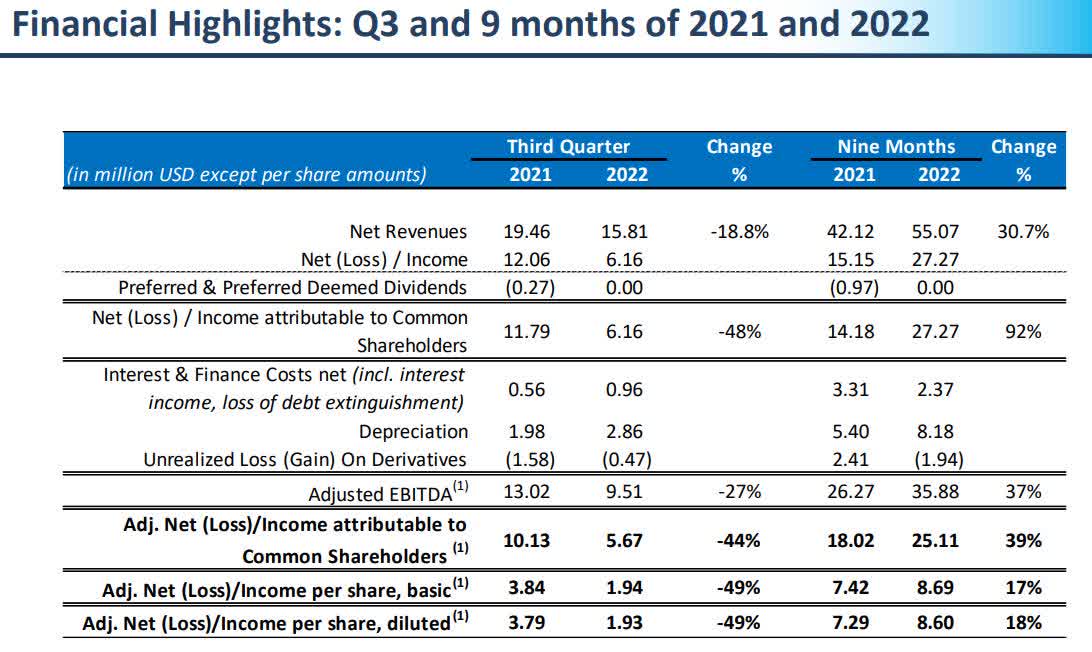

Revenue in the third quarter of 2022 was $15.81 million, down 18.8 percent from the $19.46 million in revenue from the third quarter of 2021. Revenue in the first nine months of 2022 was $55.07 million, up 30.7 percent from revenue of $42.12 million in the first nine months of 2021.

Net income in the reporting period was $6.16 million or $1.93 per diluted share, down 48 percent from net income of $11.79 million, or $3.79 per diluted share in the third quarter of 2021.

Investor Presentation

Net income for the first nine months of 2022 was $27.27 million, or $8.60 per diluted share, compared to net income of $14.18 million, or $7.29 per diluted share in the first nine months of 2021.

Adjusted EBITDA in the third quarter of 2022 was $9.51, down 27 percent from adjusted EBITDA of $13.02 in the third quarter of 2021. Adjusted EBITDA in the first nine months of 2022 was $35.88 million, up 37 percent from adjusted EBITDA of $26.7 million in the first nine months of 2021.

Taken together, the first nine months of 2022 looked good, but the bad news is it appears that is quickly changing, based upon the weak third quarter and headwinds contributing to its underperformance remaining in place. For that reason, 2023 looks to be a challenging year for EDRY.

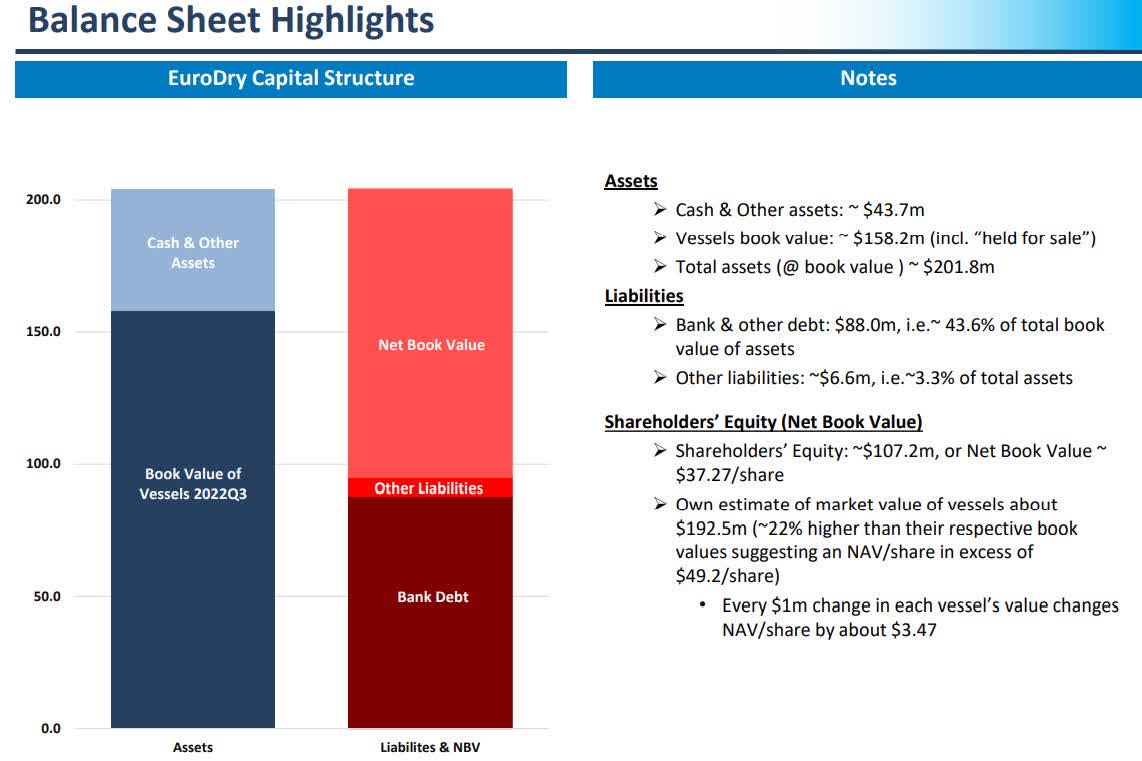

At the end of the third quarter of 2022 the company had cash and cash equivalents of $47.7 million, with debt of $88 million.

Investor Presentation

Headwinds and outlook

Over the last several years or so the need to replace shipping fleets has been one of the major tailwinds for the shipping industry, based upon the decline in the number of available vessels to ship products. Under normal conditions it would continue to be a tailwind, especially now that ordering new ships for deliveries in 2023 and 2024 are close to zero, according to EDRY management.

With the orderbook at about 3.4 percent for 2023 and 2.2 percent for 2024, the size of the overall fleet is expected to decline because of the scrapping of some vessels. Again, under normal conditions this would be a tailwind because of higher shipping costs associated with supply and demand, but the supply and demand picture going forward, at least for 2023, lacks visibility, and the working assumption at this time is the first half will probably remain under pressure on the demand side, and may improve in the second half of 2023 if the economy rebounds.

EDRY management isn’t convinced which way the shipping market will head in 2023 because of lack of certainty concerning the strength of the global economy, the unknown outcome of the war between Russia and Ukraine, and how the Chinese economy in particular does in 2023. Concerns in China are primarily in regard to its real estate sector.

The main effect of the weak real estate sector in China is the resultant drop in demand for steel, and by extension, iron ore. China’s real estate sector accounts for approximately 30 percent of its GDP.

What’s important to takeaway is even if the shipping fleet in the overall reduces in size, declining demand will mean even if shipping prices move higher, there’s not as much money to be made if there’s a lot less product to deliver. Another factor is higher interest rates have had an impact on commodity demand as well as freight rates.

On the competition side of things for EDRY, with much of port congestion being relieved, it’s bring back more players into the market, which could put downward pressure on prices. One positive catalyst in the shipping sector, specifically with sub-Capesize vessels, is the increased demand for coal associated with the existing energy crisis.

Cash flow breakeven rate

In the third quarter of 2022 the daily cash flow breakeven rate was $13,984, compared to $9,992 per vessel per day in the third quarter of 2021.

The reason for the significant increase in the daily cash flow breakeven rate was an increase in loan repayments and higher dry docking costs.

Excluding dry docking costs total operating expenses in the quarter were $6,587 per vessel per day, compared to operating expenses of $6,510 per vessel per day in the third quarter of 2021. The takeaway there is the company remains disciplined with its operational spend, and is basically flat year-over-year with the exception of the big increase in dry docking prices.

For the first nine months of 2022 cash flow breakeven was $12,961 per vessel per day, compared to cash flow breakeven per vessel per day of $10,456. The reason for the increase was the increase in dry docking costs paid and higher loan repayments.

From the time of the earnings report, the company guided for cash flow breakeven rate to be at approximately $13,550 per vessel per day.

Combined with a weak charter rate environment and an uncertain economic and geopolitical environment in 2023, I think EDRY could be in for a tough year.

Investor Presentation

Conclusion

I think 2023 is likely to be more of a regrouping year for EDRY, based upon expected elevated dry-docking costs, an unfavorable charter rate environment, and the strong possibility demand will be subdued, especially in relationship to the Chinese market.

The major question investors must answer for themselves is: has the company reached a bottom yet or is there more to come, considering how far the stock has dropped since April 2021?

If the global economy comes under more pressure and Chinese demand continues to be weak, the company is going to struggle to find near-term tailwinds, and if it shows more revenue and earnings weakness going forward, its share price is going to get punished more.

Unless something far worse in the global economy unfolds, I don’t think the share price of EDRY is going to get crushed, but it could test its 52-week low, or even $10.00 per share if the next earnings report reveals more weakness in the company.

At this time management considers the best deployment of capital would be to buy back its stock, because of it low entry point. With the sale of its Panamax dry bulk carrier, the company feels it’ll provide the liquidity need to buy back shares.

And while it’s looking at potential vessel acquisitions under the right circumstances, it doesn’t seeing that as the best way to spend at this time because of the favorable share price presented to it.

A positive for investors is expectations for the company’s performance is low at this time, as evidenced by its share price, but if there is a correction in the stock, it could provide an extraordinary opportunity to take a position at a cost basis that would be hard to match in the years ahead.

I think over the long-term EDRY should be a solid holding for patient investors, over the next year it looks like it doesn’t have the tailwinds to push the share price up.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment