MarsBars

Net lease REITs are a favorite asset class for many income investors, and for good reasons. This segment is well known for providing steady income and high operating margins, due to passing of costs such as property maintenance, tax, and insurance to tenants.

While Realty Income (O) and W.P. Carey (WPC) are popular favorites, lesser followed REITs such as Essential Properties Trust (NYSE:EPRT) provide a better valuation and faster growth profile due to their smaller nature. In this article, I highlight why EPRT presents a buying opportunity at present for long-term income and growth.

Why EPRT?

EPRT is a self-managed REIT that owns and manages single-tenant net leased properties with long-term leases. At present, it has a portfolio of 1,572 freestanding net lease properties and is well diversified by geography, with a presence in 48 states.

As its name suggests, EPRT’s diversified tenant base is comprised of industries that are essential in nature. As shown below, no one industry makes up more than 14% of EPRT’s annual base rent, with early childhood education, quick service restaurants, medical / dental, car washes, and auto service comprising 57% of EPRT’s ABR.

EPRT Tenant Industries (Investor Presentation)

Meanwhile, EPRT demonstrates strong portfolio fundamentals, with a 99.8% leased rate, and its leases are longer in duration than its net lease peers, at 14 years weighted average remaining term. EPRT’s tenant base also appears to be rather healthy, with an average unit-level rent coverage of 4.2x.

Plus, most of its properties (87% of ABR) was acquired through sale-leaseback transaction, which means that the tenant has had prior experience in running the property, and 64% of ABR is from master leases. As an added safeguard, EPRT receives unit level reporting from 99% of its properties, which means that it can address issues with a problem property before problems get bigger.

Moreover, EPRT is seeing healthy growth, as FFO per share rose by 6% YoY to $0.38 in the third quarter, driven in part by investments and asset recycling, including 40 property acquisitions and 12 dispositions. The acquisitions come with a weighted average cash and straight-line cap rates of 7.1% and 8.2%, which sit comfortably above EPRT’s cost of capital.

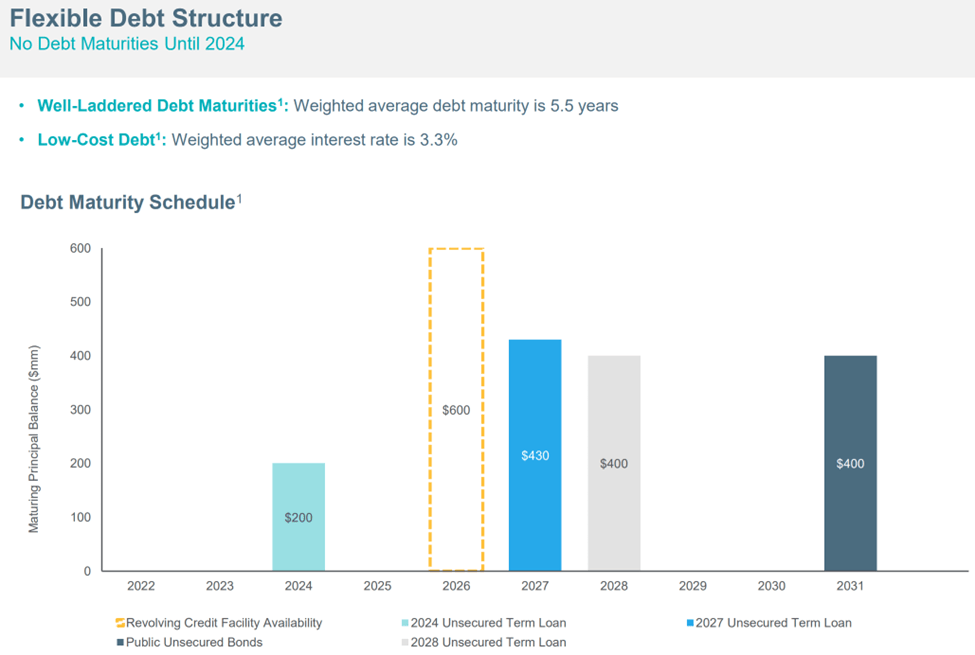

Potential headwinds include higher interest rates, which may pressure EPRT’s cost of capital. This risk is mitigated, however, by EPRT’s strong balance sheet with a net debt to EBITDA ratio of 4.4x and $900 million of available liquidity. In addition, EPRT maintains well balanced debt maturities, with 100% fixed rate debt and no debt maturing until 2024, as shown below.

EPRT Debt Maturity Schedule (Investor Presentation)

EPRT continued its strong momentum during the fourth quarter, as management highlighted in a pre-earnings update. This includes $328 million worth of investments at an even higher initial cash yield of 7.5%, and EPRT’s pipeline carries an attractive 7.6% cash yield. As such, it appears EPRT is well-positioned to take advantage of an attractive buyer’s market, as overleveraged property owners pressured by higher interest rates seek to unload assets.

Importantly, EPRT pays a respectable 4.5% dividend yield that’s well-covered by a 72% payout ratio, based on Q3 FFO per share of $0.38. EPRT also has a decent track record of raising its dividend payout every year since IPO in 2018, and this includes 2 dividend raises in 2022. Looking forward, I would expect for annual dividend growth to be in the 5% range, which would be in line with long-term FFO per share growth expectations.

Turning to valuation, EPRT is no longer cheap at its current price of $24.38. However, we can’t turn back the clock and I continue to find the P/FFO valuation of 15.5 to be attractive, considering the quality of EPRT’s strong balance sheet, operating fundamentals, property profile, and forward outlook. Plus, analysts have a consensus Buy rating on the stock with an average price target of $26.

Investor Takeaway

EPRT is a high-quality and fast-growing self-managed REIT that owns a well-diversified net leased portfolio in essential industries. It’s also demonstrating respectable growth in the current environment and is well positioned to consolidate the fragmented net lease segment with its strong balance sheet, particularly as overleveraged property owners seek to sell at high cap rates. Lastly, EPRT pays a respectable and well-covered dividend and appears to be a solid choice for dividend growth investors seeking a reliable income stream.

Be the first to comment