Robert Way

The Italian luxury fashion company Ermenegildo Zegna (NYSE:ZGN), which debuted on the New York Stock Exchange just over a year ago is performing well. In the past year, its share price is up by 18%. This is in line with the run-up in luxury stocks recently, along with consumer discretionary ones as such. But here’s the rub. Its price rise is bigger than that for the French luxury giant LVMH (OTCPK:LVMUY), which has gained 14.3% at the time of writing. Can it continue its upward streak?

Improving macro outlook

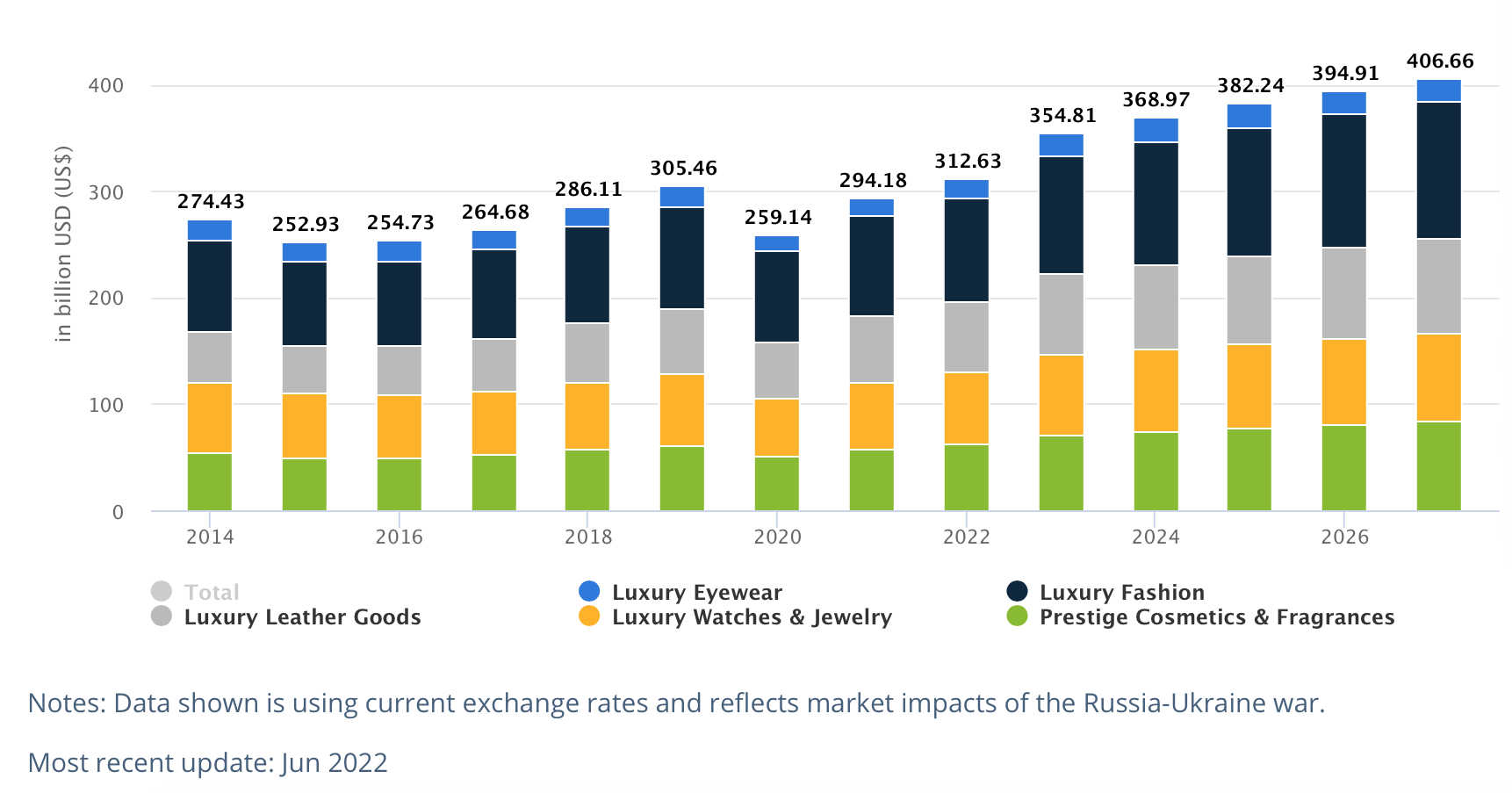

Broadly, there are good reasons for a rise in consumer stocks at the macroeconomic level. Inflation is now showing signs of some genuine come-off, most obviously in the US, where it’s now at 6.5% YoY for December 2022. While fears of recession have been prevalent, they appear to be waning too. Deutsche Bank has, for instance, removed the recession from its 2023 forecast for the euro area. And the relaxation of COVID-19 regulations in China has added to optimism about this big market for luxury products. The outlook for the luxury goods industry is positive, even as such. It’s expected to show a compounded annual growth rate [CAGR] of around 3.5% between 2023 and 2027.

Luxury Sector Size Over Time (Source: Statista)

Robust growth

ZGN’s just released 2022 revenue numbers at 15.5% further endorse the growth in the luxury segment. The company operates under two brands, the first of which is Zegna, which manufactures and markets menswear and accessories. The second, and smaller segment, is Thom Browne, which produces womenswear and accessories. Both segments have seen double-digit growth for the full year 2022, but Thom Browne has grown much faster at 25.3% compared to Zegna at 13.7%. This is because Zegna is a much bigger revenue generator for ZGN though, accounting for 78% of its total revenues. In absolute terms, it has contributed far more to the revenue rise.

