Bulgac/E+ via Getty Images

With its ninety years of existence, Ethan Allen Interiors, Inc. (NYSE:ETD) has been through a lot of highs and lows. It has withstood various market challenges, making it a durable industry contender. In the last two years, it has stayed thriving amidst changing market dynamics.

Today, Ethan Allen shows well-maintained viability and fundamental stability. Although its demand has softened, revenues and margins stay manageable. Lower revenues may take place as overall market demand normalizes. Thankfully, furniture companies, such as ETD, have sustained their inventory recovery. Supply is catching up with demand, so supply chain management may become easier. Also, Ethan Allen maintains an excellent liquidity position to cover its production capacity. It also maintains adequate core returns to cover borrowings. With that, it remains well-positioned against market headwinds. It can sustain its operations without increasing its financial leverage further.

Moreover, ETD stays consistent with dividend payouts, making it an enticing dividend stock. However, the stock price appears too high to reflect its intrinsic value.

Company Performance

The household durable industry has been through disruptions in the last two years. Things started with pandemic restrictions that led to a deep recession. Despite this, it proved to be more resilient than many others by regaining its footing in a short period. Thanks to price drops, real estate boom, and changing work setups. Today, Ethan Allen shows it can rise above disruptions and exceed pre-pandemic levels.

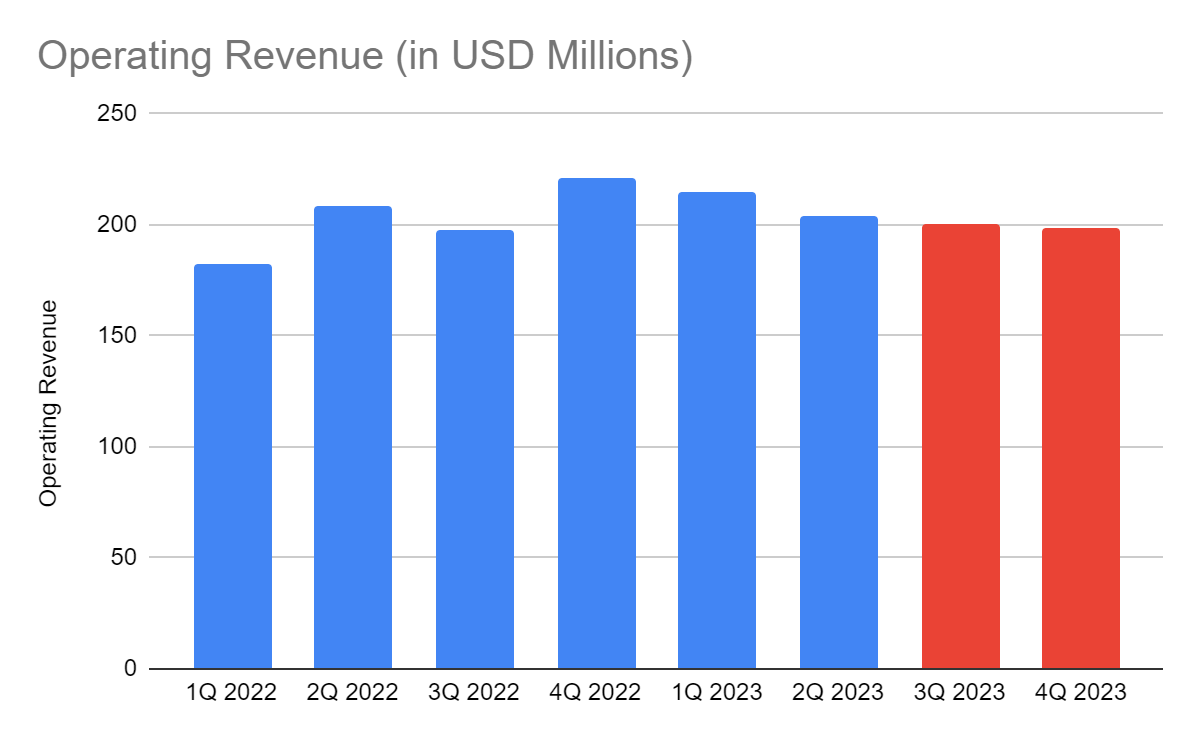

The operating revenue amounts to $203.2 million, an 11% year-over-year increase. It’s great to see a company stabilizing revenue growth amidst the softening of demand. We can see it in the sequential decrease since 4Q 2022. As such, we must focus on its near-term performance and the potential changes in the second half of FY 2023.We can attribute the sequential downtrend to several factors. First, inflation has been reflected in the core operations as it set a new all-time high in forty years. It eroded the purchasing power of many consumers, especially in the US and Canada. These two countries were some of those first hit by inflation. Fuel prices also put pressure on transporting and processing raw materials. Fortunately, the US, Canadian, and China markets now have a more stable inflation lull. The challenge is that some international markets have a slower inflation reaction. It may cause inconsistency in sustaining its growth potential. Hard lockdowns in China may also have an impact since about 30% of its design centers are located there. We can also expect the cooling home demand to affect furniture and home furnishing sales. Home sales decrease has become more evident during the second half of 2022. As such, the demand for

Operating Revenue (Ethan Allen 3Q Report And Author Estimation)

Amidst all these, the company maintains the balance between growth and stability. It is one of the integral attributes for evaluating its performance. What makes Ethan Allen a solid company is the fact that it focuses on aspects it can control and improve. First, we can see it in its strategic pricing that makes up for the lost demand. Doing so helps its operations become more flexible to market volatility. Second, it has evident flexibility when it comes to inventory management. It remains careful amidst supply chain bottlenecks by not carrying too many inventories. So now that demand softens, it can adjust production volumes and avoid overloading. Today, it sees the end of industry backlogs as inventory levels improve. It can concentrate on setting favorable prices and cost-reduction strategies. It may also increase its spending on promotion and innovation.

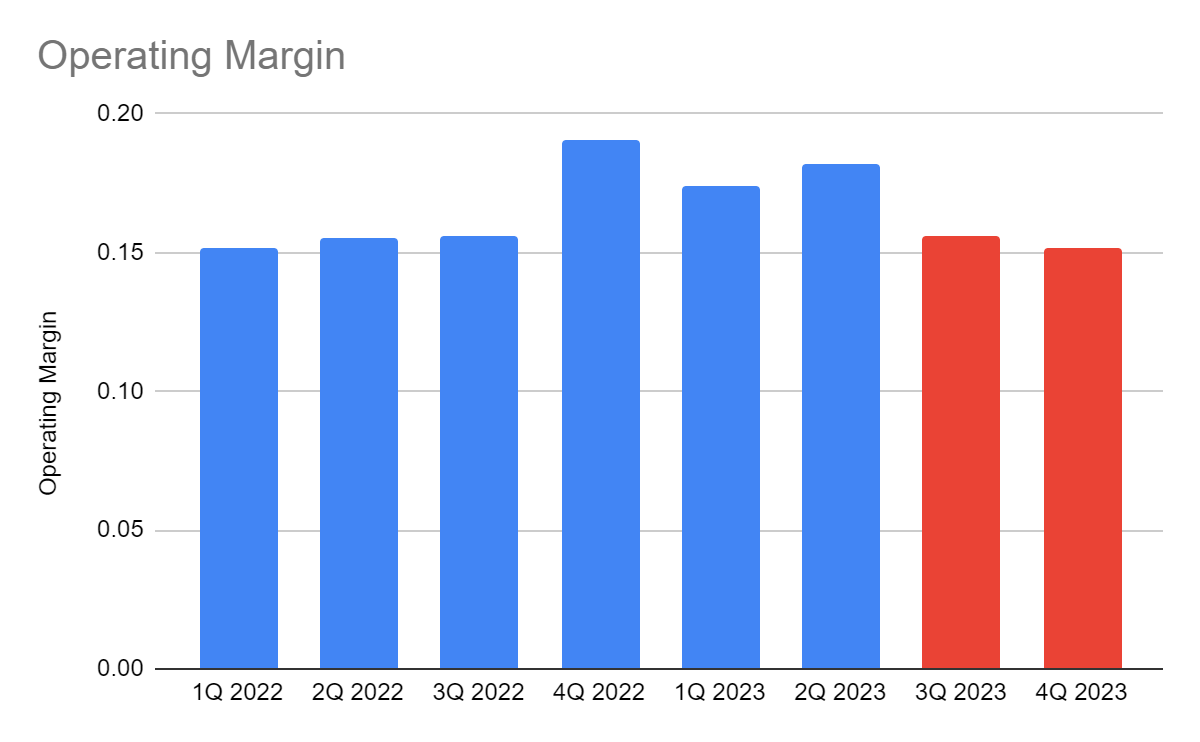

Moreover, Ethan Allen keeps its costs and expenses manageable despite the elevated prices. It improves operational efficiency to offset revenue decreases. So, it matches the pricing strategy of the company. And these adjustments prove sufficient as the viability of core operations is increases. Its operating margin is stable at 18.2% compared to 15.1% in 2Q 2022 and 17.4% in 1Q 2023.

