Ultima_Gaina/iStock via Getty Images

Investment Thesis

Ero Copper Corp. (NYSE:ERO), a mining company headquartered in Vancouver with operations in Brazil, has ambitious growth plans that if realized will allow it to capitalize on the soaring demand for copper, considered by many as indispensable for transitioning to a green global economy. With relatively high long-term growth estimates and a P/E ratio of 5.2 (as of 9/25/22), the stock would normally represent a no-brainer bargain. However, momentum matters.

The stock’s dramatic (and somewhat baffling) underperformance versus the S&P 500 and its direct competitors – in addition to near-term headwinds – are causes for concern. In the long run, we believe this stock will bounce back in a big way. However, any turnaround is unlikely to happen by year-end given unprecedented exposure to copper prices on the international market due to operational issues at Ero’s primary domestic customer. Not to mention, because it pays no dividend, the stock does not represent any refuge in a storm. Although we still think the stock is a buy, it is for these reasons the rating comes with great caution.

This article will first look at Ero Copper’s growth prospects and valuation relative to the market before exploring near-term headwinds.

Growth & Valuation

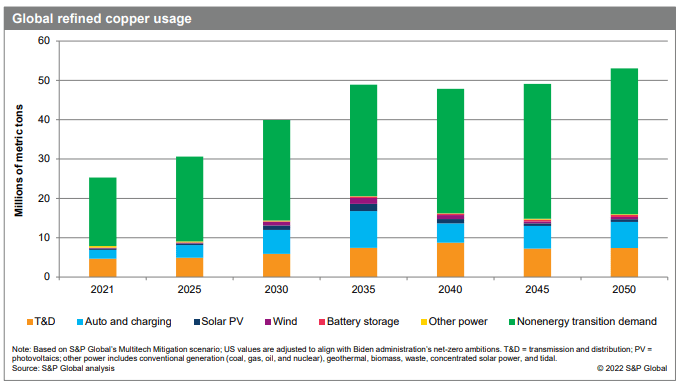

Reaching net-zero emissions by 2050, a target set by more than 70 countries, will require a rapid switch to electric vehicles (EV) and renewable electricity on a scale that will send copper demand surging to new heights. S&P Global in a July study projects that the demand for copper, the “metal of electrification,” will double by 2035 as the world attempts to pull off this green energy transition.

Copper Demand Forecast 2021-2050 (S&P Global)

Supply forecast scenarios suggest that the world could see a shortfall ranging from 1.6 million metric tons (mmt) to nearly 10 mmt as demand reaches close to 50 mmt by 2035.

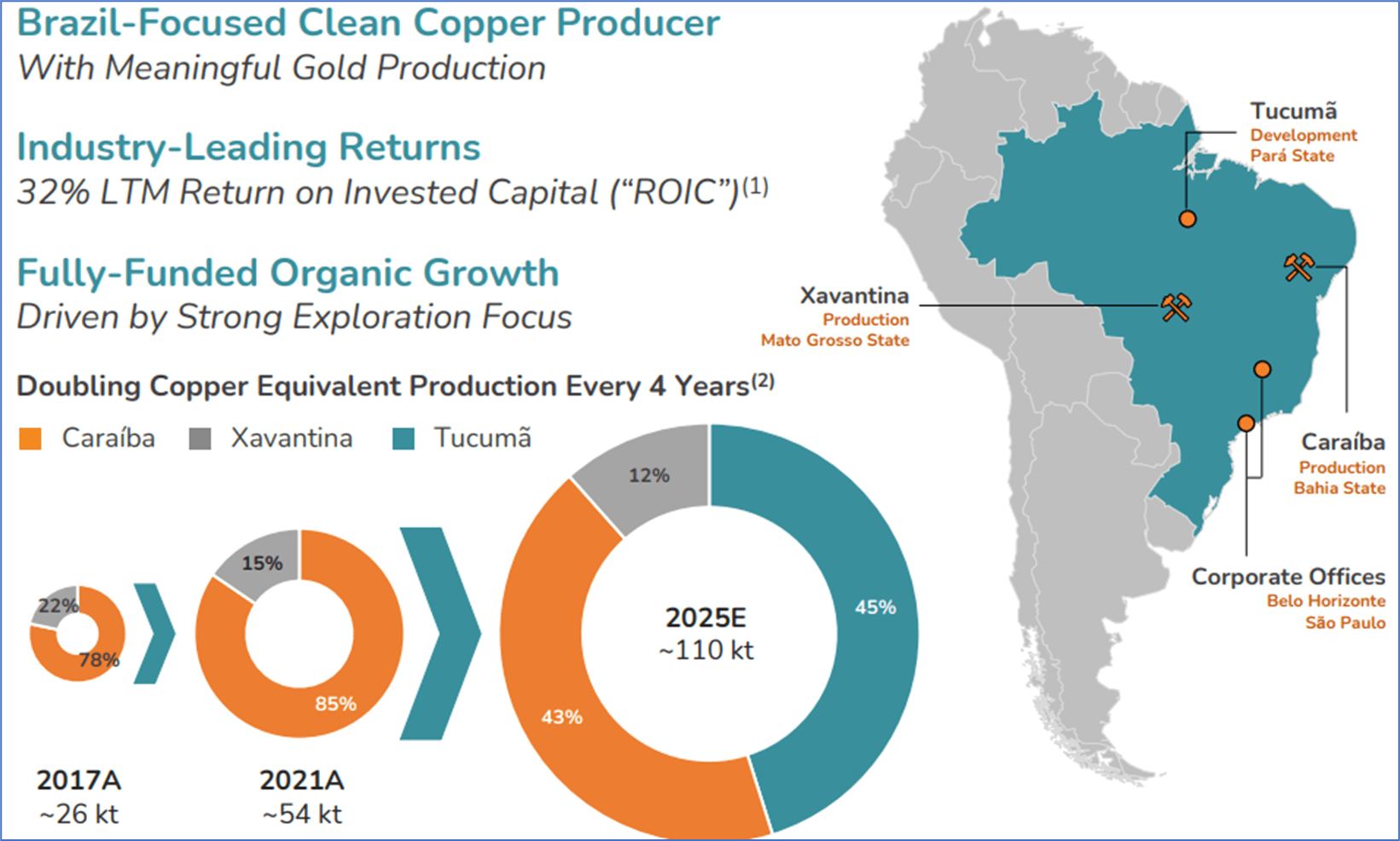

Ero Copper’s stated objective is to exploit this soaring supply gap by expanding capacity and output. The company has more than doubled copper production since 2017 and plans on doubling it again by 2025. All copper production to date has come from the Caraiba Operations located in the Curaça Valley, Bahia State (see map below), accounting for 83 percent of revenue in Q2. The company generated about 17% of its revenue from gold mined out of the Xavantina Operations in Mato Gasso. Reaching its ambitious long term targets will depend on ramping up copper production at what it calls the Tucuma Project in Para, Brazil. The first production forecast for the Tucuma site is expected in Q3 2024.

Ero Copper Production Growth 2017-2025 (Ero Copper Investor Presentation September 2022)