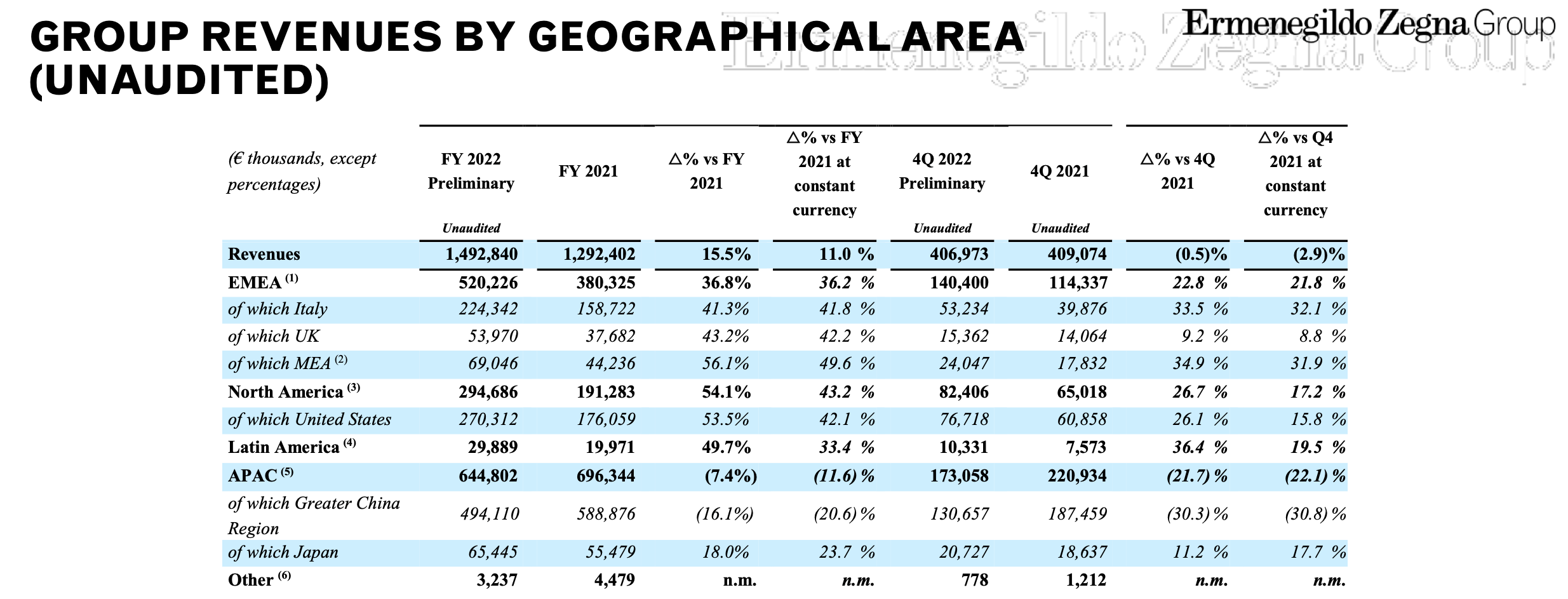

Notably, the growth comes in despite a shrinking in revenue from China by a whole 16%. This is significant because China contributed 45.6% of the company’s revenues in 2021, a figure that has now fallen to 33%. The rise is down to robust growth in its other big markets, like the Europe, Middle East and Africa [EMEA] region as well as North America (see table below).

Source: Ermenegildo Zegna

Q4 2022 signals caution

However, the trends for the latest quarter aren’t quite as encouraging. In the final quarter of the year (Q4 2022), ZGN’s revenue actually declined by 0.5%, and performed even worse in constant currency terms, falling by 2.9%. While growth stayed in double digits in EMEA and North America, the pullback from China became stronger, as revenue declined by 30%. Interestingly enough though, segment-wise, Thom Browne still continued to grow by double digits at 11.5% in Q4 2022, while Zegna fell by 2.2%.

Positive profit projections

Still, the company is positive in its profit outlook for 2022. It “expects a moderate improvement in Adjusted EBIT and a substantial improvement in Profit for FY 2022”. Despite its strong revenue growth for the year, it’s not entirely clear though at first glance why it would expect profit improvement. So far, we have profit figures for the first half of 2022. During that time, both profit and adjusted profit declined by 34.8% and 13.2%, respectively.

However, when seen in totality with its EBIT numbers, the picture becomes clearer. Both ZGN’s reported and adjusted EBIT showed robust growth of 57.2% and 23.7%, respectively. Net profit, however, fell largely because of a put option liability. As it happens, the company doesn’t own 10% of Thom Browne yet. The put option allows ZGN to buy the rest of the stake at a future date, however, given the segment’s strong performance along with the company’s medium-term growth ambitions, the value of the liability has now risen. Profits also suffered because of higher exchange rate-driven losses. Assuming that no such outlier increases in expenses occur during the second half of the year, the company can well deliver strong profits.