This year, I expect more normality and seasonality in business patterns. Near-term growth may be lackluster, but ETD can maintain operational stability. As inflation keeps decreasing, transporting and processing inventories may be less costly. As ETD regains a firm hold of supply chains, it may do cost-reduction strategies better. I expect second-half revenues to decrease as demand normalizes. But it may remain decent, given its agile pricing and production capacity adjustment. So while I expect growth to cool down, it may stay viable through more stable costs and expenses.

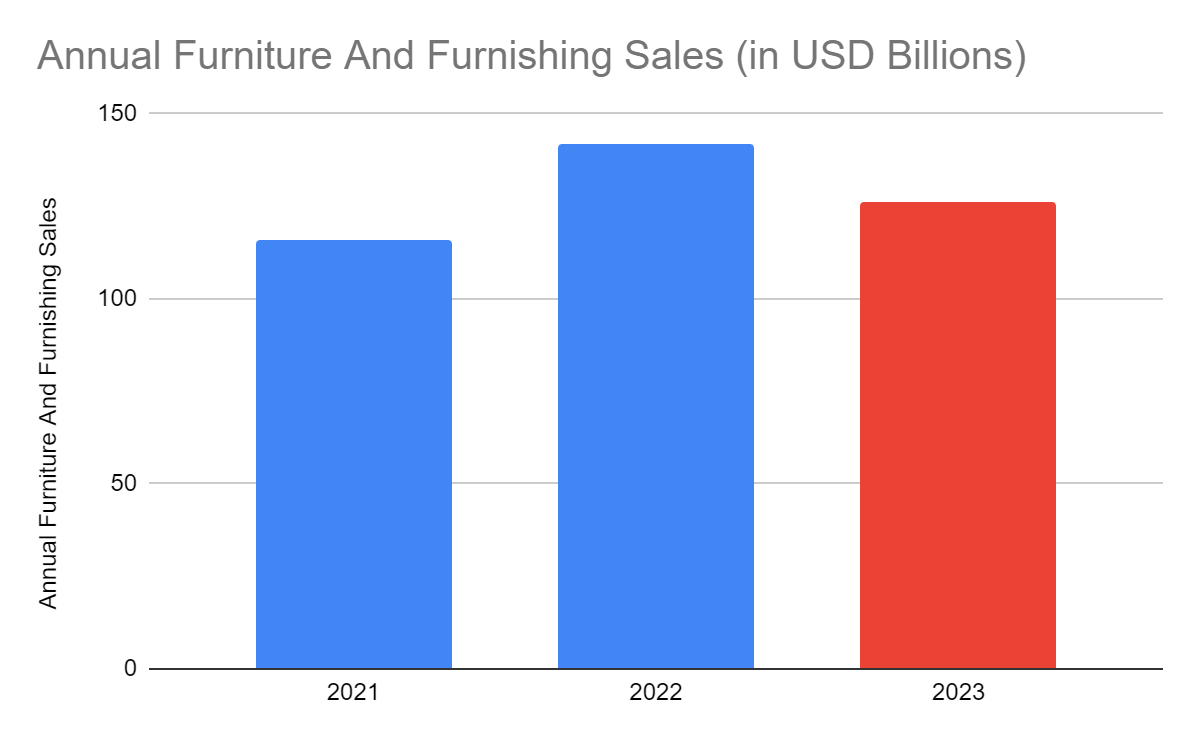

What matters is that the company remains consistent with current industry trends. In 2022, the US furniture and home furnishing sales are 1.6% higher than in 2021. November and December sales are yet to be added, so its annual value may reach $142 billion. But given the recent downtrend, sales may decrease this year but still higher than in 2021. I expect industry sales to normalize at pre-pandemic levels. But ETD must work double on promotion amidst the rise of smaller online retailers.

Operating Margin (Ethan Allen 3Q Report And Author Estimation)

How Ethan Allen Interiors, Inc. May Fare In FY 2024

Ethan Allen Interiors, Inc. remains a durable household durables provider. In over ninety years, it has gone through market crests and troughs, making it a safe stock. However, it must be careful, given the market dynamics that may become overwhelming. Thankfully, inflation keeps cooling down, landing at 6.5%, nearly 30% down from its peak. While I don’t wish to downgrade the potential recession, I am more on the optimistic side. After all, the changes that have transpired in the last year were part of the economic rebound. Inflation has been driven by pent-up demand, not by cost-push factors. Even better, low unemployment means the picture differs from the Global Financial Crisis. Inflation lull and improved income levels may stabilize purchasing power and market demand.