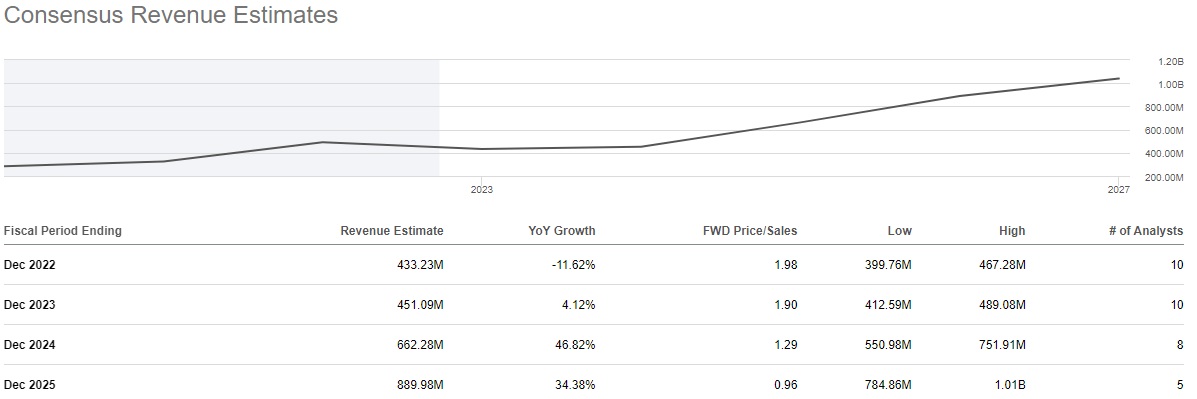

Ero’s growth plan has been pivotal in guiding expectations, with the Tucuma project representing an exciting and timely boost in capacity. Consensus estimates have Ero annual sales growing by more than 100% in the next three years – from about $430 million to almost $890 million – as illustrated in the chart below. Notice the jump in growth from 2023-2025 in anticipation of the new production coming online.

ERO revenue estimates (Seeking Alpha Premium)

Meanwhile, EPS is projected to grow by more than 200%, which can be seen by going to the ERO:CA view on Seeking Alpha. The company stock has traded on the Toronto Stock Exchange (TSX) since 2017 and only since last June on the NYSE, hence the Canadian side has more analyst information. The analysts’ average price target implies that the stock price will grow by more than 50% in 12 months.

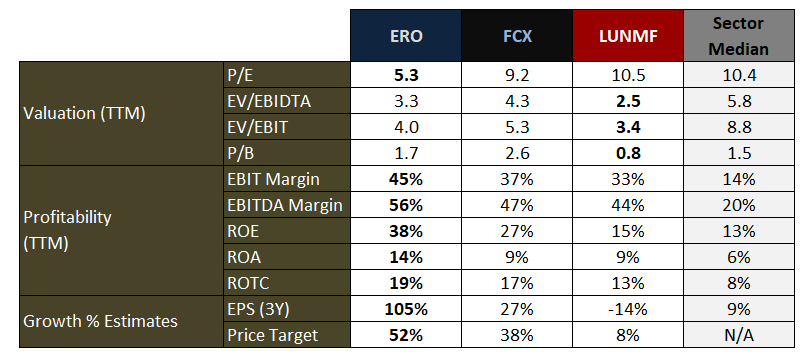

Combine these growth estimates with profitability figures relative to the sector median and its peers, and it is clear Ero Copper’s stock is undervalued. The below table compares some of these key metrics with the sector and two direct competitors: Freeport-McMoRan (FCX) and Lundin Mining Corporation (LUN:CA) (OTCPK:LUNMF). In terms of valuation, Ero beats the sector median and FCX but LUN bests in EV/EBITDA, EV/EBIT, and price/book valuation grades. Ero however leads the sector and both competitors in all profitability metrics and growth targets.

Ero Valuation, Profitability, Growth Metrics Comparison (Data Source: Seeking Alpha)

Great Value, Bad Timing

Between now and 2024 the company will be highly focused on boosting margins to maintain profit growth, which is why analysts have been razor-focused on metrics related to production costs and selling prices. Although the management team has shown an adept ability at cost control and shielding themselves from copper price volatility, Ero missed Q2 revenue estimates due to these very factors, which led to some analyst downgrades.

After their primary customer, Brazilian smelter Paranapanema, had operational issues, Ero was forced to shift volumes onto the international market, thereby exposing it to unfavorable fluctuations in commodity prices. Historically, Ero has had limited exposure to movements in copper prices due to favorable payment terms with domestic customers. The reallocation coincided with a plunge in the price of copper futures, which is down nearly 20% in the past 12 months.

