Tony Anderson/DigitalVision via Getty Images

Author’s Note: A version of this article was previously published on iREIT on Alpha.

Dear readers/followers,

In this article, it’s time to look at Equity Residential (NYSE:EQR). The company is a residential REIT and shares its sector with many stellar apartment and residential REITs, such as Essex (ESS) and AvalonBay (AVB). Both of these are REITs I’m invested in, at non-trivial levels (above 1%). Equity is one I’ve been having my eye on for a long time, and I became more and more interested over the past few months.

In this article, I’ll show you why, and why I’m positive about EQR at this time, going into 2023.

Presenting Equity Residential REIT

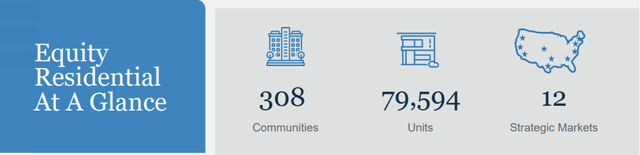

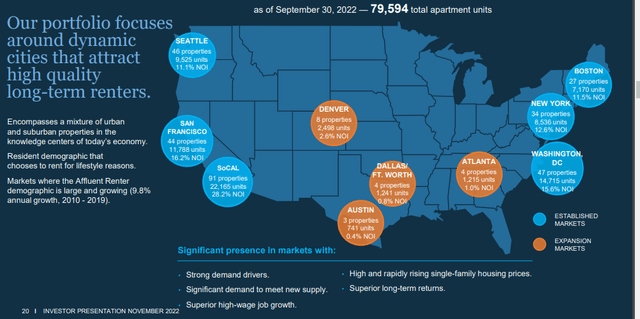

This is a REIT with investments in 308 properties across the USA, totaling almost 80,000 apartment units. Its main markets are Washington, Seattle, San Francisco, and Southern Cali overall – but it’s also pushing into the Sunbelt as well as Denver.

The company has the sort of base statistics you would expect from a REIT in this sector, meaning a high, 95%+ physical occupancy and very high safety ratios. The company is guiding for double-digit same-store revenue growth, and an operating margin on a same-store basis of 68.5%.

The company has been part of the S&P500 since 2001, is stellar at an A-rating, has returned more than the market at 11.2% annually since the IPO in 1993, has grown its dividend by 6.4% annually since 2011, and has an EV of $34B.

It is neither small, risky or quick to move either up or down.

EQR IR (EQR IR)

The company has superb capital allocation histories, strategies, and trends, combining M&A’s with development, with renovations, with portfolio optimization – it does it all.

Ironically, I’ve actually toured one of EQR’s properties, a fact I realized only a few months ago when looking at the company. It was when I was visiting the US and me and my partner at the time were looking for a place for a relatively short term. if the company’s property qualities have held up, I would not mind at all living in the company’s properties.

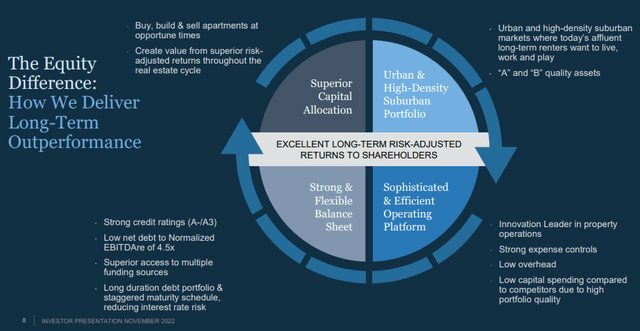

Like most successful REITs, the company has a strategy/approach it follows and how it aims to “differ” and deliver outperformance over time, even form here on out.

EQR IR (EQR IR)

As you can see, it’s basically by continuing with the same strong trends it has until now. Strong credit, low debt, good funding with not much variable, long debts, and reduction of interest rate risks. A company in EQR’s position which has been through multiple downturns can certainly do this.

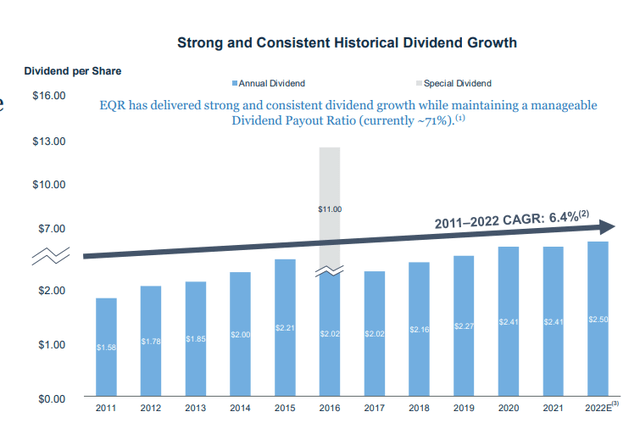

The dividend safety since 2011 has been absolutely stellar in stability, if not in growth. But this is a mature apartment REIT.

