sankai

By Raffaele Savi, Head of Systematic Investing & Co-Head of Systematic Active Equity and Jeff Shen, PhD, Co-Head of Systematic Active Equity

Markets have entered a new regime of higher macro volatility as central banks take action to fight inflation. With tighter financial conditions on the way, what’s next for investors?

Since the Great Financial Crisis (“GFC”), we’ve been in an environment characterized by strong financial market returns and low volatility against the backdrop of ultra-accommodative monetary and fiscal policy. A continuous stream of upside surprises in inflation data has led to a material shift—with macro risk making a swift comeback. Amid a new era of unprecedented quantitative tightening, markets have entered a phase of persistently higher volatility and growing uncertainty with potentially broad investment implications.

Macro volatility driving equity markets

Following the pandemic recovery and start of the war in Ukraine, market focus has been dominated by upside surprises in inflationary data. In the US, elevated headline inflation readings have caused the Federal Reserve (“Fed”) to retire the term “transitory” and kick off an aggressive tightening cycle. The Fed raised rates by 0.75% in June, the largest increase since 1994. Several other developed market central banks followed in a rush to normalize policy, joining the Fed and emerging market central banks who had already kicked off tightening cycles.

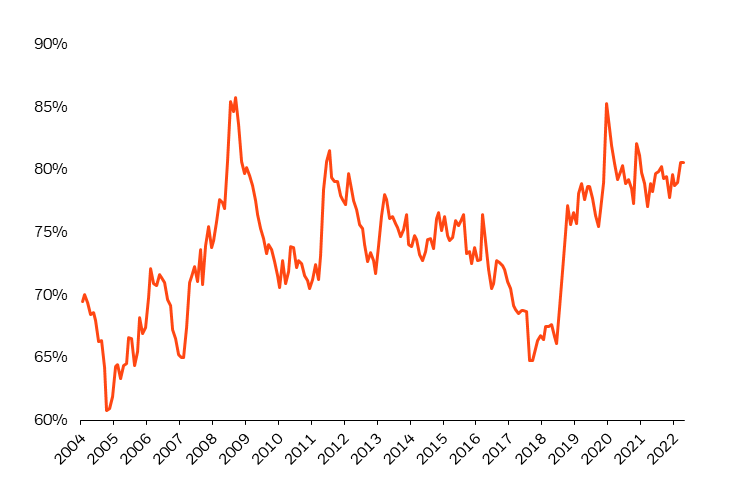

We have entered a new regime with macro factors driving asset prices and contributing to a higher level of volatility than we’ve seen in recent decades. Figure 1 underscores this shift, with macro risk factors explaining more than 80% of asset returns for the model shown below—a level comparable to highs seen during 2008 and 2020.

Figure 1: A new regime of macro volatility

Macro risk factors contribution to asset returns (%)

Source: BlackRock, as of June 30, 2022. Macro factors include growth, inflation, real yield, emerging, credit, and liquidity. Model asset universe includes Global FX, Equities, Fixed Income, Credit, and Commodities.

Markets have undergone a hawkish repricing as investors weigh the possibility of lower growth in a new era of quantitative tightening. This is further complicated by the potential consequences of higher interest rates with unprecedented levels of public and private sector debt in the system. Given these dynamics, are markets accurately pricing recession risk, or is the reaction overblown?

Will the inflation fight cause a recession?

Looming recession risk relies partly on the path of inflation as we look ahead. The war in Ukraine has led to soaring commodity prices—notably energy—further layering on existing supply constraints. Despite a recent decline in energy prices, markets are pointing to further price pressures in Europe due to supply-demand imbalances throughout the upcoming winter months and the gradual end of lockdowns in China. In our view, energy markets are becoming a bifurcated story with a more stable outlook in the U.S., but a challenging road ahead for Europe.

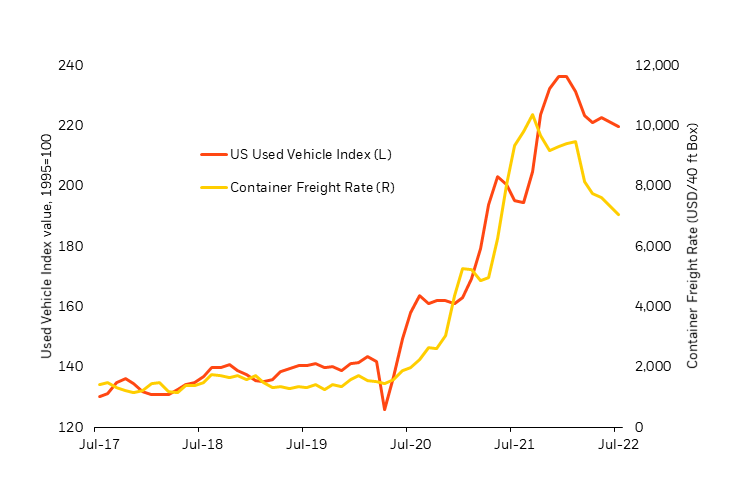

While inflationary pressures are persisting in certain areas, others appear to be improving. Figure 2 shows that supply bottlenecks may be normalizing for used cars along with decreasing container freight transport costs which are an important component of global trade.

Figure 2: Supply bottlenecks may be easing

Value of US Used Vehicle Index and Container Freight Rate

Source: BlackRock, Bloomberg, as of June 30, 2022.

Labor tightness in focus

In addition to supply-driven inflation, the post-COVID economic restart unleashed pent-up demand for services, compounding those pressures through a tighter labor market. The state of the labor market is crucial to assess the inflation outlook and future growth expectation—raising the issue of how tighter monetary policy can be effective at offsetting inflationary pressures.

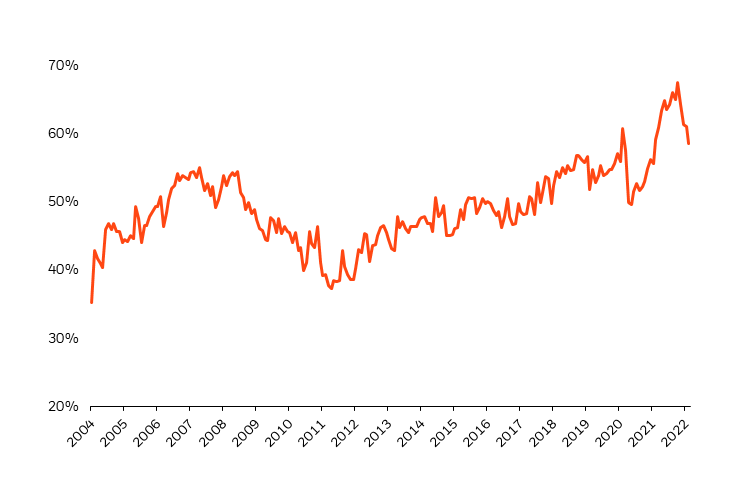

Figure 3 shows the percentage of US industries experiencing wage increases beyond seasonal norms. While wage inflation remains high, the data shows early signs that the rate of acceleration may be moderating. Despite this dynamic, we expect labor market tightness to persist in the near future as tighter financial conditions haven’t created a meaningful deceleration in the labor market.

Figure 3: Wage pressures remain elevated

% of US industries with wage gains beyond seasonal norms

Source: BlackRock, Bureau of Labor Statistics, June 2022. Figure illustrates the diffusion index of average hourly earnings across US industries.

Along the same lines, we monitor the volume of online job searches to gauge changes in labor market supply. Job search intensity is slowly normalizing but still remains roughly 10% below peak levels despite making a significant recovery from lows seen during the pandemic.

Weighing recession risk

So does tightening policy to control inflation require reducing demand to the point of a recession? Analyzing the consumption patterns across different income cohorts shows a universal decrease in the demand for goods at each income level in recent months. In our view, this decrease is a function of the aggregate shift from goods to service spending and isn’t necessarily a recessionary signal.

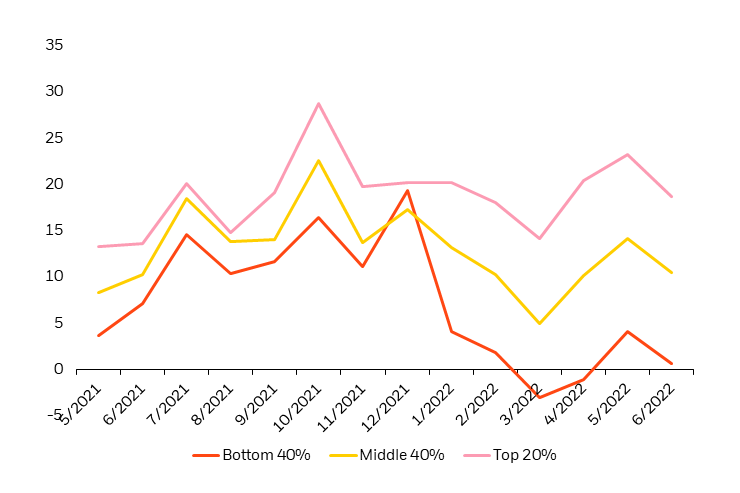

As demand has shifted towards services, examining service consumption reveals divergence in spending patterns across income groups (Figure 4). Spending has remained relatively stable for higher-income individuals compared to weakening consumption in the lower and middle-income cohorts. In the case of a near-term recession, we’d expect to see a broader retrenchment in service consumption across all income levels—including higher-earners.

Figure 4: Divergence in service spending

Discretionary service consumption by income cohort

Source: Earnest Research, as of June 30, 2022. Figure shows consumption for bottom, middle, and top income cohorts.

As economic growth concerns rise, we’re monitoring news articles and company releases for language related to job cuts and hiring freezes. Figure 5 shows that we haven’t seen a broad, economy-wide uptick in mentions anywhere near the highs seen during the Great Financial Crisis or COVID-19 pandemic. Taking a closer look at individual sectors reveals a notable increase in language related to hiring slowdowns for technology companies. We view this as an industry-specific theme that hasn’t evolved into a widespread narrative across the economy. We observe a similar pattern in Google searches of the term ‘recession’ that show a high concentration in areas with a significant footprint in the technology industry including Austin, TX and San Francisco, CA rather than a broad-based trend.

Figure 5: Job cut language isn’t broad-based

Job contraction mentions across global markets

Update Source: Source: BlackRock, Dow Jones News, as of June 30, 2022.

Inflationary pressures and slowing growth appear likely to persist in the near future. However, our alternative data insights point to a lower probability of a near-term recession and potentially more robust economic activity than what markets are pricing.

Positioning for a new market regime

We have entered a new regime of higher macro and market volatility. Central banks face a delicate tradeoff between inflation and economic growth, with risk premia also rising as a result. While growth has started to slow down materially, it’s important to note that it’s coming off of record-high post-pandemic levels. In our view, opportunities remain to achieve an orderly macroeconomic adjustment that leads to sound financial outcomes. However, we believe investors should factor in the implications of investing in a new market regime.

As a result, we’ve shifted our global models to adopt a more defensive stance in favor of industries with inelastic demand including healthcare, utilities, and consumer staples amid slowing growth. In terms of portfolio construction, high inflation and volatility have put pressure on the traditional 60/40 portfolio, breaking down the diversifying nature of the relationship between stocks and bonds. In our view, this may require considering new sources of return and diversification with greater dynamic adaptability—including liquid alternatives for example.

Elevated macro volatility also means that market dynamics are likely to evolve at a faster speed than we’ve witnessed in the last decade—potentially creating a rich landscape for alpha generation both in the cross-section and directional asset price views. However, investors will need to be more nimble to navigate frequent macro and policy shifts. We believe this richer alpha opportunity set is best suited for systematic investment processes transforming vast timely datasets into investment insights faster, at greater scale, and with more granularity than traditional methods.

Conclusion

As central bank policy evolves to try to contain inflation, a new era of quantitative tightening and elevated macro risk will likely continue driving financial markets in the coming months. Market repricing has been significant this year across asset classes as investors weigh the inflation-growth tradeoff and growing fears of a recession.

Inflationary pressures and tight labor markets are likely to continue in the coming months, although some signs of relief are beginning to appear. While global growth is slowing, it’s coming off of record-high post-pandemic levels and the economy appears to be stronger than asset prices suggest.

In our view, this means investors can still take advantage of compelling investment opportunities on the horizon. However, the new macro and market regime may require rethinking portfolio construction and incorporating new sources of diversification and return to the traditional 60/40 portfolio. At the same time, a dynamic data-centric systematic investment approach can help investors capture fast-evolving opportunities as they emerge amid persistently higher volatility.

This post originally appeared on the iShares Market Insights.

Be the first to comment