Annual Furniture And Home Furnishing Sales (FurnitureToday)

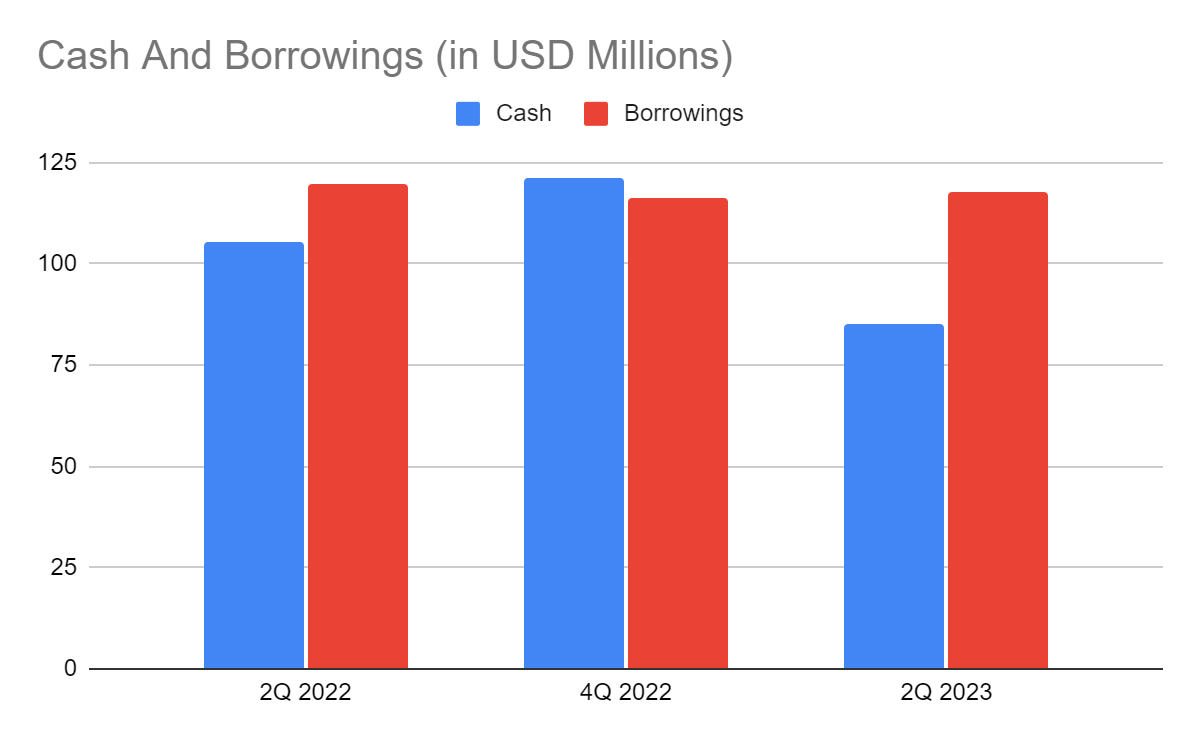

We covered parts that show why ETD is solid despite the lower projections. Again, its well-managed inventory can help it adjust to the moderating market demand. Liquidity is its primary cornerstone. Its cash reserves remain high and adequate. The Net Debt/EBITDA Ratio remains low at 0.44x, so the company earns more than enough to cover borrowings. It is a vital aspect to consider since it belongs to a capital-intensive industry.

Cash And Equivalents And Borrowings (Ethan Allen 3Q Report)

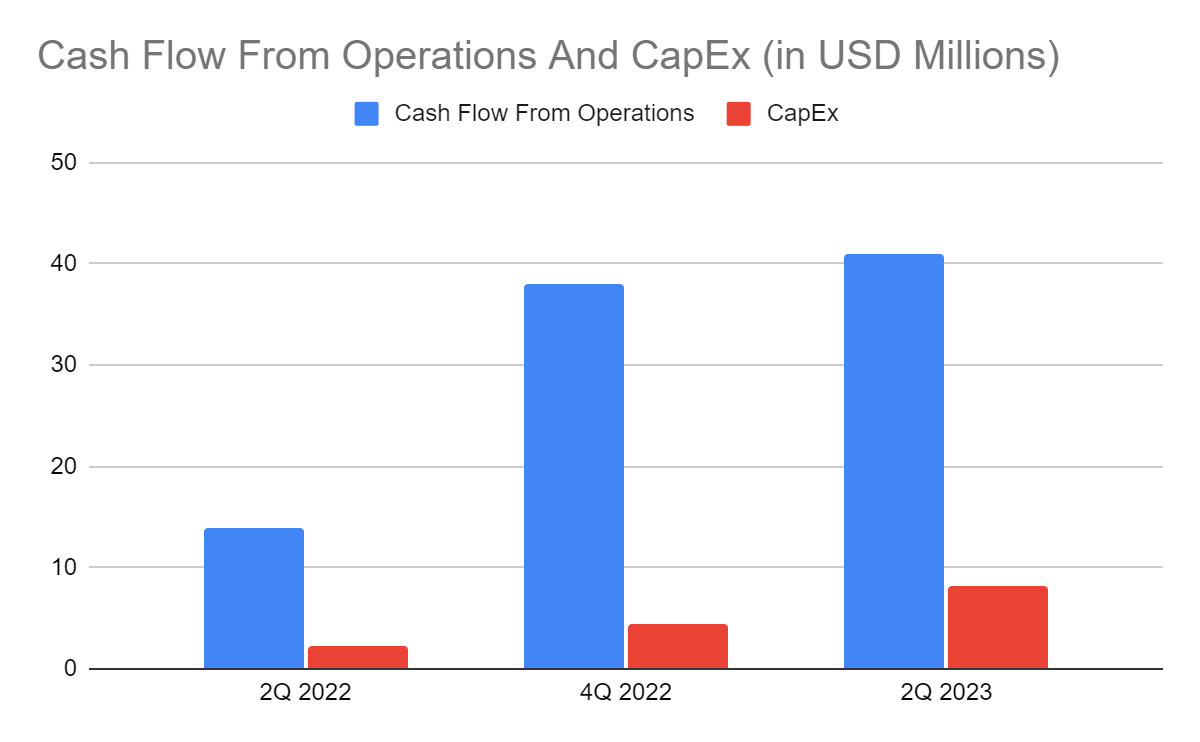

Our liquidity impression can be confirmed by its cash flow from operations. Its Cash Flow of $ is more than thrice its value last year. With that, it shows stable and higher cash inflows this quarter. It is also more than thrice its CapEx of $. With that, its FCF stays enough to cover borrowings and dividends. It makes cash levels high enough to increase its intrinsic value by buying back shares. The FCF/Sales Ratio is way higher than in 2Q 2022. It shows a massive improvement in turning revenues into cash. Given this, Ethan Allen maintains the balance between growth and fundamental stability.

Cash Flow From Operations And CapEx (Ethan Allen 3Q Report)

Stock Price Assessment

The stock price of Ethan Allen Interiors, Inc. has been in a sustained uptrend. It should not be surprising since it stays consistent with the fundamental trend. At $27.79, it is 21% higher than its value last year. However, the uptrend seems to have exceeded its intrinsic value. The price-earnings multiple is 6.3x and my estimated EPS of $4.26 gives a target price of $26.83. NASDAQ is less pessimistic with its estimated EPS of $3.54, which gives a target price of $22.30. Projections using the tangible book value show the same valuation. Its current TBVPS is 15.44, leading to a PTBV of 1.65x. If we use the average PTBV of 1.57x in recent years, the target price will be $24.24. The EV Model ($ 690 M – $ 30 M) / 25,348,000 shares = agrees with $27.22 as the target price.

Despite this, it remains an enticing dividend stock, given its yields of 4.55%. It is way higher than the $&P 600 average of 1.24%. Payouts are also well-covered, given the dividend payout ratio of 26%. To assess the stock price better, we will use the DCF Model.

FCFF $30,400,000

Cash $85,400,000

Borrowings $117,800,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 348,000,000

Stock Price $27.78

Derived Value $26

The derived value agrees with the other estimations showing potential overvaluation. There may be a 7% upside in the next 12-18 months. Investors must practice extra caution before buying shares.

Bottomline

Ethan Allen Interiors, Inc. stays a solid company this quarter. Its core operations remain stable and viable to cushion market disruptions. It also has impressive liquidity to cover its operations even during a recession. It maintains an adequate capacity to repay its borrowings. It can also sustain dividends with enticing yields. However, the stock price appears to be quite high for its intrinsic value. The uptrend is consistent with its impressive fundamentals but overvalued. Investors may wish to wait for an ideal entry point before making a position. The recommendation, for now, is that Ethan Allen Interiors, Inc. is a hold.

Be the first to comment