EQR IR (EQR IR)

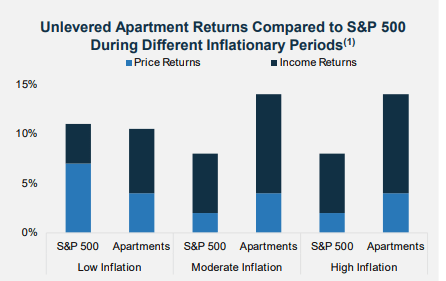

Let me help you recall that apartment REITs have returned some of the best pricing and income throughout most inflationary periods. While they certainly perform well during low inflation, the true “magic” has happened for apartment REITs, including EQR, during higher periods of inflation, as we’re seeing now.

EQR IR (EQR IR)

In fact, in FX was more favorable, I have my doubts I would invest much in non-US sectors outside of REITs – I’d be loading up my targeted 25-30% REIT allocation with quality – which would include EQR.

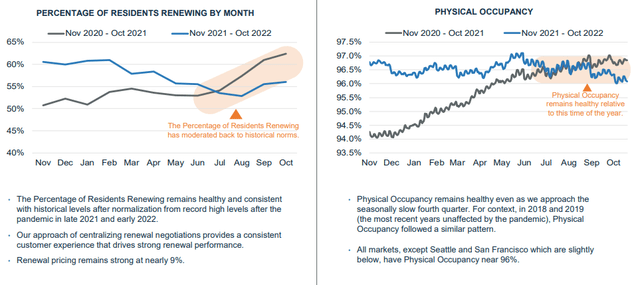

That is not to say that the company is not facing challenges. The recent months in 2022 have seen a relatively atypical decline in the company’s occupancy and renewal numbers.

EQR IR (EQR IR)

While these numbers are nothing to be worried about fundamentally at this time, it is nonetheless worth mentioning, and clarifying, that EQR is in no way immune to these overall trends.

Perhaps the riskiest markets that the company holds are the markets out west, Seattle, and S-F for the main part. This is not unique to EQR, but trends we find in the other major apartment and residential players as well. I personally view the risks as overplayed, especially for high-quality businesses. Even if they in the end are forced to moderate rent growth as a result of lower demand, there will still be plenty of profit available in these regions, as the companies diversify their holdings – as all of them are currently doing.

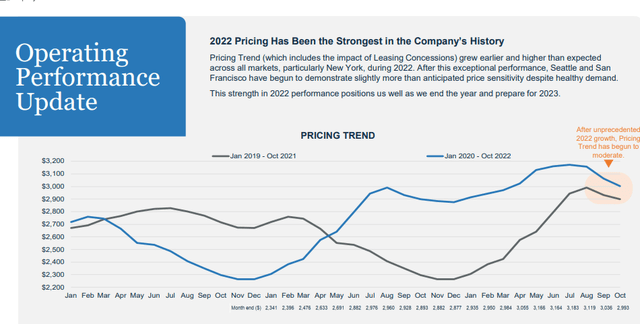

Despite these headwinds, the company’s 2022 pricing trends, have proven to be some of the most advantageous (for EQR) in recent history. Take a look at these trends for 2021, but what happened in 2022.

EQR IR (EQR IR)

So you may see why I may view the risks to the company as somewhat overplayed here. The company’s actually realized same-store revenue growth sets the stage for a potentially strong 2023. The company also sees no fundamental risk to its physical occupancy ratios – it’s expected to continue to be around 96-97%.

The company does have some bad debt, excluding rental assistance – it’s down to around 225 bps, which is well above the historical norm of 50 bps, but down from 275 bps back in 2021. EQR’s renters are typically affluent, which means typically that the normalization is going to be faster – but we’ll see how things go here. What I want to point out though, is that this is not justifying the current levels of valuation.

2020 turned out, in retrospect – to be one of the hardest years in recent memory for EQR and similar companies. It came to around negative 3.9% embedded growth – a metric we get by annualizing total lease income anticipated for the last month of the current, not counting vacant, compared to anticipated actual full-year lease income for the current year (without regard to vacancy) and excluding the impact of Leasing Concessions.

The current trend for the coming year is expecting this to grow to 4.5% (positive), which is well above the current average from 2016 and up until now, which excluding 2020, has been around 1-2%.

