imaginima

EQT Corporation (NYSE:EQT) management understands that more than a vision is needed to create a sound business. As the tech bubble bursts because the vision was not matched with a well thought out business plan in a lot of cases, EQT Corporation provides a very good example of how to grow a business that actually will be there for a long time to come. Competitive moat equivalents often come from good management execution. Many times, management is the most important asset (or liability) not on the balance sheet or in the financial notes. This management is one heck of a shareholder asset.

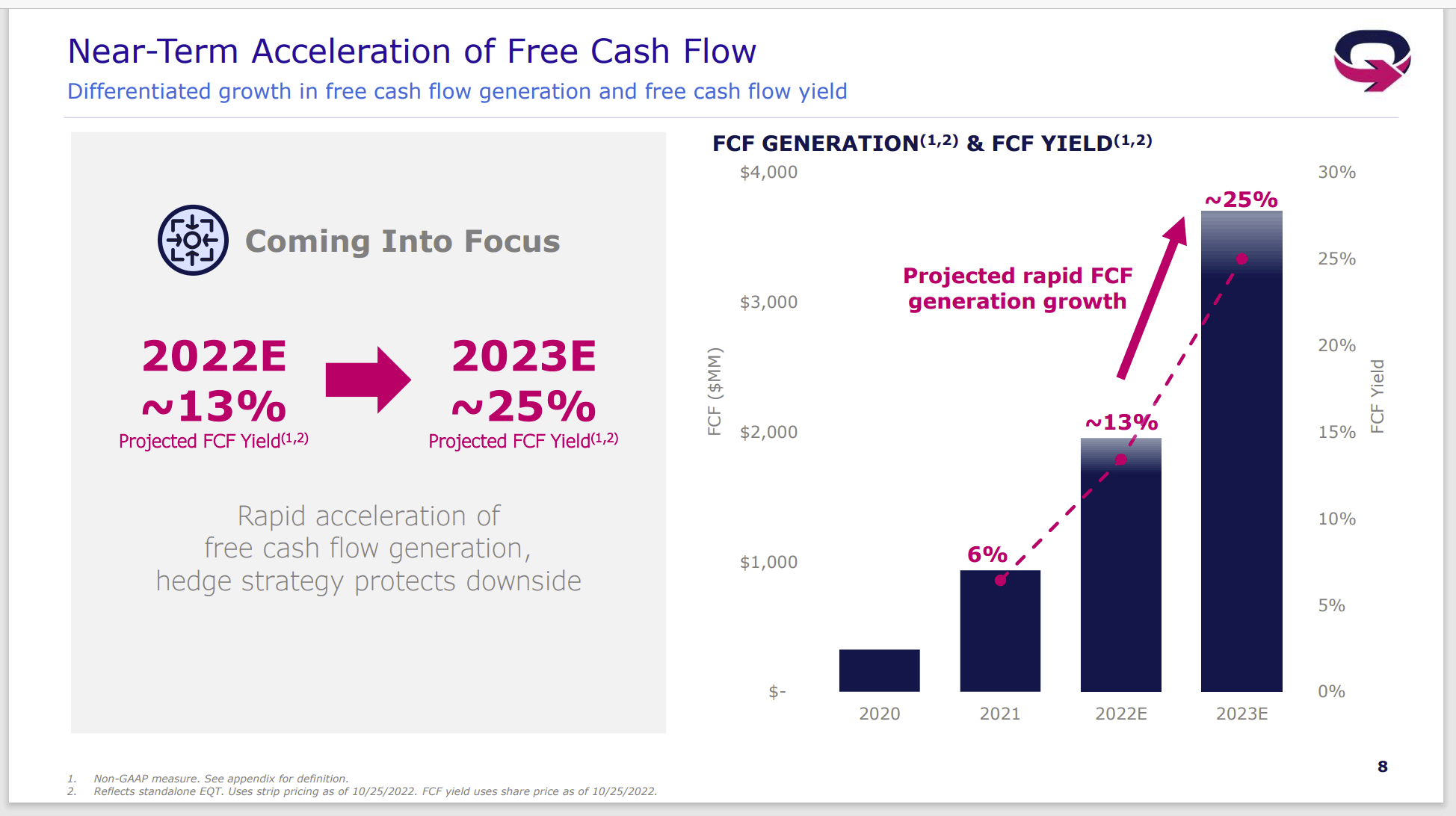

EQT Free Cash Flow Guidance (EQT Shareholder Presentation For Third Quarter 2022, Conference Call)

EQT demonstrates how oil and gas is further along the curve than is much of the technology crowd (where the current asset bubble is being deflated). Oil and gas had the industry “housecleaning” back in 2015. Further “housecleaning” happened with the 2020 coronavirus demand destruction. Most managements, including this one, were, therefore, ready to provide the necessary cash flow growth that a business requires to be long-term successful.

Many bubbles are being deflated because the claim about being a true disrupter fails when there is no cash to back up the claim. Accounting turns out to allow a lot of management assumptions and choices to allow for the reporting of profits without the necessary cash flow. All that means is that management picked some very optimistic accounting assumptions that are allowed to report profits. But the cash flow statement tells the real story about the profit potential of a business.

Here, EQT Corporation management is not about to repeat old industry mistakes or take after the “bubble” crowd that is now in the process of retrenching. As shown above, there will be cash to back up the promises of a lot of profits. This business will be thriving long after a lot of companies that pursued only revenue growth crash and burn.

Cost Cycle Reduction

A lot of established companies often have a continuing cycle of cost reduction because many industries benefit from continuing technology advances. Therefore, if a company wants to be around a long-time, then continuing cost decreases are the order of the day.

Many pioneer companies skip the cost reduction process for a very long-time because “they have the field to themselves.” They can sell a “new toy” for a premium price without the quality worries that are far larger considerations for more established companies.

The problem with this is when the established crowd decides to enter this new market, they automatically drive costs down because they have been doing it a long time. That often catches a pioneering company by surprise. That leads to an unexpected competitive disadvantage.

EQT Cost Improvement History And Implied Guidance (EQT Third Quarter 2022, Earnings Conference Call Slides)

Oil and Gas, like many industries, constantly decreases operating costs. The declining cost curve along with abundant potential drilling targets (really throughout the industry) implies a period of lower pricing that will eventually make its way to the consumer.

The cure for high prices is high prices. But the process is always messy. It does not happen when you expect it or as you expect it. But the market will get there as it always has in the past.

Some tech companies are about to learn this the hard way. They may have had a new idea when the business got started and it may have still been new when the business went public. But unless that idea provides a competitive moat or long-term advantage, then the new company will not likely withstand any competition that appears to be entering a lot of new “tech” industries.

Here, with EQT Corporation, the advantage is some of the lowest costs in the industry for a dry gas producer. That advantage is likely to last for some years to come. But just as the tech industry often sees “a better mousetrap,” this industry often sees new basins come online that were previously not commercially viable. Technology keeps moving to change the competitive landscape in a lot of industries (in remarkably the same way despite obvious industry differences).

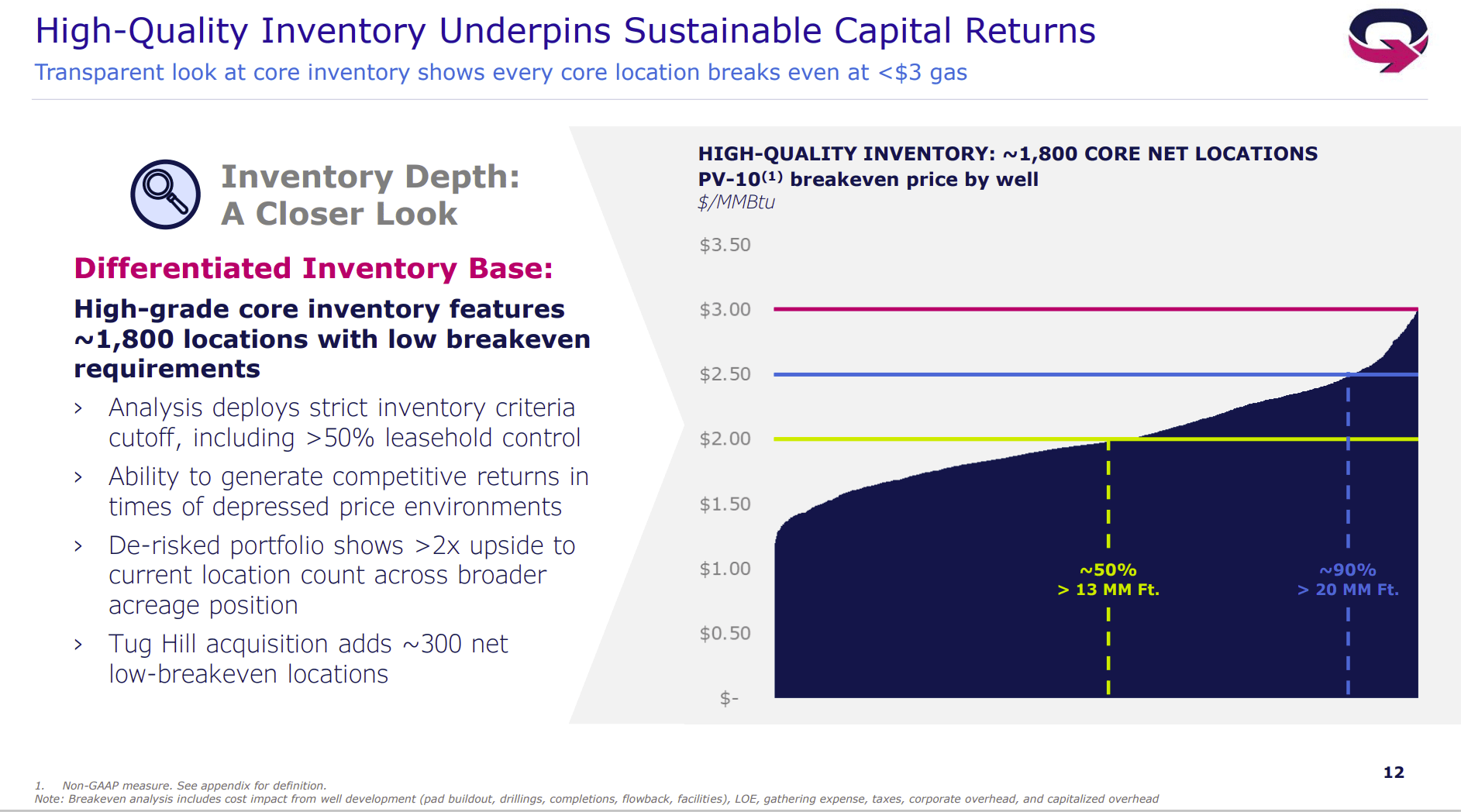

EQT Drilling Inventory Breakeven Points (EQT Third Quarter 2022, Earnings Conference Call Slides)

As the North American natural gas industry joins the world natural gas market, the low-cost inventory shown above is going to generate a lot of cash flow long-term. Historically, the world market has stronger pricing than the usually oversupplied North American market.

The number of projects underway to enable more export ability is breathtaking. All that is needed is some patience on the part of shareholders. That probably means a solid company like EQT Corporation is a potential investment proposal before all that exporting capability comes online.

The Weather

Currently, the weather is forecast to be warm. But that is typical for La Nina. The cold Arctic air leaks that give this weather pattern its cold reputation often happen with little advance notice. Yet January and February (and sometimes March) are well known for periodic (or even one big) Arctic air leak that often sends temperatures downward.

Because there is little notice and the event itself is not regarded as predictable or even reliable to the markets, these cold spells are often met with little market reaction. Yet if enough of them cause a material change in the natural gas supply, the market will react to lower long-term supplies because a La Nina winter is often followed by a hot summer that further puts pressure on natural gas supplies.

The current winter is far from over and could have some more cold days ahead despite the long-term forecast that is typical for this weather pattern.

The Future

Oil and natural gas has already had its deflating period and has been housecleaned. The survivors have learned to generate free cash flow and give at least some of that back to the shareholders. Because that lesson has been learned, the industry will likely outperform the current stock market action by a comfortable margin in the future.

The oil and gas story about pricing was slightly different. Unconventional events arrived after oil prices rose as demand kept prices high for some time beginning in the 1990’s. Like the tech cycle (but for a different reason), costs were not as important because oil prices remained stubbornly high. Natural gas may be about to enter such a period, as North America increases the exporting capability to join a very strong world natural gas pricing market. But for investors, long-term company survivors are nearly always the ones emphasizing low costs regardless of the current environment. This is something the tech crowd will learn the hard way.

Dry gas producers actually suffered terribly during the growth of unconventional production. As a result, issues like competitive advantage, low costs, and competitive moat equivalents have long been a part of the industry operating priorities.

The oil industry went through growing revenue and growing reserves without regard to cash flow earlier in the decade and before when it was the “hot industry.” Natural gas producers actually tended to move to “liquids rich” production to escape the excess natural gas supply effects. Chances are there will be technology improvements at some point in the future that will again make the natural gas industry hot.

Anytime I have ever gone to a presentation by geologists, I always get the answer that the earth has plenty of oil and natural gas remaining. We just have to depend upon continuing technology advances to get it.

EQT Corporation has darn good geology underlying the acreage. That quality appears to allow the company to have a low-cost advantage for a long time to come. Management appears to want to keep that advantage by continuing to lower costs in line with much of the industry.

The company has achieved that investment grade status that puts it financially ahead of much of the industry. The demand for natural gas as a source of hydrogen (a rapidly growing market) and plastic should keep this industry busy for a very long time to come. Management has positioned the company to take advantage of the future.

Investors should consider holding EQT Corporation until the long-term story changes or until management considers selling the company for a good price. Oil and gas tends to be a volatile field. But EQT Corporation management has had considerable success with past companies. Therefore, it is probably wise to follow the lead of EQT Corporation management unless the prices gets so out of line, that it represents several years’ worth of future appreciation.

Be the first to comment