alvarez

Quick Recap

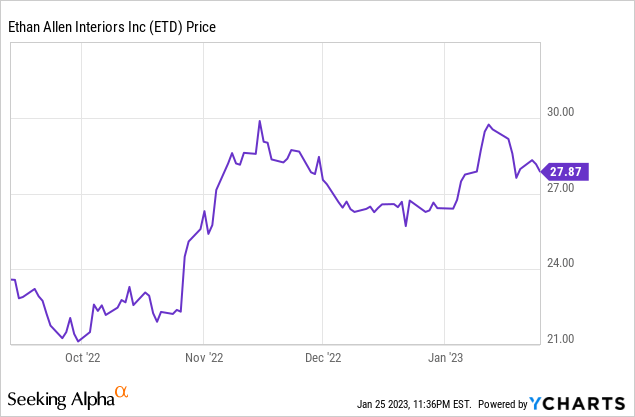

We initiated a “BUY” rating for Ethan Allen (NYSE:ETD) on September 13th, 2022 based on strong financial performance, strong brand, and steady dividend distributions. Shares are up ~20% since the publication of the initial coverage writing. The stock at the time of this writing is delivering higher returns than the stock market on a year-to-date basis. We are reiterating our “BUY” rating based on strong Q2 earnings results and the continued attractiveness of the dividend yield.

Q2 2022 Earnings

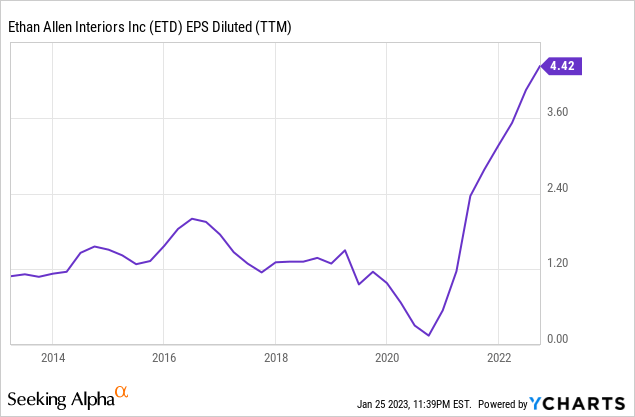

For Q2 2022 earnings, the company reported $1.10 per share, which is higher than a publicly reported consensus estimate of $0.89 per share. The 23.60% earnings surprise have sparked a modest rally in the stock price since the earnings announcement. Though on a year-over-year basis, the revenue has declined 2.4%, we do not believe it affects our thesis as long as the bottom line remains strong to support our dividend-based thesis. The diluted EPS actually saw a 16% increase on a YoY basis, thanks to increase in gross margin and better cost efficiency. Taking a step back, the company’s six month revenue performance is 7.0% higher than the six month figure from a prior year, so we believe that the minor decline in the year-over-year earnings for Q2 is not a big issue. Furthermore, economic conditions have deteriorated in the last few months, and we believe that such a minor decline on a YoY basis given this colder economic climate is a positive sign of the company’s resiliency.

Reaffirmation of Thesis

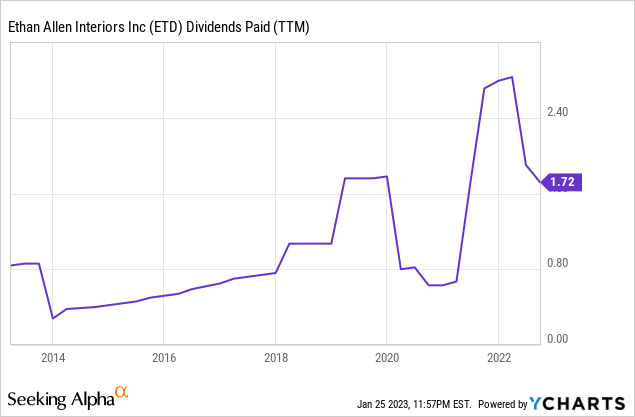

Our thesis centered around the company’s profitability and its ability to pay out its dividends sustainably during times of economic uncertainty. The company has continued to remain committed its shareholder return program, and the company paid out another dividend of $0.32 per share in last December. At current levels, the annualized dividend yield stands at 4.62% which is far higher than S&P 500’s dividend yield of 1.67% and U.S. 10Y treasury yield of under 3.5%. This metric excludes special dividends that the company pays out to shareholders, such as the $0.50 per share that the company paid out in the middle of last year. Though volatile, the dividend compensation is likely to be higher from the current annualized figures due to its history of special dividend payouts.

Strong Balance Sheet

Furthermore, the balance sheet remains strong, as the company reported a cash balance of $140.4 million compared to $121.1 million at the end of June 30, 2022. The high cash balance and the continued profitability of the business makes this a fairly attractive dividend investment in our view. Not only that, the company has no debt outstanding. Compared to indebted companies with high leverage and interest rate burden, ETD has a robust balance sheet that can help sustain its operations, shareholder programs, and uncertain economic environment. We believe that ETD remains a great investment for income-oriented investors who would like exposure to equity upside.

Gordon Growth Model

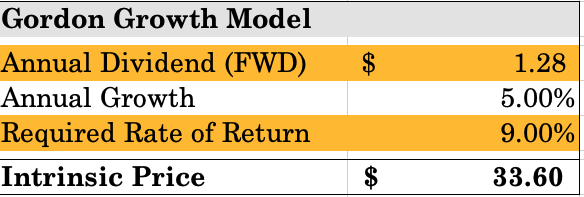

To reflect the higher interest rate environment and more modest growth scenario of its dividend program, we have updated our Gordon Growth Model using a baseline assumption scenario, where compared to the previous model, we lower annual growth expectations and increase the RRR based on marginally higher rates. We believe 5.00% growth is more than achievable given in the last 3 years, the quarterly dividend growth has been growing at a 19% CAGR from $0.19 per share in 2019 to $0.32 per share in 2022. These assumptions have provided us with an intrinsic price of $33.60 per share, which still represents 21% upside from current levels.

Sweet Minute Capital Valuation

Conclusion

Our update based on Q2 2022 earnings re-affirm our “BUY” rating and we believe that the investment will continue to provide predictable and stable dividend distribution for the coming years regardless of the economic environment. The recent beat in earnings expectation should lend further confidence in the company’s business operations, and more faith in management’s continued commitment in its dividend program for shareholders.

Be the first to comment