While company expenses are up – mostly due to utility costs and the like, which the company can do nothing about – EQR is working with initiatives to lower the expenses, such as reductions in on-site payroll.

Also, it’s important to realize that EQR guiding and realizing expense growth rates of less than 3.5% means that it’s well below the comp average of around 5%. It’s doing better than other Residential REITs.

EQR IR (EQR IR)

So, a small checklist here.

-

Company fundamentals? Check – A-credit and a solid portfolio across the entire nation, though with a legacy of overexposure to coastal regions, and nothing in Florida.

-

Dividend? Check – 4.21% means it’s not only good, but it’s also higher than peers.

-

Expense control/inflation? Check is what I would say here – the company has this under control better than most of its peers, or at least on an equal footing.

-

Forecasts? Check, again. I believe the company will realize a same-store growth rate for 2023 which will result in FFO outperformance, and grow by 6-7% at least, as are the current forecasts.

-

Valuation? Let’s see.

Company valuation

EQR is attractively valued here, even if since the time of this article’s original publication on iREIT on Alpha, the share price has improved several percent. The company’s typical 5-year average comes to around 20-22x P/FFO, which is the range for most premium Residential REITs, of which EQR is one. The company’s A-credit and other fundamental characteristics make other considerations almost impossible.

EQR currently yields 4.21%, which is well above its average, and its current P/FFO is 16.8x normalized. We can compare this to 16.7x for AVB, and 14.8x for ESS – however, ESS also has a somewhat lower credit at BBB+, so there’s some explanation for the slightly lower valuation.

EQR might not be the most undervalued residential REIT out there, but in terms of growth estimates, it beats out both of the others here. The upside to a ~21x P/FFO normalization is about 17% annually, or 60% until 2025E. Even if it normalizes at 18-19x, that’s still a double-digit annualized RoR.

EQR Upside (F.A.S.T graphs)![]()

Analyst forecast accuracies here are nothing to joke about – only an 8% miss rate, the rest of the time, the analyst hit their target with a 10% MoE. Like other apartment REITs, this one of relatively stable and easy to forecast.

Historically speaking, whenever this company has traded below its 20-year premium of 18.8x, it’s been a time to invest, because the company has reverted back, and above it, sooner or later. When that happens, EQR can go as high as 30x P/FFO, leading to some very impressive amounts of overall outperformance.

While we’re not yet near the trough levels of 2020, which saw 14x, or 2009, which saw even lower, 16.8x is enough for me to really shine a light on this company, what it does, and what it usually achieves. I believe you should not overlook EQR at this time.

EQR offers living space to people with above-typical household average incomes. That’s a category of people that are typically more resilient to chaos in the market.

EQR IR (EQR IR)

And even if these individuals need to cut down on luxuries, living space and apartments will be among the last thing to go, not the first. Given the average age of the resident, it’s also likely that there will be smaller amounts of churn from these residents.

All of these lend themselves to positive valuation and pricing trends, which in turn lends credence to the premium view I hold of this company. EQR at the right price is part of my “basket” of Residential REITs, which includes AVB and ESS, but also EQR (as well as Mid-America (MAA)).

All of these REITs have more in common than they have in terms of what sets them apart. They’re superb businesses with a good future.

S&P Global analysts average PTs between $59 on the low side and $95 on the high side. You’ll realize that all of the PTs are mostly around, or above the current price of the company, and they average to around $70/share, implying an upside of 18.4% to a NAV of 0.76x – a conservative rating for a business such as this one. 22 analysts follow the company, and 10 of them rate this company at a “BUY” or equivalent here.

This means that there are investors that think these companies can fall further before finding a “bottom”, and indeed, this could be the case.

So, there are plenty of ways to invest in EQR – but what I want to point out here is that this is an attractive investment, no matter how you choose to enter it.

At iREIT, we consider EQR a “BUY” with a PT of no less than $73/share, or a safety margin of 18.6%.

Because of this, this REIT enters my list of “BUYS”. I already own a small number of shares and am looking to get more.

Thesis

- Equity Residential is a very attractive REIT, and the company, like other Resi REITs, has been receiving upgrades as of late, with the company scoring very attractively with analysts. The fundamentals are solid, the yield is there, and the upside is in the double digits.

- I remain exposed to the entire sector and wanting to increase my overall exposure here.

- My PT for EQR is $73/share, which means that even though the company is up to around $63/share, there is still a significant upside here, and I’m buying more over time.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I view the company both qualitative enough, cheap enough and attractive enough to invest in here.

Be the first to comment