Low operating margin

As a luxury company, the one big downside to ZGN however, is its operating margins. For the full year 2021, the gross margin was strong at 59.4%, but the operating margin was at 10.6%. The operating margin has got a shade stronger in the first half of 2022 but has actually declined to 51.5% at the gross level. Margins were particularly important in the last couple of years, as inflation was reigning high, but it’s still not out of the picture. And we are one energy price shock away from its spiking again. So I’d still watch for margins when considering which luxury stocks to buy.

A high P/E

Next, its forward price-to-earnings (P/E) ratio is at a huge 35x, compared to 15.5x for the consumer discretionary sector. Now, it has shown robust growth through the year and it’s still profitable, but even compared to LVUMY, which is trading at 26x, it looks quite high. Also, the trailing twelve months [TTM] P/E is not applicable in this case, because the company reported losses on account of its merger with the Investindustrial Acquisition Corp., a special purpose acquisition company [SPAC], in order to go public. As a result, it ended up with losses in both 2021 and in 2020, presumably because of COVID-19.

What next?

The forward P/E can change of course, if its earnings turn out better than expected. But we don’t know that yet. If the latest update is any indication, that may well be the case. However, two risks to ZGN persist. The first is revenues. The latest decline is a red flag. With the Chinese economy back on its feet, the numbers may stabilise soon, but we will have to see that too. It’s also helpful that its other big markets might just see a slowdown instead of a full-blown recession. And with inflation on the decline, its relatively low operating margins might not matter as much either. The point here is, that there’s just too much up in the air. It’s a classic case of wait-and-watch for me. So I’ll put a Hold on this one.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment