yujie chen/iStock Editorial via Getty Images

In our initiation of coverage, we were not particularly optimistic about Erste Group Bank AG’s future (OTCPK:EBKOF, OTCPK:EBKDY). Looking at the company’s fundamentals, the Austrian-based bank is very well-managed and is delivering solid results, however, our main concerns were due to the ongoing macroeconomic challenges. Already at that time, energy price developments and Europe’s GDP forecast were in our minds. Since our neutral rating, Erste’s stock price declined more than 30%. Today, following the just-released debt update, our internal team is back to analyze the bank’s performance and its long-term financial implications.

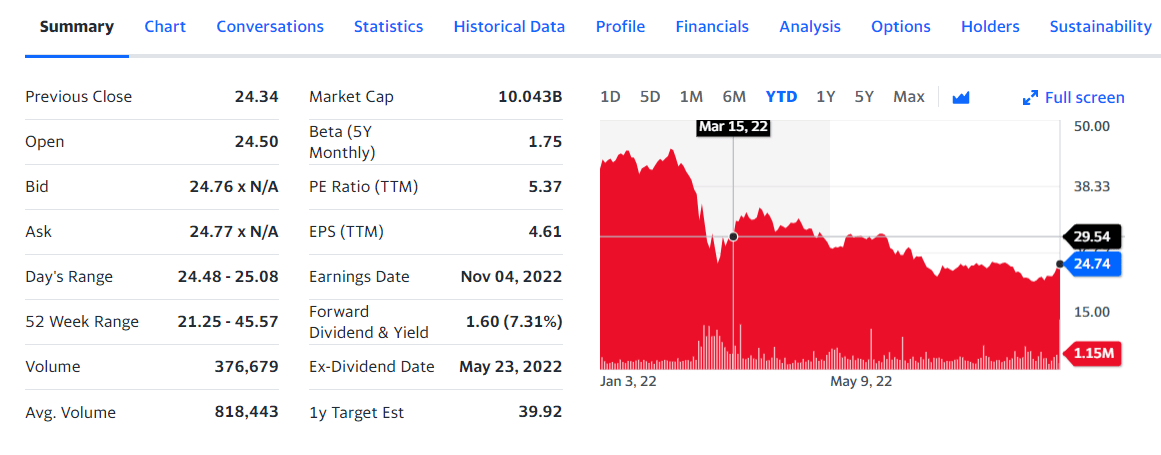

Erste’s stock price development

Source: Yahoo Finance

Looking ahead the Q2 results

In the first semester, the company reported strong numbers. Briefly, we can say that there was a positive pricing delta supported by an early rate hike in many countries where Erste operates. Indeed, net interest income and fees increased more than operating costs. As a result, Erste’s cost/income ratio further decreased reaching 55.1% from 55.5%. Looking at the solvency ratio, the bank CET 1 and the NPL reached respectively 14.2% and 91.8% coverage.

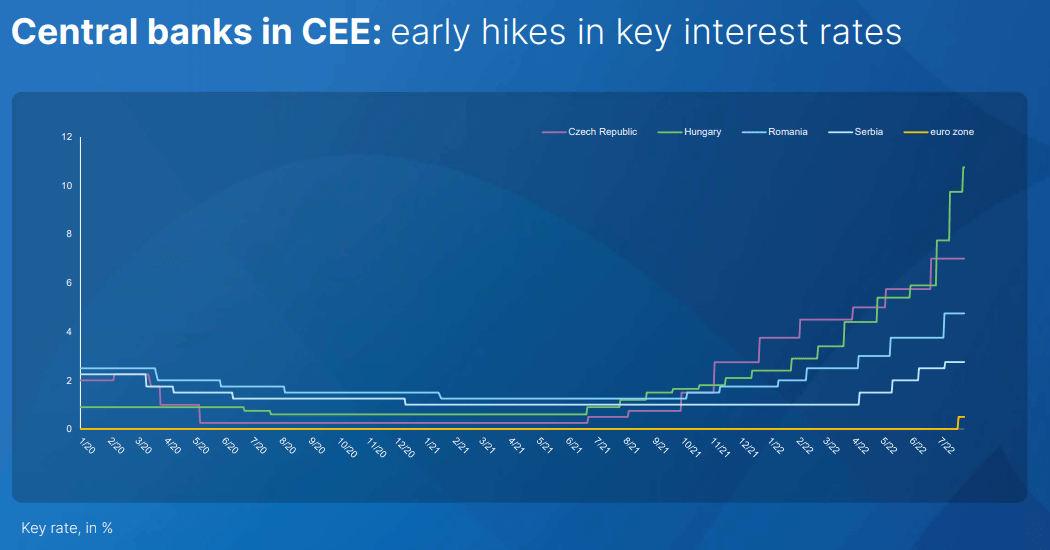

Rate hikes evolution

Source: Erste Q2 results

Aside from the good set of numbers, Erste’s forward-looking outlook is based on the expectation that Russia won’t stop gas supplies in Europe and the ECB will continue to support rate hikes. Just yesterday, the ECB raised interest rates for the second time by 75 basis points (50 basis points was the increase that happened in July), and now there is a question that haunts the market: how much will it raise them next time? According to rumors, another increase of 75 points will happen in October. Our internal team believes that the ECB is lagging behind in its path of rate hikes towards neutrality. In some cases, ECB forecasts have already proven to be wrong and this was confirmed by Lagarde’s speech at the end of yesterday’s meeting. While Frankfurt expected stagnant growth in the winter months, she acknowledged that many of the downside risks of this outlook have already materialized. For instance, consider in particular the Russian gas access and the increasing risk of a downturn (We believe that the Euro area is already in recession).

Conclusion and Valuation

Looking at the aggregate European banks, tangible book value is around 0.7x and we are confident that Wall Street is already implying a recession case scenario. However, almost 75% of the European banks (even looking at our modest universe coverage) delivered higher numbers than consensus expectation thanks to rising interest rates and strong asset quality. The bank’s profitability is lowering the whole sector’s Price Earnings ratio versus a historic low both at absolute value (6.3x vs. 5.6x during the financial crisis) and at relative value (2.4x discount vs. 3.1x recorded in 2008). Dividend yields are also at a historic high. Concerning the valuation and given the stock price decline, we are inclined towards a buy rating. Based on a 2023 expected RoTE, we value the Austrian-based bank at €30 per share. However, in our banking coverage, there are players with higher dividend yields and credit solvency ratios. Credit Agricole is a clear example.

Be the first to comment