Other reasons export sales lead to higher unit operating costs is due to the loss of domestic tax credits and additional logistics expenses, CFO Wayne Drier explained on Ero’s recent earnings call. In the end, the reallocation resulted in a $13 million reduction in revenue for the quarter. CEO David Strange, on the same call, however, reassured that the operational issues with the customer and the significant deviation in copper pricing were both “unprecedented.”

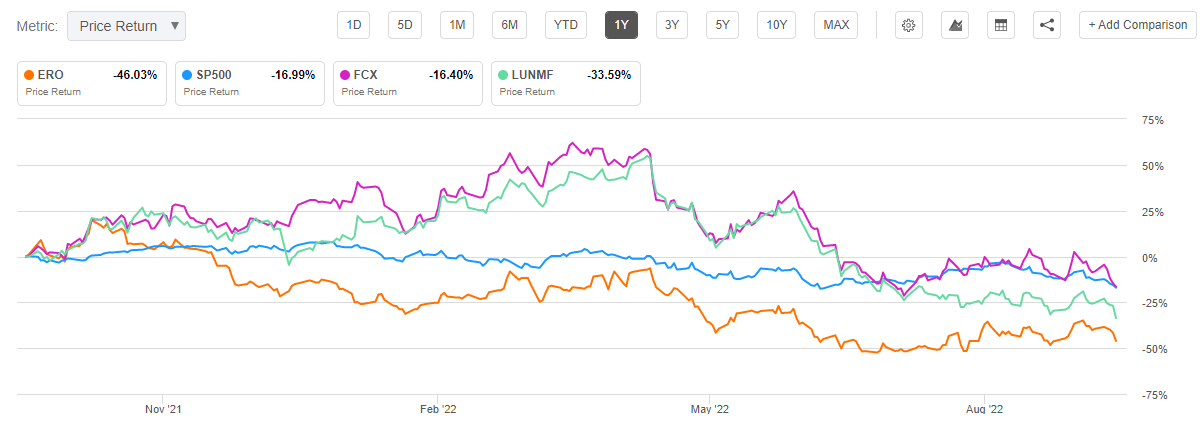

Ero certainly had some bad luck timing-wise in debuting on the NYSE in June of last year. However, Ero’s stock price has significantly underperformed both the S&P 500 and two of its top direct competitors.

ERO 1Y Price Performance Comparison (Seeking Alpha Premium)

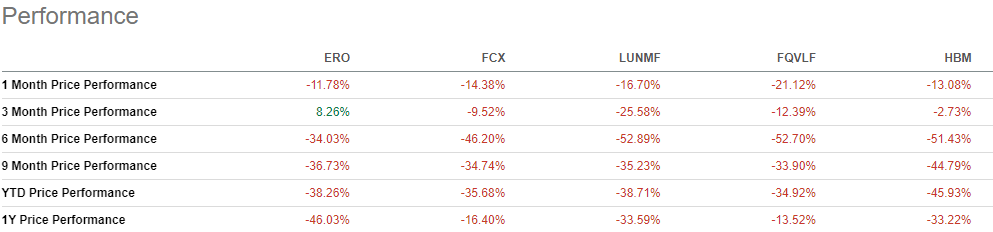

It is hard to attribute Ero Copper’s stock price performance in the past year to poor macroconditions resulting from interest rate hikes when it underperformed the S&P 500 by 30 points. It might be some consolation to point out, however, that it has shown signs of life within the past 3 months, up over 8%, much better than four of its top rivals: FCX, LUNMF, First Quantum Minerals Ltd (OTCPK:FQVLF) and Hudbay Minerals Inc. (HBM).

ERO price performance comparison (Seeking Alpha Premium)

Conclusion

Encouraging 3-year growth targets, ambitious production expansion aligned with projected booms in copper consumption, massive profit margins versus the market, and its low P/E ratio, make Ero Copper’s stock an attractive long-term investment. However, our buy rating is a cautious one in light of the poor price momentum relative to the market and direct competition, along with near-term headwinds. We look forward to the next earnings report to see how the company fares in managing unfavorable fluctuations in copper prices and other costs associated with an increase in exports as a percentage of sales volume.

Be the first to comment